Investing in Clean Energy

- Clean energy investment has surged to record levels globally, exceeding $2.2 trillion in 2025 and driven by policy and energy security needs.

- Renewable capacity expanded rapidly, with 582 GW added in 2024, highlighting the acceleration of solar and wind adoption, notably dominated by China and Asia.

- Slowing growth in U.S. solar and wind is countered by explosive battery storage gains, marking a shift in where investment momentum lies.

- Policy catalysts like the U.S. IRA and Europe’s Clean Industrial Deal are unlocking massive capital and reinforcing the sector’s maturity and economic significance.

TradingKey - Clean energy has progressed from a specialist policy talking point to one of the world's most influential forces acting upon global capital markets. In 2025, clean technology investment, from renewable generation and storage to electrified transport, surpassed an unprecedented barrier, exceeding money spent on fossil fuels for the first time in history. This was not driven by an isolated event, but was the culmination of several years' worth of breakthrough technologies, decreasing prices, favourable government policies, and changing corporate agendas. For investors, no longer is the debate about whether clean energy is expanding, but how to capture the value of an industry that is rapidly redefining the world's energy economy.

Source: https://www.rinnovabili.net

Scale and Momentum of Transition

The statistics present overwhelming evidence. In recent years, year-on-year renewable capacity additions have reached record highs. Solar has been leading from the front, adding hundreds of gigawatts annually. Onshore wind keeps its trajectory, even if on a relatively more subdued note, and storage batteries are proving to be the category with the highest growth, which fuels the stability and flexibility of renewable-dominated networks. Even if certain markets experience slower year-on-year percentage growth, their intrinsic foundation has grown exponentially so that raw absolute additions remain stunning.

This surge is not limited to advanced economies. Asia, driven by China, now leads clean energy growth globally, opening huge new solar, wind, and hydropower projects annually. Emerging markets like India, Vietnam, and Brazil are ramping up their own build-outs, spurred by domestic demand and hopes of luring foreign investment into manufacturing and infrastructure.

.jpg)

Source: https://www.statista.com

Technology, Costs, and Competitiveness

Clean energy's investment thesis is built upon the dramatic declines of the last ten years. Photovoltaic module prices have declined by over 80% since 2010, and onshore wind prices have declined by over a third. In most markets, renewables are now the lowest-cost source of new power generation, even before considering subsidies or tax credits.

This cost competitiveness has fundamentally changed the way utilities, corporations, and governments plan for the future. Where renewable adoption was once driven by environmental mandates, it is now increasingly an economic decision. Combined with the flexibility offered by advanced energy storage and smart grids, clean power is moving from an “alternative” to a “default” choice in new capacity planning.

