How to Navigate the War in the Middle East: the Trades You Need to Know

AI Podcast

The Middle East conflict has driven Brent Crude to a four-year high, impacting global economic narratives. While oil and defense sectors are first-order trades, second-order opportunities in shipping, insurance, and aviation are emerging. Tanker equities have declined despite soaring freight rates, indicating pricing dislocation due to operational risks. Maritime war risk insurance premiums have quadrupled, yet insurers' equities remain stable, suggesting mispriced risk and potential for underwriting margin expansion. The aviation industry faces headwinds from high fuel costs and demand destruction, creating opportunities in aircraft lessors and maintenance providers. Investors should focus on durable earnings tailwinds in these less crowded segments.

TradingKey - Over recent weeks, war in the Middle East has shone the spotlight on oil prices. Brent Crude has surged 65% to briefly cross $119 per barrel, a four-year high.

Amid shipping disruptions in the Strait of Hormuz, damage to energy infrastructure across the Middle East, and the looming threat of a ground conflict, the economic narrative of the war centres on what higher oil prices might mean for the global economy.

Meanwhile, the defence sector also commands attention during geopolitical conflict. While defence spending tends to follow conflict with a lag, war typically sees an increase in procurement of weapons, aircraft, missile and defence systems, and generally leads to higher forward spending commitments by governments.

However, for all the focus on oil and defence equities, these are widely followed sectors expected to benefit as ‘first-order’ trades.

Understanding second-order trades in the midst of geopolitical conflict

Amid the volatility and price disturbances tied to first-order trades, ‘second-order’ opportunities often follow. The market is typically more efficient at pricing first-order shocks - especially when it comes to oil - so investors often look past associated ripple effects.

Second-order forces tend to be somewhat removed from immediate market shock. Trades in adjacent segments of the market tend to be less crowded, but may represent compelling trades, whether that be due to mispriced risk, or valuation disconnect.

The easiest way for investors to understand the second-order implications of the war is to consider the disruption to supply chains, manufacturing processes, and business operations.

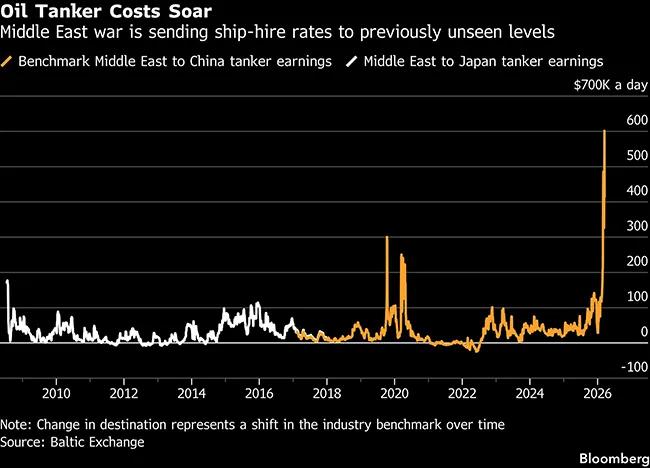

Shipping tankers hold tactical tailwinds, but are currently underperforming

The Strait of Hormuz is responsible for carrying approximately 20% of the world’s oil supply. With the critical waterway effectively shut - prompting the largest supply disruption in the history of the global oil market - the tanker industry is positioned at an intriguing juncture, showing signs of pricing dislocation. More specifically:

● Effective tanker supply in the Middle East has significantly decreased;

● Freight spot rates have surged higher, notwithstanding recent easing; yet

● Tanker equities are sharply lower since the start of the war

Investors have discounted tanker equities due to operational disruptions, attacks, and risks confronting tankers in the Strait of Hormuz. In effect, the market is anticipating that while spot prices are higher, there will be far fewer voyages owing to idle ships and those avoiding the region.

However, even if the conflict subsides quickly, the International Energy Agency (IEA) expects shipping disruptions to last months, without considering the risk of further geopolitical conflict.

The delays and higher costs in moving product during geopolitical conflict tend to linger beyond the resumption of flows, with markets constrained by significant pent-up demand for tankers. This supports elevated freight spot prices beyond the short-term, while even shielding the oil tanker segment from the longevity of heightened oil prices.

