US Stocks Crash This Week, But Trump’s China Visit May Spark a Short-Term Rally

AI Podcast

Rising recession risks, amplified by U.S.–Iran tensions and higher energy prices, are overshadowing AI enthusiasm. Despite strong demand for AI hardware from companies like Nvidia and Micron, with memory prices set to rise, macroeconomic data points to increasing recessionary pressures. However, President Trump's upcoming China visit offers a potential short-term boost, with historical precedents suggesting potential benefits for aerospace and agriculture sectors. U.S. equities typically show pre-midterm weakness followed by post-election gains, with market sentiment now heavily influenced by the outcomes of Trump's diplomatic efforts. Volatility is expected to persist due to Trump's policy style.

TradingKey - The week opened to a familiar sense of unease across Wall Street. History, hard data, and the destructive aftershocks of renewed U.S.–Iran tensions have converged to point toward rising recession risks. For all the enthusiasm around artificial intelligence investment, that optimism looks too slight to offset the shock of higher energy prices — and markets are starting to reflect it.

Even though America’s oil and gas output now roughly matches domestic demand, the global energy picture has darkened. Investors worry that a tightening macro environment would not leave the AI boom untouched; capital expenditure in cutting‑edge computing might slow just as enthusiasm peaks.

AI Can’t Offset Rising Recession Risks

The technology narrative continues to supply its own bursts of excitement. Nvidia (NVDA)’s Jensen Huang took the stage at this week’s GTC conference to a rapt audience, unveiling what he called a trillion‑dollar order pipeline. Demand, he said, “still far exceeds supply”, with fresh orders driven less by hyperscale cloud providers and more by corporate‑level deployments of AI inference — a market reaching what he described as an inflection point. Deploying trillion‑parameter models requires enormous pools of low‑latency computing power, and Huang touted Nvidia’s architecture as “the world’s lowest‑cost infrastructure”, extending product life cycles while keeping running costs down.

Elsewhere in the semiconductor ecosystem, Micron (MU) added its own proof of resilience. The memory‑chip maker’s quarterly results beat market expectations by a wide margin, a vivid confirmation that storage demand from AI applications continues to surge. Chief executive Sanjay Mehrotra called memory “a strategic asset for AI”, revealing the firm’s first five‑year supply contract and announcing that its latest HBM4 chips would go directly into Nvidia systems.

Together with industry leaders Samsung and SK Hynix, Micron’s message underscored the scale of AI demand. The three companies’ capacity is effectively booked out through 2027 by AI‑related orders, with HBM memory prices expected to rise by 53 per cent in 2026 as inference workloads — roughly three times more power‑hungry than training — drive the next phase of hardware expansion. The supply shock perfectly complements Nvidia’s trillion‑dollar forecast.

