Coca-Cola Earnings Preview: Moat Remains Robust, Defensive Attributes Regain Investor Favor With AI Support

AI Podcast

Coca-Cola (KO.US) is set to report Q1 FY2026 results on April 28, with Wall Street expecting revenue around $12.244 billion (up 9.17% YoY) and adjusted EPS of $0.81. The company's stock has gained 7.49% YTD, outperforming the S&P 500. Analysts highlight Coca-Cola's low-volatility and high-dividend profile, brand strength, and global distribution network as key resilience factors amid inflation and geopolitical risks. New CEO Henrique Braun is focusing on AI integration to enhance marketing, forecasting, and pricing power, while maintaining an outlook for 4%-5% revenue growth and 7%-8% EPS growth in 2026.

TradingKey - Coca-Cola, the world's largest beverage manufacturer (KO.US) will report its first-quarter results for fiscal year 2026 before the U.S. market opens on April 28. This marks the first quarterly performance report since new CEO Henrique Braun took the helm.

Wall Street consensus estimates project Q1 revenue of approximately $12.244 billion, representing a year-over-year increase of about 9.17%; adjusted earnings per share are expected to be $0.81, up roughly 11% from $0.73 in the same period last year.

Coca-Cola's stock has climbed approximately 7.49% year-to-date, outperforming the S&P 500's 4.27% advance and several mega-cap tech stocks, including Apple. In an environment of geopolitical maneuvering and high interest rates that have kept tech stocks under pressure, Coca-Cola’s low-volatility and high-dividend profile is once again attracting capital inflows.

Expected to Maintain Revenue Resilience Amid Tariffs and Geopolitical Conflicts

Jefferies lowered its price target from $90 to $88, citing input cost inflation and potential supply chain disruptions from geopolitical conflicts in the Middle East; meanwhile, JPMorgan slightly lowered its Q1 EPS estimate to $0.82 (still above the $0.81 consensus) ahead of the earnings release, while reaffirming its $83 price target and Overweight rating, expecting that the rally still has room to run.

Morgan Stanley analyst Dara Mohsenian reaffirmed a Buy rating on March 23 with a $87 price target, emphasizing that Coca-Cola possesses earnings visibility superior to its peers and can maintain robust operations through its strong pricing power, bottling system cost absorption, and partial foreign exchange hedging, even in the face of potential supply chain disruptions such as the conflict in Iran.

JPMorgan further noted on the same day that while the easing of geopolitical tensions might drive capital back into risk assets in the short term, Coca-Cola remains well-positioned to withstand inflationary cost pressures.

Moat Remains Robust: The Rationale Behind Buffett’s “Permanent Holdings”

While the new CEO focuses on AI transformation, the core moat supporting Coca-Cola's long-term compound growth remains unshaken. Coca-Cola possesses two indestructible structural barriers: its brand moat and its operational moat. At the brand level, when consumers think of carbonated soft drinks, 'Coke' is often the first name that comes to mind, with brand recognition that is nearly synonymous with the category.

At the operational level, through an asset-light franchising model of 'concentrate production, bottling systems, and regional distribution,' Coca-Cola retains high-margin concentrate manufacturing at headquarters while licensing low-margin bottling and logistics to independent bottlers. Spanning over 200 countries and regions, it has established an irreproducible, low-capital-intensity global distribution network.

This enables it to maintain a gross margin of around 60% and an operating margin exceeding 20% over the long term, ensuring financial resilience even when raw material prices fluctuate significantly.

