Earnings Per Share Significantly Beats Expectations, Why Did Occidental Petroleum Still Fall Over 7%?

AI Podcast

Occidental Petroleum shares fell over 7% as oil prices dropped below $100 per barrel due to easing geopolitical tensions. Despite a raised price target from HSBC, the stock declined. Q1 revenue missed expectations, though adjusted EPS exceeded forecasts, driven by a one-time gain from the OxyChem sale rather than core operations. Overseas asset disruptions led to lowered 2026 production guidance. Free cash flow turned negative, impacting deleveraging risks. However, debt reduction is progressing. Analysts maintain an average price target of $64, implying upside potential. Market sentiment remains tied to oil prices and operational recovery, not earnings outperformance.

TradingKey - On May 6, Eastern Time, Occidental Petroleum ( OXY.US) shares fell by more than 7% intraday.

Oil price anchors are loosening as bearish macro factors resonate. Over the past two trading sessions, geopolitical tensions between the U.S. and Iran have continued to ease, with Brent crude dropping to $98 per barrel and WTI crude to $95 per barrel, both slipping below the $100 mark for the first time since late April. For energy stocks such as Occidental Petroleum, oil prices are the most sensitive variable in the earnings curve; the sharp correction from the removal of the 'war premium' has weighed on the share price.

[Occidental Petroleum Stock Price, Source: Google Finance]

Although HSBC Holdings raised its price target for Occidental Petroleum from $68 to $73 during after-hours trading, the stock still fell by as much as 1% in pre-market trading on May 7, Eastern Time, weighed down by the continued decline in international crude oil prices.

Q1 performance pressured by geopolitical conflicts.

