CoreWeave (CRWV): Is This AI Cloud Powerhouse the Smart Buy Right Now?

Executive Summary

TradingKey - CoreWeave is a specialized AI infrastructure company delivering rapid access to advanced Nvidia GPUs and liquid-cooled clusters, with client demand exceeding current supply. Multi-year take-or-pay contracts and a large backlog underpin strong revenue growth, but results remain dependent on a small group of major customers and are supported by high leverage and aggressive CapEx. Its contract-first model creates a timing gap—cash and debt up front, revenue recognized over time—requiring disciplined execution and utilization. The investment case is high-upside for those bullish on AI and comfortable with build-phase volatility; accumulation below $90 is attractive, with a 12-month price target of $115–168 if deployment and utilization trends hold.

Source: TradingView

Company Overview

CoreWeave is a purpose-built Infrastructure-as-a-Service (IaaS) cloud platform combining specialized hardware and software to deliver GPU-accelerated AI computing. Customers can rent Nvidia GPUs by the hour, ranging from about $2.70 for A100 to $6 for H100/Blackwell, on bare-metal Kubernetes-native clusters designed for low-latency, high-throughput model training and inference.

Its key strengths lie not only in rapid deployment of the latest GPUs and high-performance liquid-cooled, dense hardware clusters, but also in its cloud-native software platform that enables efficient resource scheduling, multi-tenancy, and real-time monitoring, ensuring consistently high utilization and seamless scaling.

The company is also diversifying its offerings beyond core GPU compute by adding VFX workstation and rendering services, as well as flexible “Spot” capacity for on-demand use, showcasing its evolution into a full-stack AI cloud services provider that integrates hardware infrastructure with software-driven resource management.

-ecf09af56e814957af719701bdf2e560.jpg)

Source: CoreWeave

Industry Context

AI infrastructure demands massive and cyclical investments in GPUs and power, with each new chip generation causing shortages that then stabilize as more capacity comes online. Power and cooling are as limiting as chips, often requiring years to set up, making speed and specialist expertise critical. Operators that secure Nvidia supply and large-scale power early, and manage their own performance across power, cooling, and networking, can convert investments efficiently, outperforming generalists. However, reliance on big clients and complex build-outs introduces risk, highlighting the need for solid contracts and careful timing of new capacity.

Contract-First Model: Economics and Timing

CoreWeave’s contract-first model drives rapid infrastructure growth while managing risk. Clients sign 2–5 year take-or-pay contracts before new GPUs and data centers are ordered, turning future guaranteed revenue into collateral for debt financing. CoreWeave then spends heavily up front on hardware, cooling, and power, expensing these investments over 5–6 years. This creates a timing gap: most cash and interest costs arrive immediately, but revenue is recognized only as new clusters go live and are used. Early contract cohorts may show operating profits, but company-wide cash flow and net income remain negative until revenue ramps enough to cover debt and depreciation.

After initial terms, GPUs can be re-leased to extend returns. If new activations, including next-gen GB200/GB300 hardware, proceed on schedule and utilization is strong in late 2025 and 2026, much of this year's CapEx will start earning promptly, narrowing the timing gap and significantly improving profitability under the same contract-anchored, depreciate-over-time structure.