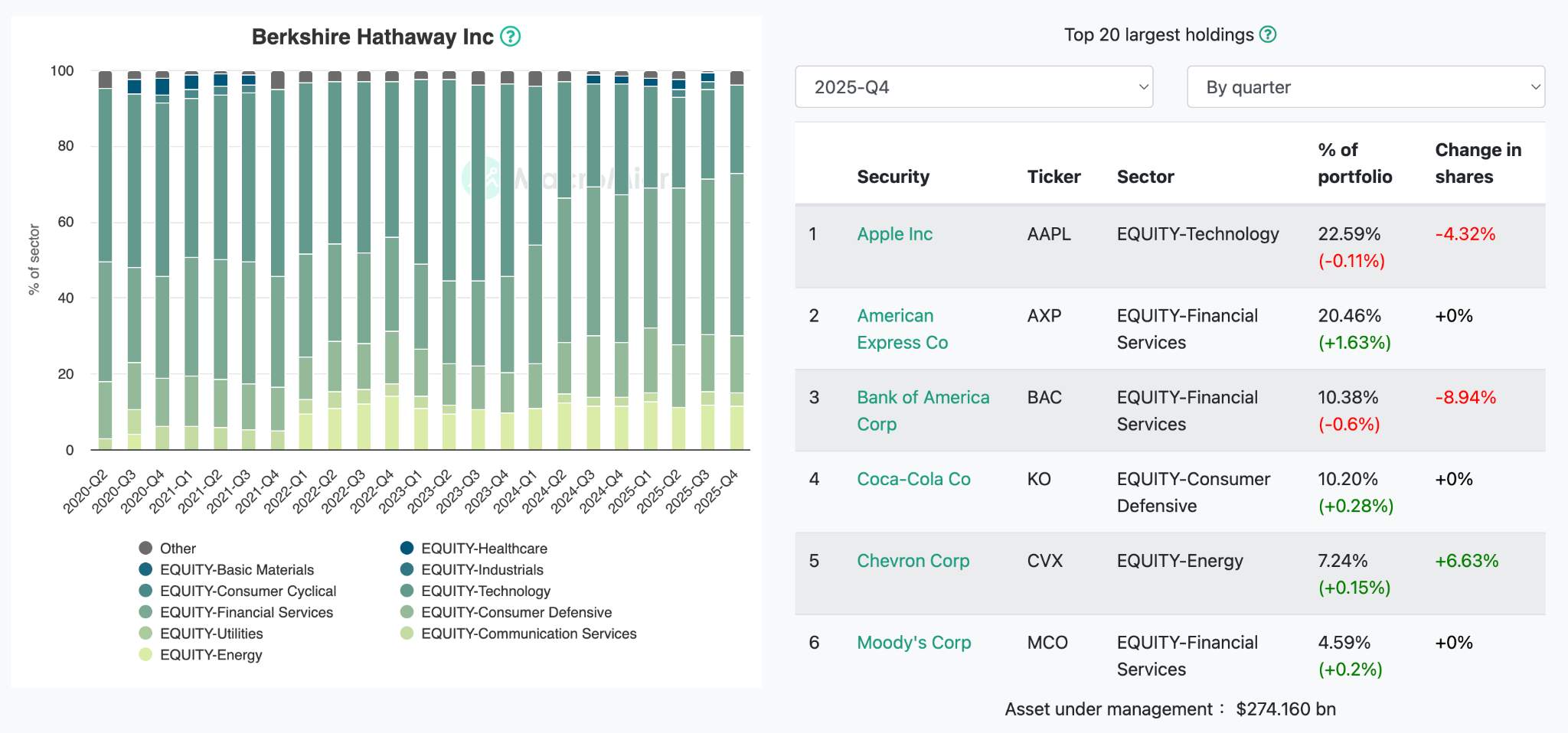

[Coca-Cola remains a top holding for Berkshire Hathaway; Source: Macromicro]

In his first shareholder letter, Berkshire Hathaway's new CEO Greg Abel listed Coca-Cola as one of the company's four 'core holdings,' explicitly implying they are 'permanent,' which serves as the most direct endorsement of Coca-Cola's moat.