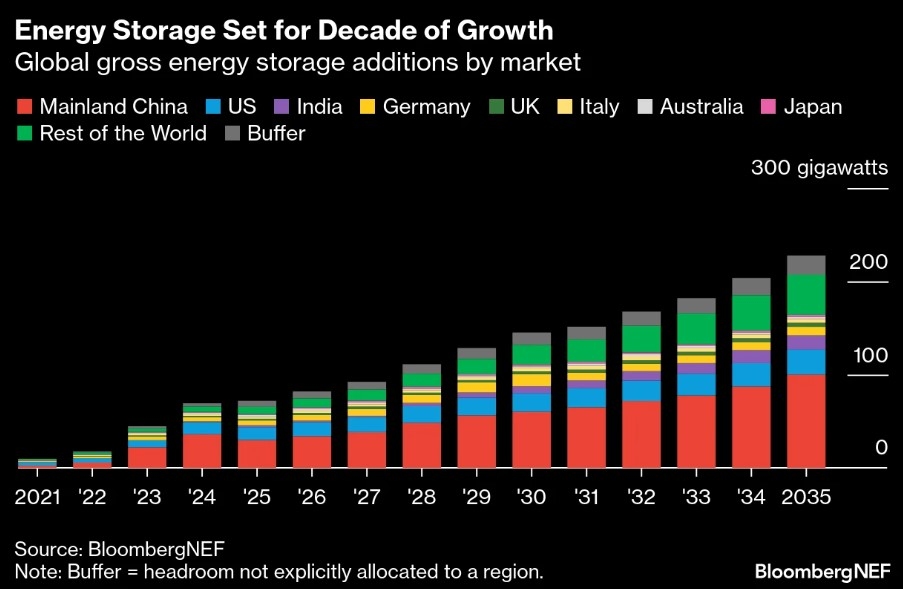

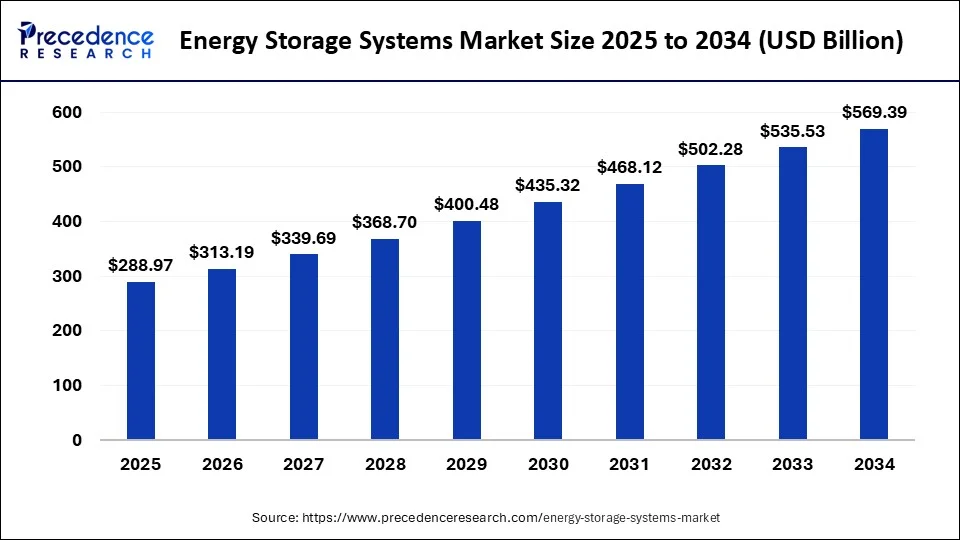

Battery storage, in particular, is unlocking the promise of levelling renewable generation variability, which would make wind and solar mainstream, as opposed to supplementary forms of power. Sudden leaps in battery density, efficiency, and duration are attracting utility-scale applications, as well as distributed, behind-the-meter applications for companies and households.

Source: https://www.precedenceresearch.com

Policy As A Growth Multiplier

Government incentives remain one of the key motivators of the industry’s pace and trajectory. In America, the Inflation Reduction Act has triggered hundreds of billions of dollars of investment commitments, reviving US domestic manufacturing centers, renewable farms, and EV corridors from coast to coast. In Europe, all-of-economy policy efforts like Europe’s Clean Industrial Deal are aligning decarbonization objectives with industrial competitiveness, with a twin goal of enhancing the continent’s energy security and clean value chains.

Meanwhile, China has again held its position as the world's leading clean-energy investor, setting aggressive long-term non-fossil fuel energy targets, and once again leading solar manufacturing production. Such policy-driven tailwinds not only offer short-term project pipelines, but multi-year predictability supporting company planning horizons and investor portfolio allocations.

Structure Problems and Market Imperfections

Despite its path, though, the clean-energy sector has to tread delicate paths. In a number of locations, accelerated capacity additions have outstripped power-grid upgrading, leading to inefficiencies such as curtailment or even negative electricity prices when supplies exceed demand. Imbalances of this sort, unless balancing power transmission infrastructure and storage investment accompanies new projects, can upset subsequent projects' economics.

Supply chain volatility continues to be an issue as well. Geopolitical tensions have sparked increased concern over key materials like lithium, cobalt, and rare earth, which are needed for solar panels, wind turbines, and batteries. Export curbs or supply bottlenecks can spread throughout an entire value chain, causing cost and schedule impacts on projects.

In addition, the industry's dependence on favorable policy implies that changes in political attention, driven by elections, budget concerns, or trade controversies, can quickly change the investment environment. In this way, short-term policy uncertainty can cause volatility for publicly traded clean energy equities, even if the long-term trend to decarbonize is not likely to be overturned.

Investment Strategy and Opportunities

Despite its complexity, the clean energy industry has several points of entry for investors of different risk tolerances. At one extreme of the spectrum are the big, diversified industrial and energy majors that diversify their overall portfolios with add-ons of renewables. The companies provide exposure to growth within the industry but cushion investors with revenue streams from unrelated lines of business.

On one extreme are pure renewable developers, equipment companies, and storage battery players. These have more upside in a healthy market but are more vulnerable to policy shifts, input cost moves, and debt markets. Those funds that buy clean energy through exchange-traded funds (ETFs) do not get to diversify across geography and technology without choosing individual winners.

Income-seeking investors who desire stable cash inflows from long-term utility/government contracts favor infrastructure funds and green bonds. For exposure to earlier-stage risk, the venture category offers exposure to nascent technologies such as green hydrogen, carbon capture, and next-generation storage solutions.

A Role for Energy Storage in Unleashing Value

If clean power is the power plant of the transition, storage is its gearbox that gets it operational. Battery deployment is growing rapidly, both for utility-scale deployments and for distributed deployments for communities, businesses, and electric vehicles. Storage doesn't only balance supply and consumption but also enables transport electrification as well as microgrid development in remote, underserved communities.

With further falling battery prices and scaling performance, storage will be an even greater investment driver of clean energy's appeal. This forms a secondary investment universe within battery production, recycling, software optimization, and associated supply chains.

Long-Term Perspective

Clean power in the coming decade will continue its climb towards world electricity's number-one source. Renewable generation economics, as well as automobile and building electrification, will slowly erode further fossil fuels' share of the mix. Despite occasional spotty policy interruptions or macroeconomic declines, their long-term trajectory is toward further integration, decreasing prices, and higher profit margins.

What investors would like to do is put time horizon and risk tolerance together with a suitable asset mix. For stable growth, investors can balance portfolios with mature utilities and broad-line industrials, aggressive investors can introduce exposure to high-growth manufacturers, warehousing, and early-stage innovators.

Renewable energy investing today is the early internet, early cloud computing, an early transformative technology on the brink of mass adoption. No longer about being an ethics play, it's now about being a structural growth story that combines environmental sustainability with economic promise. As demand for clean, affordable, low-carbon power continues to surge globally, the clean-energy industry's 21st-century role will be an ever-expanding one. Patient capital will be amply rewarded, and timing couldn't be much better than it is today, when we are in this era of mass transition and building out of infrastructure.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.