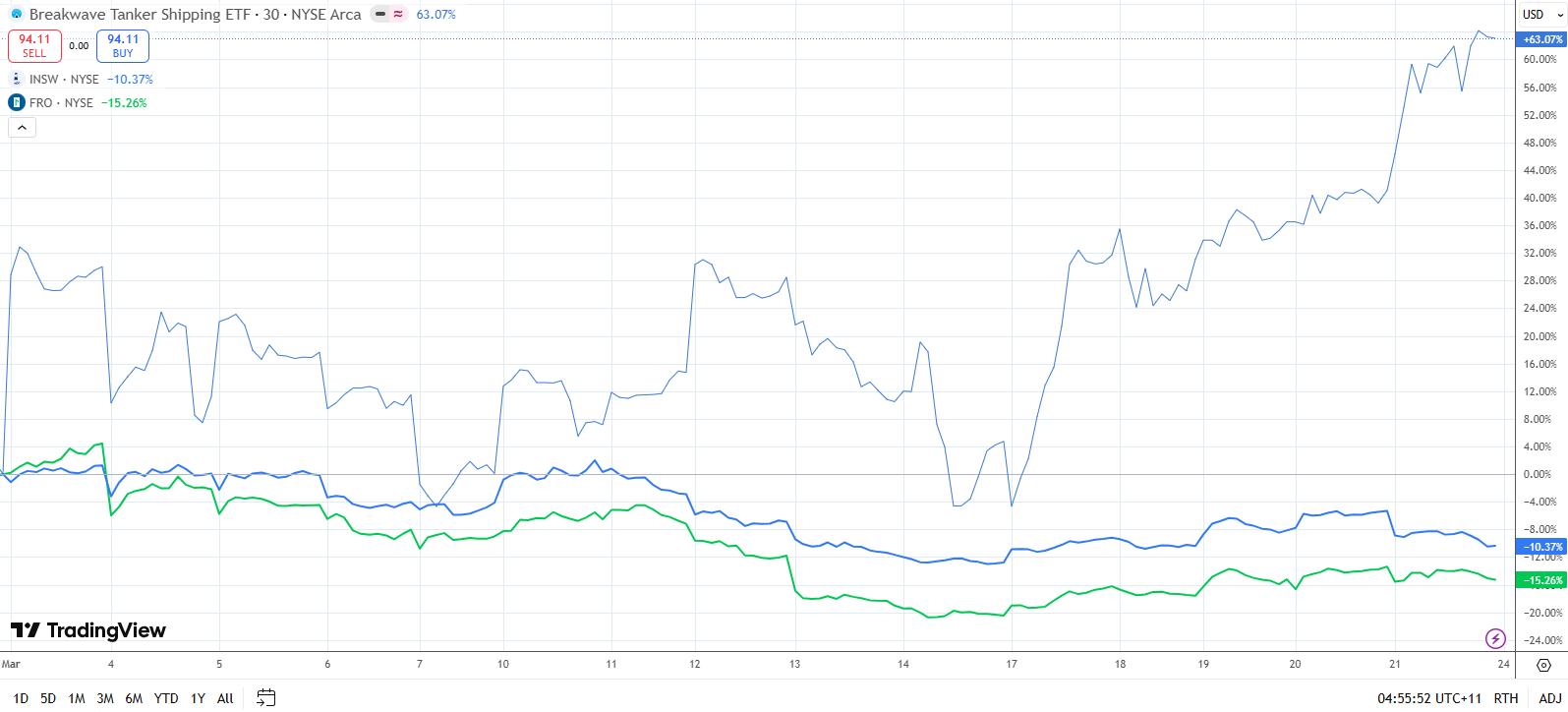

Tanker equities International Seaways (INSW) and Frontline (FRO), both highly leveraged to spot freight prices, have declined 10.4% and 15.3% respectively during the first three weeks of the war. It should be noted, shipping equities recorded strong gains in the lead-up to the war. But the Breakwave Tanker Shipping ETF (BWET), which tracks futures for oil tanker freight rates, has soared over 60%, highlighting asymmetry and pricing dislocation between expectations and news flow.