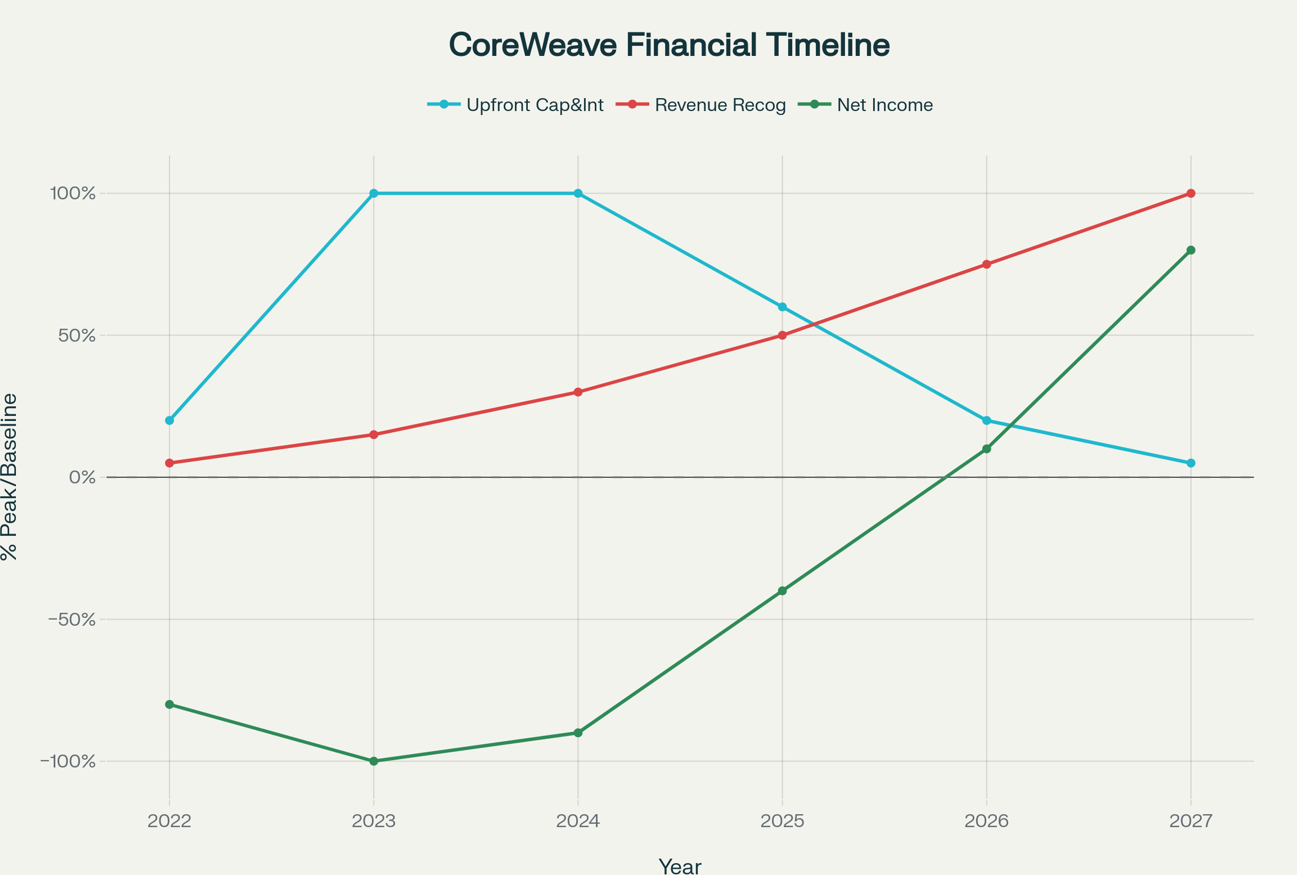

The graph below shows a possible timeline for CoreWeave’s finances from 2022 to 2027. Upfront capital and interest peak in 2023–2024 during heavy buildout, then decline. Revenue ramps from 2023 through 2027 as capacity comes online. Net income is expected negative early on due to timing gaps but may turn positive around 2026 if utilization and execution go well.

Source: CoreWeave, TradingKey

Competitive Advantages: GPU Scale, Speed, and Operational Excellence

CoreWeave quickly brings Nvidia’s latest GPUs (H100, H200, Blackwell/GB200) online—often in months, not the year-plus typical at major clouds—giving customers fast access when supply is tight. Its bare-metal, liquid‑cooled clusters reduce throttling and maximize uptime, while smarter scheduling delivers GPU utilization above industry norms, lowering training costs. CoreWeave’s pre‑aligned land, power, and networks mean new capacity activates fast, cementing CoreWeave’s edge in speed and performance for demanding AI workloads.

Infrastructure and Power: Critical Enablers of Scale

Power is the main bottleneck for scaling AI infrastructure. By mid-2025, CoreWeave ran 33 data centers with 470 MW active, and 2.2 GW contracted, planning to exceed 900 MW active as sites energize. Major projects, including the $6B Lancaster data center (up to 300 MW) and the pending Core Scientific acquisition (adding about 1.3 GW of capacity), will further expand reach and control. Securing utility interconnects, grid upgrades, and liquid cooling takes 18–36 months; CoreWeave’s approach coordinates land, power, cooling, and networks to speed up deployments and maximize density.Unlike hyperscalers (AWS, Azure, Google), which spread multi-gigawatt footprints across a mix of workloads and prioritize custom chips, CoreWeave focuses on rapid deployment of Nvidia clusters for AI, providing scale and timing advantages. Compared to regional neocloud rivals, its multi-gigawatt pipeline and frequent first-wave GPU rollouts offer more capacity and faster upgrades, while smaller competitors operate at much lower power and slower pace.

)

*Note: Hyperscalers’ numbers include diverse workloads, less specifically AI GPU-dense.

Financial Landscape & Outlook

CoreWeave is executing a capacity‑led ramp: guidance is rising, backlog is large but concentrated, capex is heavily back‑weighted to Q4 for site energizations, and leverage is high but manageable if power activations and GB200/GB300 placements stay on schedule.