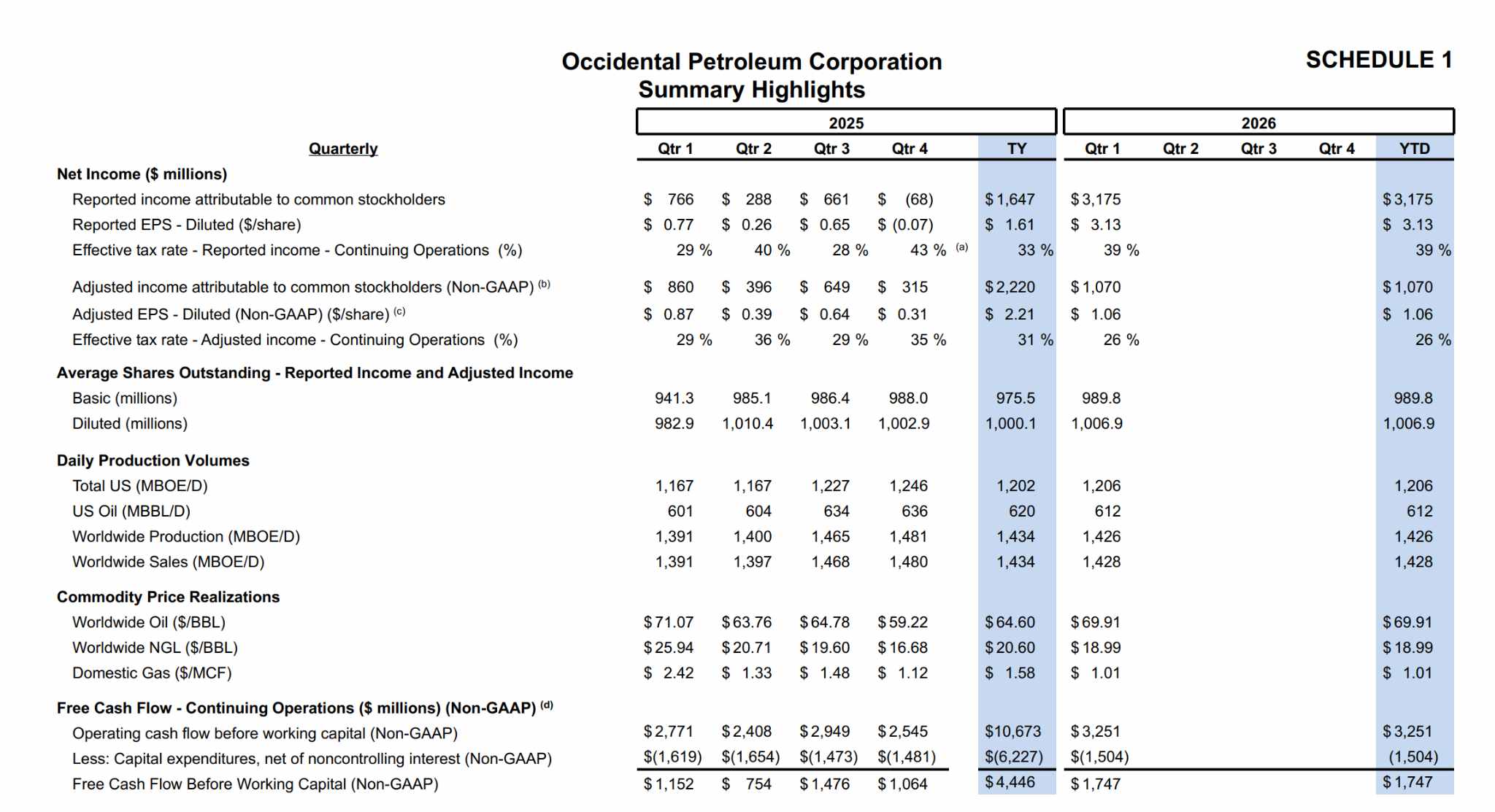

The earnings report shows that Occidental Petroleum's first-quarter 2026 revenue was $5.23 billion, falling far short of analysts' expectations of $5.67 billion and representing a decline of approximately 11% year-over-year; however, adjusted earnings per share reached $1.06, significantly exceeding the expected $0.59, an increase of 79.7%.

[Occidental Petroleum Q1 Earnings Results, Source: OXY Investor Relations]

In fact, following Berkshire Hathaway's acquisition of OxyChem, Occidental's chemical subsidiary, the company recorded high profits driven by a one-time gain of $9.7 billion. This resulted in earnings per share significantly exceeding expectations, which, combined with an unusually low effective tax rate for the industry, pushed up quarterly profits—a situation not directly related to the operational performance of its core business. Meanwhile, weighed down by the conflict in the Middle East, some of the company's overseas assets remain in a suspended state.

At the same time, Occidental holds a 40% interest in the Shah gas field in the UAE, where operations have been fully suspended since an Iranian attack on March 16; other operations in Algeria, Oman, and Qatar have also not yet resumed. Consequently, management has lowered its 2026 full-year daily production guidance to 1.41 million to 1.46 million barrels of oil equivalent (boe), down from the previous forecast of 1.42 million to 1.48 million boe.

More concerning is the reversal in free cash flow. Due to delayed customer payments and supply chain mismatches between receipts and disbursements, free cash flow plummeted from a positive $466 million in the same period last year into negative territory at -$112 million.

Within a macro cycle where the company continues to pursue further deleveraging, the shift to negative cash flow increases the risk of delayed debt repayment. However, progress on debt reduction is proceeding simultaneously: Occidental repaid $7.1 billion in debt in the first quarter of 2026, and its macro leverage ratio is nearing the company's $10 billion target.

Previously, following the sale of its OxyChem chemical business, the company underwent a strategic transformation to focus on oil, gas, and carbon management. This decision accelerated debt reduction and enabled better value creation within its core operations. HSBC has repeatedly raised its price target for Occidental Petroleum.

Market institutions maintain a wait-and-see stance.

According to data from London Stock Exchange Group (LSEG), 26 analysts have a 12-month average price target of $64 for Occidental Petroleum. Based on the current stock price of $55.12, this implies an upside potential of over 16%.

[Occidental Petroleum Analyst Ratings, Source: TradingKey, LSEG]

Most institutions did not revise their ratings or price targets following the earnings release. Market sentiment indicates that the core logic for institutional long positions in Occidental Petroleum remains tied to the pace of oil price changes and continuous operational recovery, rather than any sentiment driven by earnings outperformance.