Abel pointed out that these companies are entities that Berkshire 'fully understands, highly recognizes their management, and expects to continue compounding growth for decades.' Based on Berkshire's acquisition cost of approximately $3 per share, the compound growth rate of the Coca-Cola holding over decades validates the consumer giant's ability to weather economic cycles.

Repricing Defensive Assets under AI Transformation

On March 31, ET, current COO Henrique Braun officially succeeded James Quincey as CEO, while Quincey transitioned to Executive Chairman. During the handover, Quincey stated: "The AI era brings massive transformation, and the company needs a leader with the abundant energy required to drive this next phase of evolution."

Coca-Cola is advancing AI integration across multiple scenarios:

- Leveraging generative AI to accelerate creative production and A/B testing—achieving precise targeting that is expected to enhance marketing ROI and the success rate of new product launches.

- Utilizing AI machine learning for demand forecasting, inventory allocation, and transportation scheduling to reduce stockouts and excess inventory, thereby improving working capital turnover and gross margins.

- Applying AI-assisted price elasticity analysis, promotional depth, and packaging mix design for precise execution across various channels, magnifying pricing power without sacrificing volume.

From a financial perspective, Coca-Cola expects 2026 adjusted revenue growth of 4%–5%, non-GAAP EPS growth of 7%–8%, and free cash flow of approximately $12.2 billion.

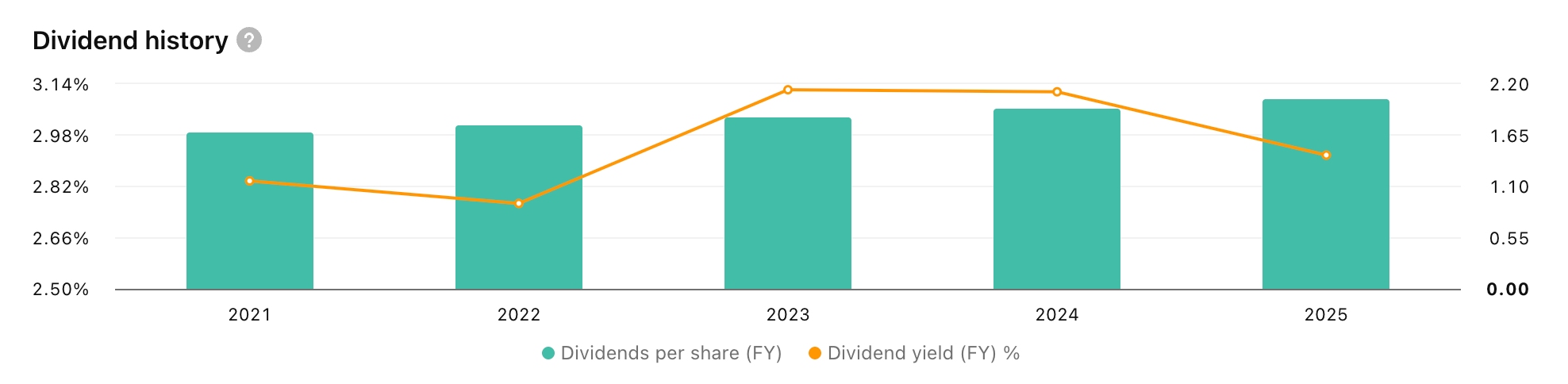

Notably, dividends have increased for over 60 consecutive years, with an annualized dividend yield of approximately 2.92% for 2025. Supported by a massive cumulative free cash flow base of over $70 billion, AI investments remain well within a manageable range.

Overall, the upcoming Q1 earnings report is likely to deliver a scorecard of "revenue in line with expectations, EPS near the upper end of guidance, and steady performance outlook."

In a macro environment where risk-aversion sentiment continues to rise, Coca-Cola remains resilient, supported by a moat built on brand pricing power, a global operating network, and steady cash returns.

The market will further test whether this century-old beverage giant can continue to deliver on its "cycle-defying" promise under new leadership and in the age of AI.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.