The Great SaaS Divergence: Why B2C SaaS are Built Differently

AI Podcast

The software industry faces disruption from AI, challenging traditional SaaS models. B2B SaaS, historically valued for utility and ROI, is vulnerable as AI offers cheaper functionality, eroding its "middleware" moat. Revenue growth for B2B leaders is declining. In contrast, B2C SaaS, driven by emotion, habit, and identity, enjoys stronger moats. Daily rituals, pricing resilience, and diverse monetization strategies protect B2C companies. Infrastructure-focused B2B niches, such as cybersecurity and data analytics, are also positioned to survive. The future favors software deeply integrated into user identity and daily life.

The software industry is currently navigating its most turbulent era since the dawn of the cloud. For over a decade, Software-as-a-Service (SaaS) was the undisputed darling of Wall Street, characterized by astronomical valuations and the promise of endless recurring revenue. However, the market has recently undergone a significant correction, with software stocks crashing as investors rethink the long-term viability of the traditional SaaS model.

The primary catalyst for this shift is Artificial Intelligence, a technology so disruptive that it threatens the very foundation of how software companies extract value. While the industry is far too broad to disappear entirely, its future landscape will look radically different than the past.

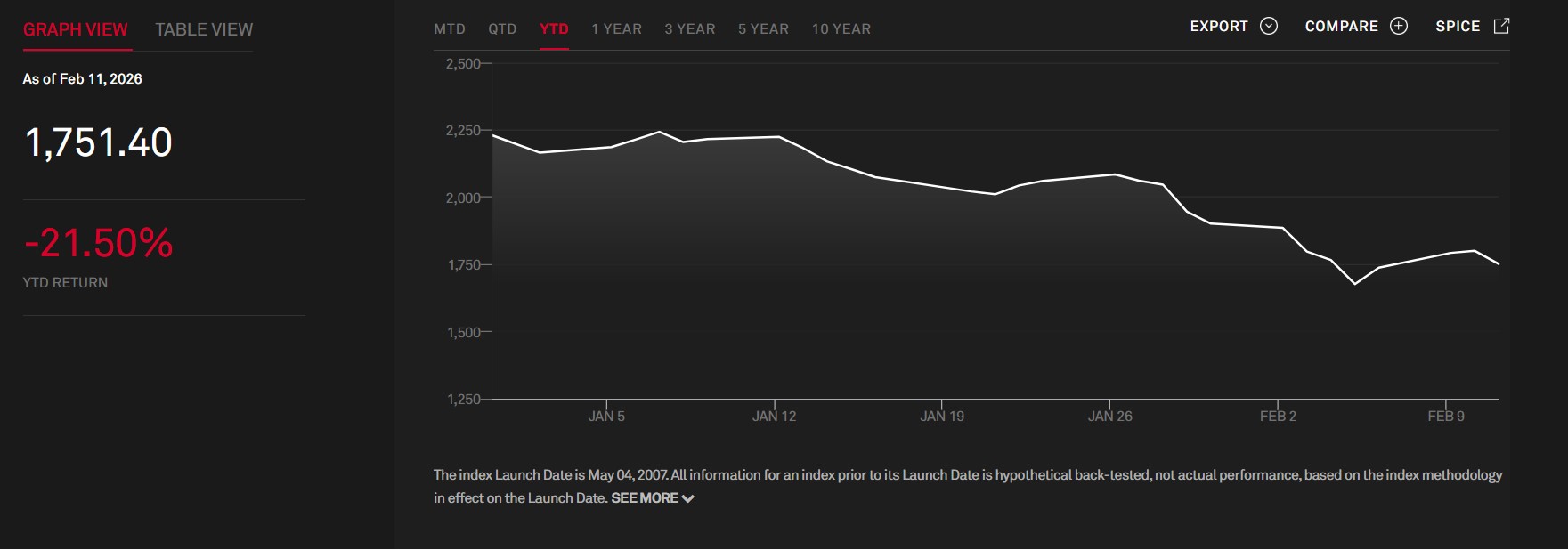

Equity U.S. Equity S&P Sectors S&P North American Technology Software Index (Source: S&P Global)

The AI and the Commodity Trap

The central threat AI poses to software is the erosion of the "middleware" layer. Historically, software served as the essential interface between complex data and the end consumer. However, as AI makes it increasingly cheap and efficient to build custom software, the justification for paying high subscription fees for standard applications begins to vanish. If a big AI scaler can provide the functionality of a complex application at marginal or zero cost, the traditional SaaS moat evaporates.