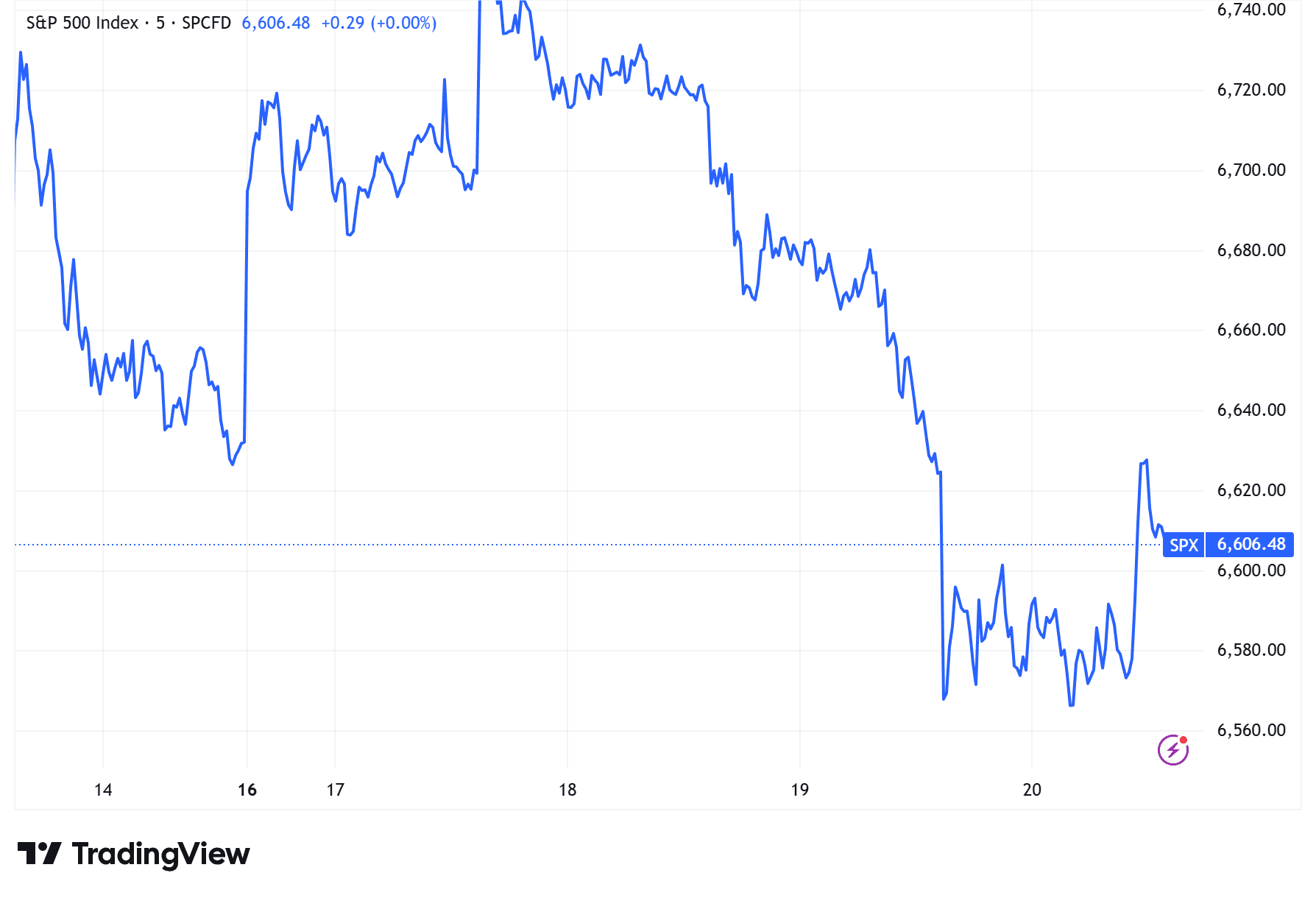

Yet against this backdrop of technological abundance, the macro data remain bruising. Recent employment and inflation readings, coupled with oil’s relentless climb after the Iran conflict, all point to heightened recession risk. The S&P 500 registered three consecutive days of declines this week.

Trump’s China Visit Offers Short-Term Boost

Still, not all catalysts are negative. The prospect of President Trump’s upcoming visit to Beijing has become an important emotional anchor for markets, with some traders betting that the renewed dialogue between Washington and Beijing could translate into a brief relief rally.Many see the trip as a signal that 2026 might mark a year of moderation in U.S.–China relations. Since Washington paused part of its tariff regime in 2025, both sides have had strong incentives to stabilise trade. Memory runs back almost a decade: during Trump’s 2017 visit, U.S. and Chinese companies signed cooperation deals worth $253.5 billion, triggering a broad global equity bounce.

If history offers any guidance, aerospace may again be a beneficiary. In 2017, the visit brought a headline agreement for 250 Boeing 737 MAX jets; today, China still represents around 30 per cent of Boeing’s deliveries. New contracts could lift the company’s order book by as much as 15–20 per cent.

The agriculture sector also looms large in the political calculus. With the midterm elections approaching, Trump has every reason to showcase trade “wins” to voters in the Midwest, where farm states can decide the outcome. Renewed Chinese purchases of soybeans and corn would provide low‑cost proof of success. After exports to China were halved in 2025, companies such as Archer Daniels Midland (15 per cent of sales to China) and Bunge, the world’s second‑largest grain trader, remain highly sensitive to tariff‑waiver expectations; the confirmation of multi‑year contracts during the visit could materially lift revenue visibility into the next fiscal year.

Energy trade could add a further layer of alignment. The ongoing U.S.–Iran confrontation has paradoxically strengthened America’s position as the world’s top liquefied‑natural‑gas exporter. For Cheniere Energy, the country’s largest LNG producer, signing long‑term supply deals with Chinese buyers could connect Washington’s export interests with Beijing’s growing power needs — a scenario that would ease pressure on the U.S. electricity grid and support the domestic AI industry’s hunger for energy.

U.S. Stocks Outlook Tied to Trump’s Midterm Influence

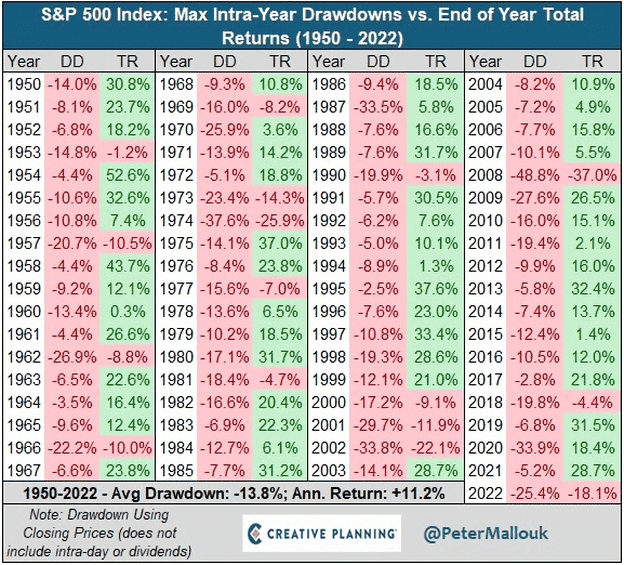

Looking to history again, U.S. equities tend to falter ahead of midterm elections before finding their footing afterward. Over the past century, the S&P 500’s average peak‑to‑trough decline in midterm years has been 18 per cent, with pre‑election pullbacks of 10 per cent or more common. Yet in the three months following the vote, the index has typically risen 5.8 per cent, and nearly 15 per cent over the following year.

In the near term, expectations surrounding Trump’s China trip have become the market’s key mood catalyst. Any rebound will hinge on the concrete outcomes announced — and investors will be watching the April window for policy signals.

As the 2026 midterm season draws closer, volatility is likely to rise, not least because Trump’s policy style remains as combustible as ever. Ed Clissold, chief strategist at Ned Davis Research, has a term for it — the “Big Mac Trade,” a play on words marking the approach of the midterms. He expects a chain reaction to unfold around the autumn vote.

Trump himself is already focusing on everyday costs ahead of the campaign: oil prices, mortgage rates, credit‑card interest, and the federal funds rate have all come under rhetorical fire. Each announcement has sent tremors through financial stocks. His habit of governing by social‑media blast ensures that nearly every pronouncement has the power to jolt multiple sectors — keeping volatility, for now, a feature rather than a bug of the Trump‑era market cycle.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.