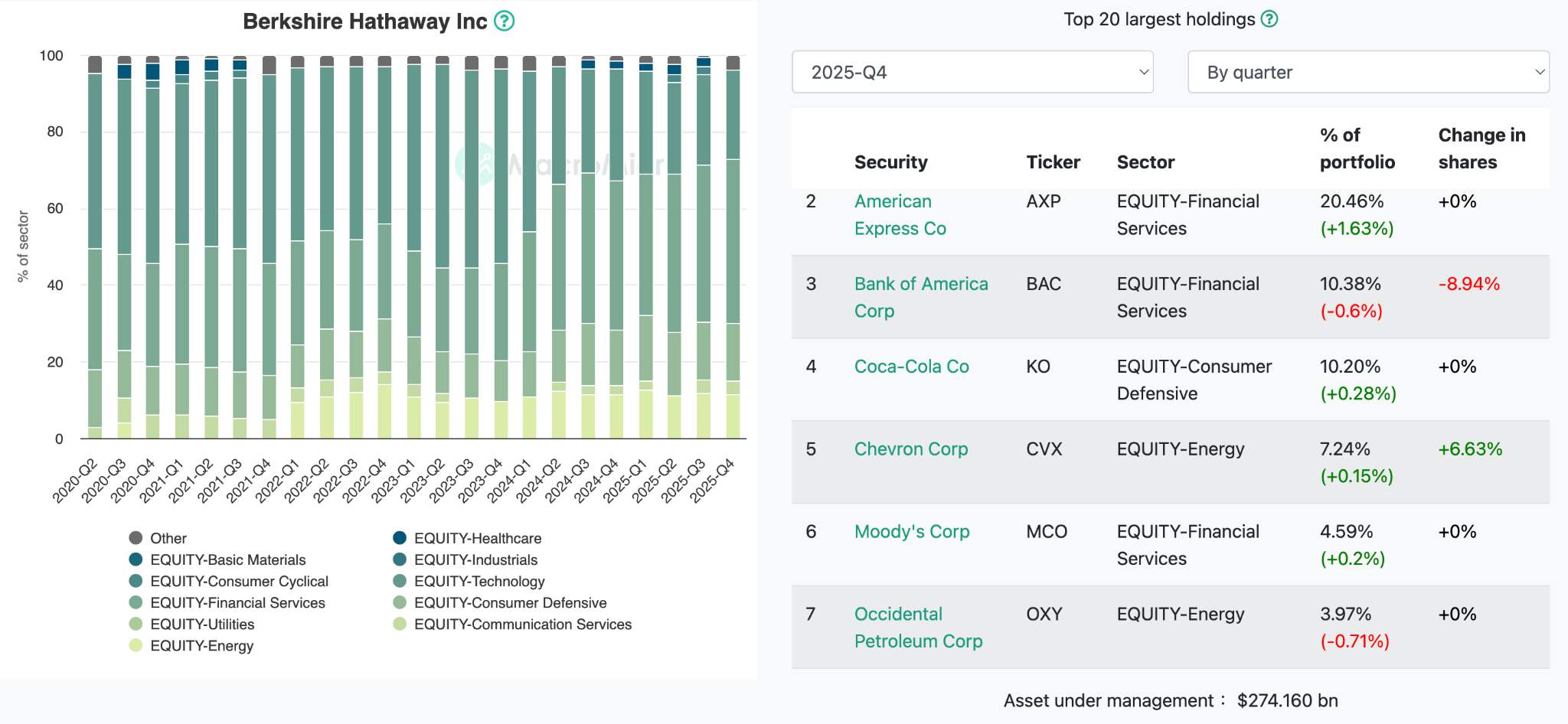

[Berkshire Hathaway Q4 2025 Holdings, Source: Macromicro]

Occidental Petroleum's stock price showed strong resilience in the first quarter of 2026, with year-to-date gains repeatedly hitting new highs. This was also supported by the substantial position held by Warren Buffett's Berkshire Hathaway in 2025, which provided solid price support for the market.

However, the current correction in oil prices and weaker-than-expected earnings have created "dual pressure." The limited intensity of institutional upgrades and the lack of policy catalysts continue to weigh on the stock. Despite the endorsement from Berkshire's holdings, secondary market liquidity pressure can hardly offset the combined impact of these two major headwinds.

As the core driver of oil prices shifts from a "war premium" back to "supply and demand fundamentals," clear divergence will emerge within the energy sector, which has already accumulated significant excess gains this year. Whether Occidental Petroleum can effectively digest the additional costs of overseas operational disruptions will determine if its valuation can recover in the next phase.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.