This pressure is already manifesting in the financial performance of major B2B players. A look at recent revenue growth trends reveals a consistent downward trajectory for many enterprise leaders.

Company | 2022 | 2023 | 2024 | 2025 (Projected/FY) |

Salesforce (CRM) | 24.70% | 18.30% | 11.20% | 8.40% |

Adobe (ADBE) | 11.50% | 10.20% | 10.80% | 10.50% |

ServiceNow (NOW) | 22.90% | 23.80% | 22.40% | 20.90% |

Workday (WDAY) | 19.00% | 21.00% | 16.80% | 16.40% |

Source: SEC Filings

B2B is a Math Problem; B2C is a Relationship

While the recent market turbulence might lead some to wonder if we are witnessing the end of SaaS, the short answer is no. The industry is far too broad, consisting of numerous companies with diverse business models and strategies solving a vast array of problems, making it simply impossible for the entire sector to disappear.

However, the landscape will be fundamentally different moving forward. To understand this evolution, we must look for specific "green flags" or moats that indicate a company's readiness for the AI revolution.

A helpful way to view the sector is by classifying it into two broad groups: B2B SaaS, which serves business customers—such as Salesforce, Adobe, ServiceNow, and Workday—and B2C SaaS, which provides services to end consumers—like Spotify, Netflix, and Duolingo. This B2C category can even extend to tech giants like Uber and DoorDash, which, while not traditional SaaS, share similar consumer-facing dynamics.

Though B2B has historically been viewed as the more stable, lucrative bet due to high switching costs and enterprise budgets, the AI revolution suggests a reversal of fortunes. In this new paradigm, B2C giants like Spotify and Netflix may actually have a higher chance of survival than enterprise stalwarts like Salesforce and ServiceNow.

B2B is a Math Problem; B2C is a Relationship

Metric | B2C (Entertainment/Consumer) | B2B (Enterprise/Utility) |

Why we buy | Emotion, Habit, Identity | ROI, Efficiency, Compliance |

Switching Effort | Low, but "Why bother?" | High, but "The savings are millions!" |

AI Threat | High (Content generation) | Terminal (Model-as-a-Service) |

Safety Net | Ad Revenue / Attention | None (Value-extract only) |

The reason B2B is more vulnerable to AI disruption lies in the fundamental nature of the customer relationship. B2B software is primarily sold on the back of utility—it is designed to improve ROI, increase efficiency, or ensure compliance. Because corporations are rational actors, their commitment to a software suite is essentially a mathematical calculation. If a generative AI model can perform the same task for a fraction of the price, a business will switch, even if the effort to move is high. In the enterprise world, savings of millions of dollars justify the headache of a platform migration. For many of these companies, the threat is "terminal" because they risk being replaced by Model-as-a-Service providers.

In contrast, B2C SaaS operates on emotion, habit, and identity. Consumers do not use Spotify or Netflix because it improves their personal "efficiency" or "compliance." They use these platforms for enjoyment, personal fulfillment, and entertainment. While the switching effort for a consumer is technically low—canceling a subscription takes two clicks—the emotional barrier is "Why bother?". This lack of strict rationality in consumer behavior creates a protective buffer against AI. AI can solve a math problem, but it has a much harder time disrupting a deeply ingrained personal relationship or a daily ritual.

