Microsoft FY26 Q1: Azure's AI-Powered Surge Meets $35B Capex Shockwave—OpenAI Pact Secures the Future

Core Takeaway

Microsoft’s fiscal 2026 Q1 results beat expectations for both revenue and EPS, powered by sustained demand in Azure and AI-driven cloud services. However, the headline beat was tempered by record capital expenditures—at $34.9 billion, far exceeding forecasts, which immediately raised concerns over margin and cash flow pressure. Adding to the uncertainty, management did not provide explicit full-year profit guidance, leaving investors to question how sustainable profitability will be as capital investment ramps further.

This push-and-pull triggered sharp volatility: the stock initially fell nearly 4% in after-hours trading as investors reacted to the Capex shock and lack of earnings visibility. As the call progressed and management walked investors through the AI backlog, Azure’s forward momentum, and the deeper logic for their AI factory capital cycle, the shares managed to claw back those early losses, with some seeing the long-term upside in Microsoft’s leadership position. But as the market digested both the scale of spending and tougher questions about payback timing and competitive dynamics, the shares slid again, ultimately down over 3%. Investors are clearly impressed by the company’s operational strength, but not all are convinced that massive AI-era spending will translate to near-term returns, especially with no detailed earnings roadmap for the rest of the year.

Source: Yahoo Finance

Financial Deep Dive: Capex and Cloud Lead the Story

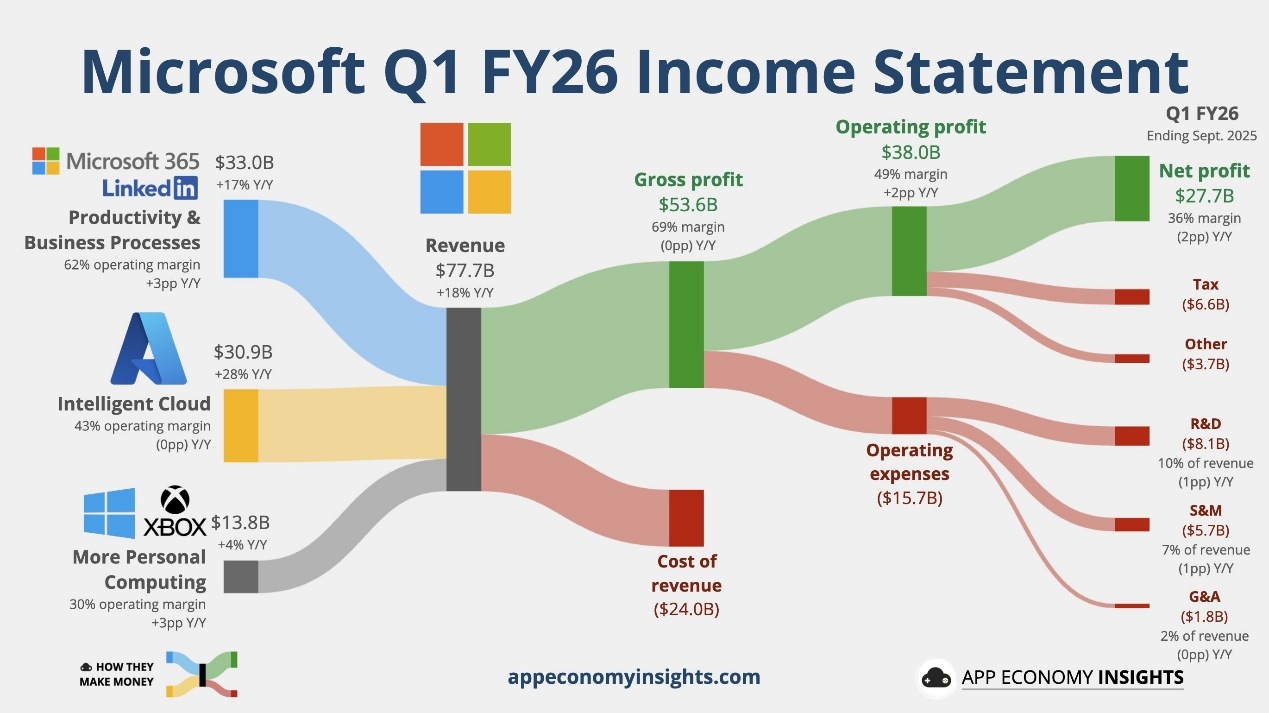

Microsoft delivered another robust quarter, with total revenue hitting $77.7 billion, up 18% year-over-year, and operating income jumping 24% to $38.0 billion. The margin story remained impressive—gross margin was strong at 69%, with operating margin holding near 49%, thanks to the growing mix of high-value cloud and productivity services.

Source: App Economy Insights

But the real headline was Capex: Microsoft poured $34.9 billion into capital expenditures this quarter—a staggering 74% YoY increase, and well ahead of expectations. Management made it clear this isn’t a one-off spike: full-year FY26 Capex is now set to outpace FY25, marking a full-throttle, multi-year expansion in data center and AI infrastructure.