Source: Tradingview.com

Nonetheless, current market signals suggest the tanker segment could be in keeping with a tactical opportunity centred on:

● Selective consideration at a stock level given recent pullbacks;

● Segment tailwinds detailed above; and

● Further upside potential tied to earnings durability based on how long the war lasts

The risk premium upside of war time insurance

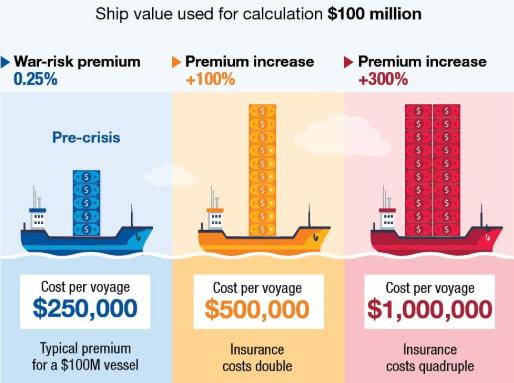

As with any bout of geopolitical instability, risk becomes a more pressing theme. During war, not only do premiums for war risk insurance increase, but there is typically greater demand for insurance. In the context of the Middle East conflict, tankers are again in focus. However, this time it is the insurance ‘backstop’ that affords investors asymmetric opportunities exhibiting pricing dislocation.

Maritime insurance war risk premiums have more than quadrupled over recent weeks, from approximately 0.25% of vessel value to as high as 1-1.5%. This reflects risk being repriced by insurers. Still, investors have not exhibited a similar appetite to reprice risk in this sector, despite strong tailwinds supporting the earnings bases of relevant insurers. These tailwinds include:

● Insurance coverage being a necessity for maritime shipping operators;

● A high issuance of rewritten policies since the start of the war

Source: UN Trade and Development

While the US features no pure-play marine insurers, diversified insurers such as American International Group (AIG) and Chubb (CB) - both of which have exhibited relatively stable performances since the start of the war - offer exposure to this segment and stand to benefit. If anything, investors have focused on the risk of forthcoming claims from the conflict, rather than an uplift in premiums.

Current pricing dislocation points to a view where investors may see rising premiums as a temporary tailwind for insurers. However, the magnitude of the conflict, and the likely lingering geopolitical strain across the region - also feeding into global shipping, where insurers are leveraged to higher earnings, even if marine traffic drops - give rise to industry changes being more structural in nature.

Accordingly, pricing dislocation in the insurance sector is confined to specific equities and is less visible than other market segments, but with less emphasis attached to timing, and more on fundamentals. Should the war drag on, or geopolitical tension remains elevated:

● Underwriting margins should see material expansion;

● Insurers would have flexibility to cancel war risk cover and promptly reprice risk; and

● Insurers are generally sheltered by a lag on claims

What rising costs and demand destruction mean for the aviation industry

With oil prices a sensitive input for airlines (fuel costs), the price shock ensuing from war in the Middle East represents a significant headwind for the aviation industry. Simultaneously, with air routes impacted, and broader cost-of-living pressures influenced by high fuel prices, the industry faces demand challenges.