The Moat of Daily Rituals and Pricing Resilience

The strength of the B2C model is best illustrated by the concept of "daily religious rituals". Platforms like Duolingo, Spotify, and Netflix have successfully integrated themselves into the fabric of daily life. Duolingo utilizes gamification and the fear of "breaking the streak" to maintain a daily active user rate of 37% to 40% among its 50 million users. Spotify serves as the "soundtrack" to life, acting as a utility for 330 million people during commutes, workouts, and work hours, boasting a 44% daily usage rate. Netflix, while having a slightly lower daily rate of 30%, maintains the highest time spent per session at over 60 minutes, serving as the universal "wind-down" moat for the modern consumer.

Company | Daily Active Users (DAU/MAU) | Why it’s so high |

Duolingo | 37% – 40% | The "Streak" Moat: Gamification and the fear of "breaking the streak" turn it into a daily religious ritual for ~50M users. |

Spotify | 44% | The "Soundtrack" Moat: Music is the background of people's lives (commutes, gym, work). ~330M people use it as a daily utility. |

Netflix | ~30% | The "Wind-Down" Moat: While it has the lowest daily rate of the three, it has the highest time spent (60+ mins per session). |

Furthermore, the pricing structures of B2C platforms offer a layer of protection that B2B lacks. For the average American with a median annual income of $62,000, B2C subscriptions are relatively inconsequential to the monthly budget. A Netflix account ranges from $7.99 for the ad-supported tier to $24.99 for premium, while Spotify and Duolingo offer plans starting around $10 to $13 per month. Because these costs are low, consumers are less likely to hunt for "AI-generated" alternatives to save a few dollars.

B2B pricing, conversely, is often based on "per-seat" licenses, which are highly vulnerable in an AI-driven economy. It is common for medium-sized enterprises to pay $500,000 annually for Salesforce. As AI automates tasks, companies may require fewer employees, leading to a direct reduction in "seats" and a significant shrinkage in SaaS revenue. To survive, these companies must transition to usage-based pricing, a move that is fraught with financial uncertainty.

Company | Plan Type | Monthly Price (USD) |

Netflix | Standard with Ads | $7.99 |

| Standard (Ad-free) | $17.99 |

| Premium (4K) | $24.99 |

Spotify | Individual | $12.99 |

| Duo | $18.99 |

| Family | $21.99 |

Duolingo | Super (Monthly) | $12.99 |

| Super (Annual) | ~$6.99/mo |

| Duolingo Max | $29.99 |

Physical Assets and Diversified Monetization

Perhaps the most significant "green flag" for B2C companies is their connection to non-software assets. While many B2B companies are just software layers over data, B2C leaders have fortified their positions with physical and proprietary assets. Netflix has invested heavily in original IP and production assets, and Spotify maintains critical partnerships with major music labels. Similarly, B2C tech companies like Uber and DoorDash—while not pure SaaS—possess massive networks of millions of drivers and restaurants alongside proprietary logistics data.

B2C companies also have more flexible monetization strategies. They can pivot between subscription models and advertising models to capture value, a transition already being executed by Netflix and Spotify. B2B companies, which generally lack an "attention" or "ad revenue" safety net, must rely almost exclusively on extracting value from the utility they provide.

The Infrastructure Exception in B2B

This is not to say that all B2B SaaS is doomed. The companies best positioned to survive are those occupying "Infrastructure" niches rather than "Application" roles. Security-focused firms like CrowdStrike (CRWD) and data-centric companies like Datadog (DDOG) provide services that are essential to the operation of a modern business. You can fire a salesperson and lose a Salesforce seat, but you cannot "fire" your security guard or your electric meter. In fact, the AI revolution creates more security risks and more data, making these "boring" B2B infrastructure stocks safer and more relevant than their application-based counterparts.

In conclusion, the AI revolution is forcing a massive re-evaluation of the software sector. While B2B companies face a "math problem" that AI is increasingly equipped to solve, B2C companies are protected by emotional moats, daily habits, and tangible assets. The future of SaaS belongs not to the companies that provide the most efficient layer between data and the user, but to those that have become an indispensable part of the user's identity and daily life.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.