)

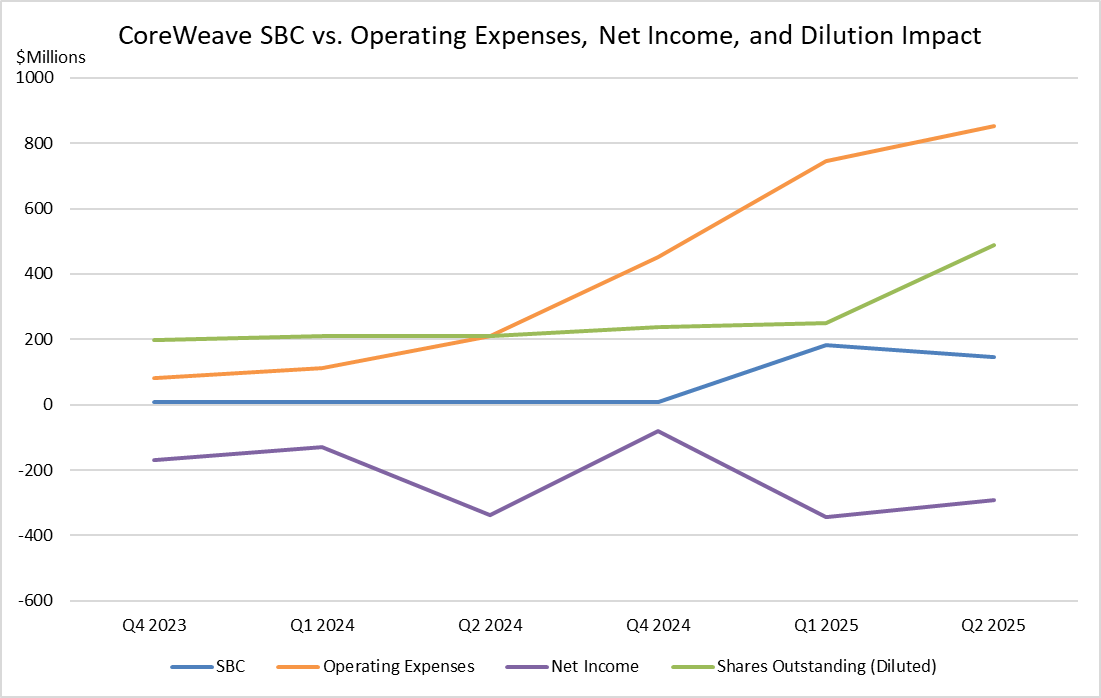

CoreWeave’s stock-based compensation (SBC) expenses have surged sharply, reaching $146M-$184M per quarter in early 2025 from under $10M in 2023, significantly inflating operating costs and compressing profit margins despite strong revenue growth. This elevated SBC level materially dilutes shareholder value through increased share issuance, while also exerting ongoing pressure on reported earnings quality. Combined with large CapEx and debt, SBC forms a substantial part of CoreWeave’s cost structure during its rapid expansion, making it a key factor in the company’s path toward sustainable profitability and cash flow generation.

Source: CoreWeave, TradingKey

Valuation

Assume 2025 revenue at the midpoint of guidance, $5.25B, and apply a 50% TTM EBITDA margin proxy to estimate forward EBITDA of about $2.63B. Given sector comps for AI-exposed digital infrastructure typically trade in the high-teens to low-20s EV/EBITDA and CoreWeave’s mix of strong contracted visibility but elevated leverage and concentration, a blended 18–24x multiple is appropriate. Applying an 18x–24x EV/EBITDA range yields an enterprise value of roughly $47.3B–$63.1B. Using net cash (debt) of TTM −$13.41B and 296M diluted shares, implied equity value per share is approximately $115 at 18x and $168 at 24x.

Risks to Consider

- Client concentration: Revenue is highly dependent on a few large customers, making results sensitive to their budget or strategy changes.

- Leverage and liquidity: High debt and interest costs constrain flexibility and raise refinancing risk if cash generation slips.

- GPU and power supply: Dependence on Nvidia allocations and timely power energization creates exposure to supply, allocation, and interconnect delays.

- Duration mismatch: Long facility commitments can outlast shorter customer contracts, increasing re tenancy and renewal risk.

- Technology and competition: Faster GPU refresh cycles and custom accelerators at larger clouds can pressure pricing and shorten monetization of older fleets.

Conclusion: High Potential with Manageable Risks

CoreWeave is a high-upside, execution-sensitive vehicle for sustained AI compute growth: the bull case relies on multi-year contracted demand, prioritized Nvidia access, and steady capacity activations translating into high utilization, while the bear case centers on delays, leverage, and customer concentration. For those constructive on continued AI workload expansion, the setup is attractive as operating leverage can improve with on-schedule deployments; if AI demand softens or activations slip, interest burden and concentration risk can keep results volatile.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.