On the demand side, the numbers speak for themselves. Commercial RPO reached a towering $392 billion, up 51% YoY, as customers lock in long-term cloud and AI commitments. Nearly half of FY26 Q1’s capex went toward GPU/CPU assets to support accelerated cloud and AI workloads. Microsoft aims to boost AI datacenter capacity by 80% just this year and nearly double its data center footprint within two years, a bold bet that AI-driven cloud workloads are only getting started.

Metric | Q1 FY2026 | Consensus | YoY Change | Beat/Miss | Commentary |

Revenue | $77.7B | $75.3B | +18% | Beat | Stronger Azure and Cloud, trend accelerating |

Operating Income | $38B | – | +24% | – | Margin ~49%, driven by cloud mix |

EPS | $3.72 | $3.66–3.67 | +13% | Beat | Non-GAAP EPS: $4.13 |

Azure Revenue YoY Growth | +40% +39% (constant currency)

| +37% (constant currency) | – | Beat | Slight deceleration |

Capex (Total) | $34.9B | $30B | +74% | Beat | Record spend, focus of investor debate |

Commercial RPO | $392B | – | +51% | – | Reflects strong AI/cloud demand pipeline |

Source: Microsoft, TradingKey

Microsoft’s numbers tell a simple story: aggressive, conviction-led scaling in AI and cloud infrastructure, with the financial strength to back it up.

Business Segment Breakdown: Azure Resilience, Copilot Expansion, Consumer Steady

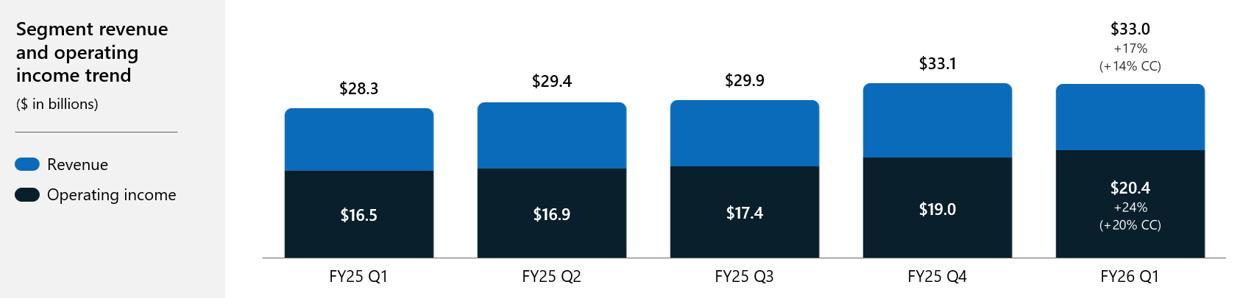

Intelligent Cloud (Azure and Services):The whole Intelligent Cloud segment put up another strong quarter. Segment revenue reached $30.9 billion, up 28% YoY—another sign that Microsoft’s leadership in cloud infrastructure and enterprise services isn’t letting up anytime soon. Azure continues to do the heavy lifting—revenue was up 40% YoY, and 39% in constant currency. While this more or less matched what buyside or the market were looking for, it wasn’t the kind of blowout number that moves the needle. The real market debate has shifted to the pace of future deceleration, as investors weigh how long Azure can keep running at this clip. AI demand, plus those headline OpenAI deals, kept backlog growth humming and helped anchor long-term confidence in the cloud story.

Source: Microsoft

Productivity & Business Processes:

This engine is steady and broad-based—Microsoft 365 Commercial revenue climbed 17%, Consumer leapt 26%, Dynamics jumped 18%, and LinkedIn tacked on 10%. Copilot is finally putting up real numbers: over 150 million monthly active users across its family of agents, with 90% of the Fortune 500 now on M365 Copilot and GitHub Copilot passing the 26 million user mark. The use case is there—information work, enterprise, coding—but real product-led breakout growth is still a work in progress, and some features arguably lag the hype.

Source: Microsoft

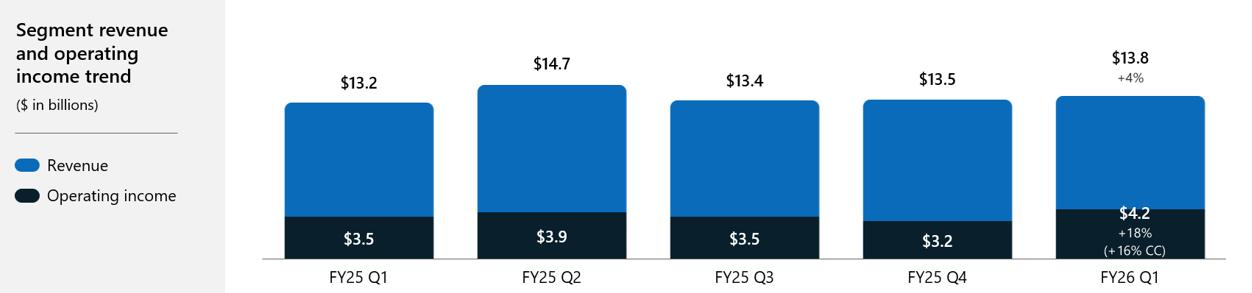

More Personal Computing:

Revenue here rose to $13.8 billion, up 4% YoY, driven by modest gains in Windows OEM/Devices (+6%), a slightly better Xbox performance, and solid double-digit growth in search and ad revenue. But make no mistake: this segment is miles behind Intelligent Cloud and Productivity in terms of contribution and narrative. The real action remains in the cloud.