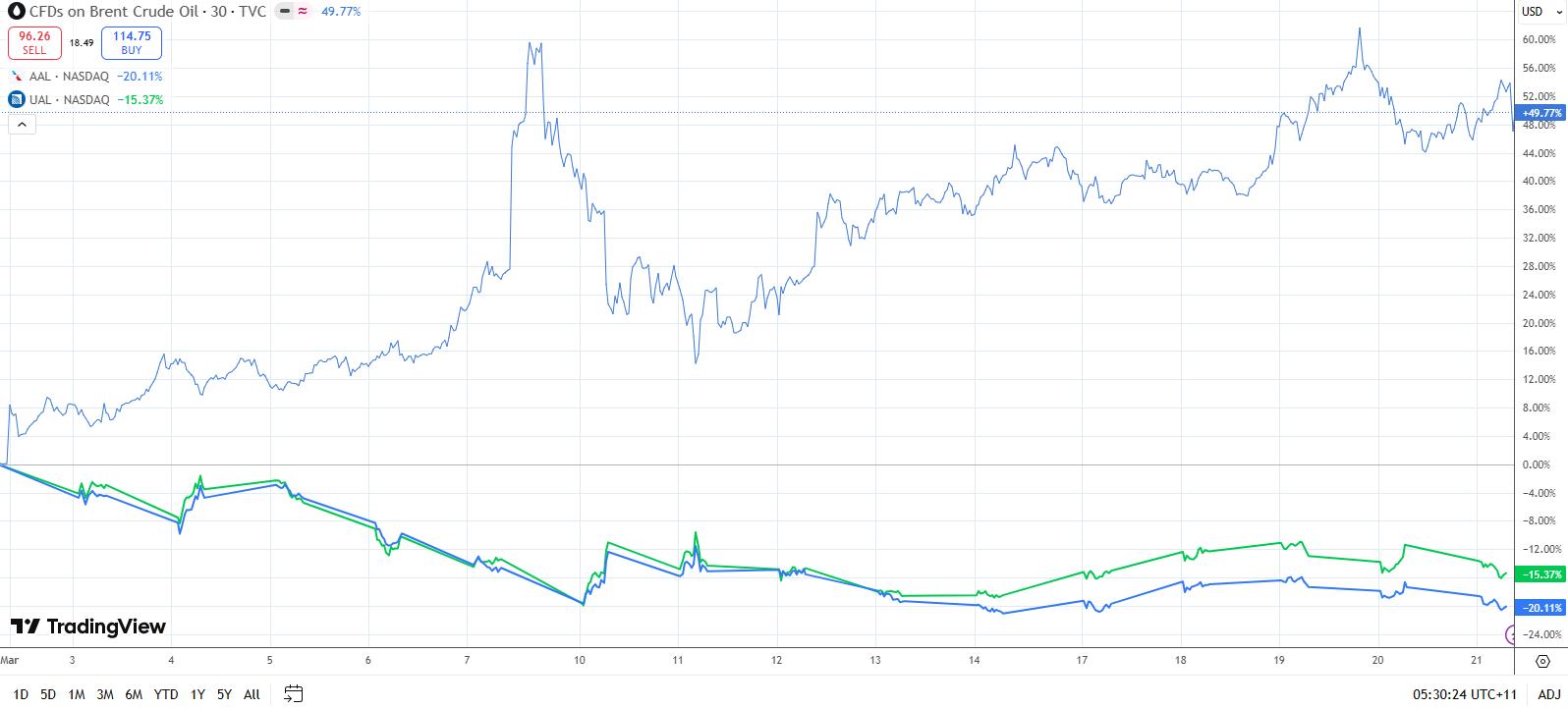

From an equities perspective, airlines underperform during heightened geopolitical conflict and rising oil prices. Investors typically discount for uncertainty with regards to forward bookings and sector margins. This often extends to airlines far removed from conflict zones. For example, American Airlines (AAL) and United Airlines (UAL) have declined 20.1% and 15.4% over recent weeks, but rallied briefly during periods where Brent Crude prices retreated.

Source: Tradingview.com

Much of this discounting typically occurs in the early stages of a major geopolitical conflict, which is when investors may wish to reposition ‘short’. But it is not the only opportunity for a short thesis. For example, subsequent periods where oil prices stabilise sometimes prompt equities rallies - even in the face of depressed travel demand - and these moments sometimes illustrate pricing dislocation supportive of a bearish outlook.

For contrarian investors, attractive entry points for long positions may emerge if there are signs that higher oil prices are only likely to prompt a temporary adjustment in fuel prices. In this instance, the narrative for demand destruction holds far less conviction, as was the case during the pandemic.

A more removed second-order trade in this segment relates to aircraft lessors and maintenance providers. A deteriorating industry outlook gives rise to margin pressures that one might reason are likely to prompt a deference in aircraft purchases. In turn, this may translate to:

● An extension in the operating life of existing air fleet;

● Greater demand for leasing aircraft, as opposed to purchasing new fleet; and

● Increasing demand for aircraft maintenance services

The asymmetry and opportunity in second-order trades

While investors may be inclined to follow visible yet crowded opportunities, second-order trades have the potential to be just as lucrative as the market’s first move.

In an environment defined by high friction and uncertainty, the ripple effects of the war in the Middle East give rise to potential pricing dislocations. Disruptions to the shipping and aviation industries present opportunities guided by recent valuation pullbacks, while a repricing of risk in the insurance industry offers an investment backdrop defined by resilient momentum.

For investors, important lessons through geopolitical conflict are:

● Obvious trades can be crowded and unreliable due to the narrative

● Obscure trades can be dictated by timing and a lag in price discovery

Nevertheless, in times of war investors should pay attention to the durability of earnings tailwinds as a calming in geopolitical tensions could unwind the asymmetry that underpins second-order trades.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.