Source: Microsoft

Strategic Highlights & Key Disclosures: OpenAI Agreement

This quarter marked a major evolution in Microsoft’s partnership with OpenAI—a deal that not only extends Azure’s exclusive relationship but also locks in a whole new layer of cloud commitment and IP rights that could shape the landscape for years. Microsoft and OpenAI signed a formal refresh of their agreement, pushing Azure’s service and IP exclusivity out to at least AGI or 2030 (for some rights, 2032), and bringing in an incremental $250 billion Azure cloud contract that still hasn’t shown up in the reported financials. The headlines focus on exclusivity and revenue, but as always, the details matter.

Key elements of the new Microsoft–OpenAI agreement:

・Azure maintains exclusive rights to frontier models and API products, at least until AGI is declared and independently verified, or through 2030–2032 for certain IP rights.

・Microsoft’s rights to product/model IP extend for two years post-AGI—covering new models and products after the official AGI milestone.

・OpenAI commits to an additional $250 billion Azure service contract, forming a massive multi-year pipeline for cloud consumption (not yet reflected in current numbers).

・Microsoft drops its previous right of first refusal to be OpenAI’s sole compute provider, acknowledging a shift to a more open ecosystem—but keeps exclusive hold on key models and API services.

・Microsoft retains its equity stake (~27%) in OpenAI and its central revenue/IP economics.

・OpenAI gains some flexibility to develop certain non-API products for other cloud providers and third-party collaborations—not a dramatic change, but formalized.

・API products developed with third parties will stay exclusive to Azure; non-API products can go multicloud.

・Microsoft is now allowed to independently pursue AGI—either alone or with other partners.

・OpenAI can provide API access to US government/national security customers on any cloud, broadening their reach.

・OpenAI is able to release open-weight models that meet certain capability criteria.

・Research IP rights have nuanced thresholds—Microsoft keeps deep rights to confidential research until AGI is verified or 2030, but not to consumer hardware.

This is a good deal for Microsoft. They still hold their OpenAI equity, retain the lion’s share of cloud and IP economics, and the shift to let OpenAI work with others essentially formalizes existing collaborations into the agreement, in the meantime not a hit to Azure’s dominant role. The real leverage is the sheer scale of dollar commitments and the sticky access to top-tier model IP, which fortifies Azure’s positioning in an increasingly multicloud world. With this update, Microsoft secures a multi-year lead as the AI infrastructure backbone—even as competitive dynamics evolve.

Guidance & Outlook

Microsoft forecasts that FY2026 Capex will grow at an even faster pace than FY2025, a major revision versus prior signals of a slowdown. This speaks to conviction in the durability of cloud/AI demand but leaves free cash flow subject to both execution and AI adoption rates.

Azure’s future growth hinges on:

・Sustained enterprise adoption of AI models and workloads,

・Continued integration of OpenAI technology and exclusivity,

・Effective monetization of RPO and backlog,

・Execution in data center expansion and supply chain management for GPUs and critical hardware.

Risks & Market Sentiment

Execution risk, competitive intensity (Amazon/Google), and uncertainty over AI hardware cycles remain front of mind. Heavy investment brings both opportunity and the threat of margin contraction if growth underwhelms or cost curves shift. Heightened Capex means less flexibility if cloud demand falters. And while the OpenAI contract gives a long-dated revenue line, its ultimate economics depend on usage patterns and industry trends.

Conclusion

Microsoft’s FY2026 Q1 paints a vivid picture of a company going all-in on the AI transformation, scaling both infrastructure spend and strategic alliances to reinforce its lead in the most critical growth verticals. Azure’s momentum is still very much intact, the newly refreshed OpenAI agreement locks in massive, sticky cloud demand, and management’s conviction comes through loud and clear in every line of Capex.

Valuation-wise, Microsoft remains expensive by historical standards and relative to peers: the stock trades at about 33x forward earnings, in line with Amazon (~34x) but at a significant premium to Google (~27x). That’s a clear leadership premium—investors are betting on Microsoft to keep outperforming in cloud and AI, but it does leave little room for disappointment if growth slows or margins get squeezed. The market is willing to look past record Capex today, but management needs to translate this investment into durable commercial returns and margin upside. The $135 billion equity stake in OpenAI is a strategic asset that reinforces the moat, but it won’t protect the stock price if AI momentum stalls.

At this valuation, the expectations are sky-high. Investors are paying up for AI dominance and Azure leadership, but with both competitive risk and execution pressure mounting, Microsoft needs to deliver on every front. The stock doesn’t offer much cushion—any slip in growth or profitability, and the narrative could flip quickly. Leadership in AI is Microsoft’s to lose, but the bar for execution is only getting higher.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.