Investing in Industrials Stocks

- Industrials are quietly outperforming the S&P 500 in 2025, driven by reshoring, infrastructure upgrades, and AI-enabled modernization.

- Strategic tailwinds like defense, grid electrification, and automation are turning legacy companies into long-term compounders.

- Opportunities span from aerospace to energy infrastructure, with rising cash flows, margin expansion, and M&A unlocking value.

- Risks include overconfidence near peak cycles, high rates, and international slowdowns—making selective exposure critical.

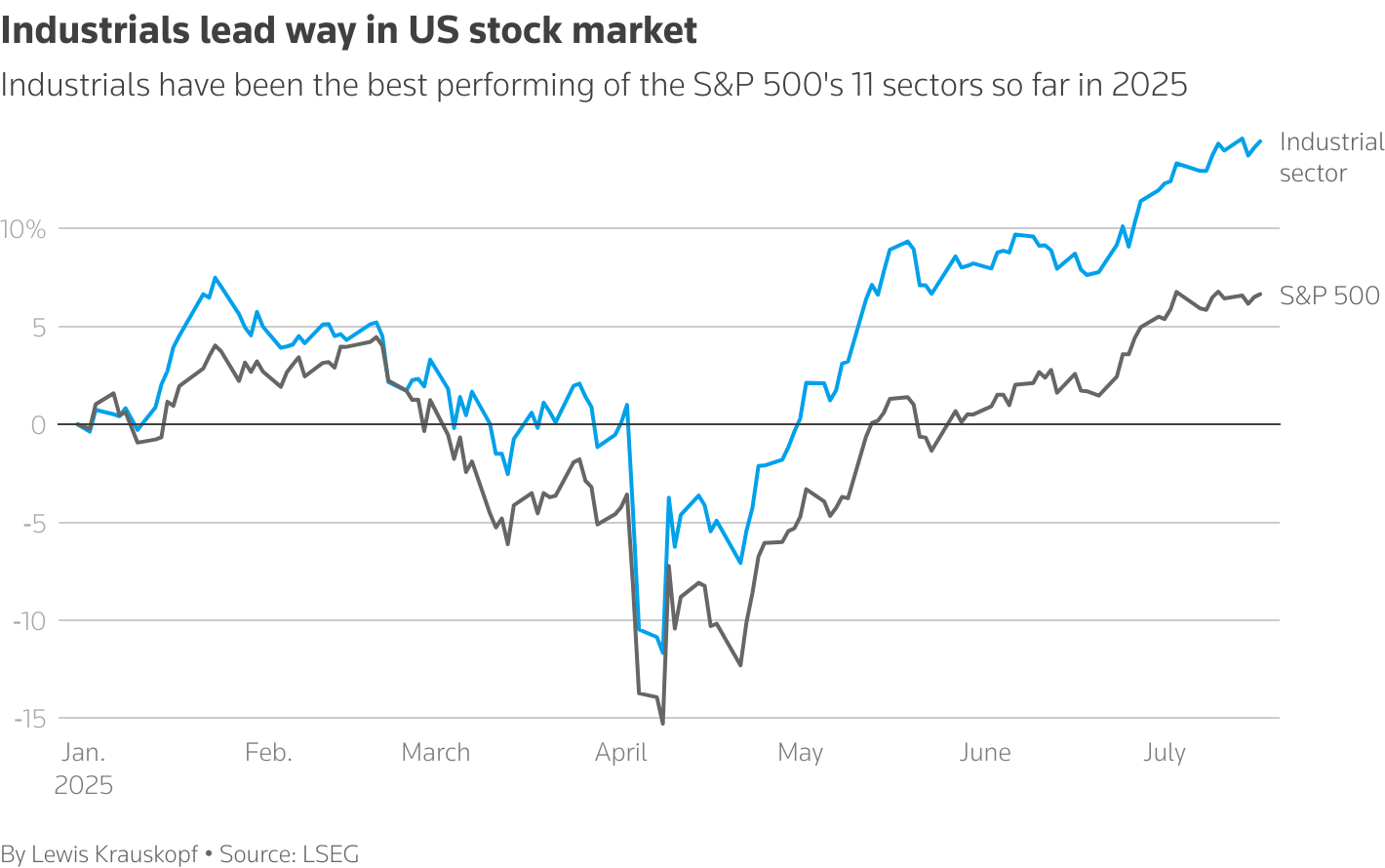

TradingKey - Industrials are having a remarkable 2025 recovery, quietly but powerfully. No longer a defensively minded, yield-driven sector, they are riding waves of structural change from geopolitics and AI infrastructure to the great global supply chain reshore. While the S&P 500 continues to climb, its own industrials sector left it in its dust as a testament to a surging investor optimism, corporate pageantry, and policy tailwinds that are breathing new life into everything from aerospace to construction equipment.

The shift isn't being driven by speculative mania but by something more substantive: fundamentals. From grid electrification to physical infrastructure reconstruction both in the Americas and abroad, demand for industrial capability is accumulating. New tech, especially that related to automation, energy transition, and supply chain transformation, is transforming old-economy corporations into next-generation entities. Such alignment of forces is turning industrials into one of the most strategic spaces for long-term deployment of capital.

Source: https://www.reuters.com

The Engines of Momentum

One of the key reasons why industrials are moving into favor is because they sit at the intersection of multiple macro trends. As nations prioritize economic security as well as home resilience, manufactured reshoring as well as physical infrastructure expenditure are fueling demand within transport, logistics, engineering, as well as power systems. That isn't a short-term cycle. It's a generation-long shift that rewards business with scalability, quite often with a few decades of history as well as balance-sheet strength.

Additionally, industrial M&A activity is picking up. Executives are selling non-core business units and concentrating on high-margin or high-tech verticals. From aerospace to automation to precision engineering, the industrial universe is retooling for success in a world defined by digital controls, AI optimization, and geopolitical fragmentation. Long-term investors are seeing selective entry points in stocks once too mature for growth.

Another underappreciated catalyst is that of industrial activity conjoining with AI and cloud technology. Power plants, electricity grids, smart factories, and defence systems increasingly require real-time data processing and edge computing, spaces once controlled primarily by technology giants. Industrial companies are integrating smart systems into their products in ever-larger quantities, giving birth to new levels of repeat revenue as well as new points of efficiency gains.

.jpg)

Source: https://www.pwc.com

Where Opportunity Is Emerging

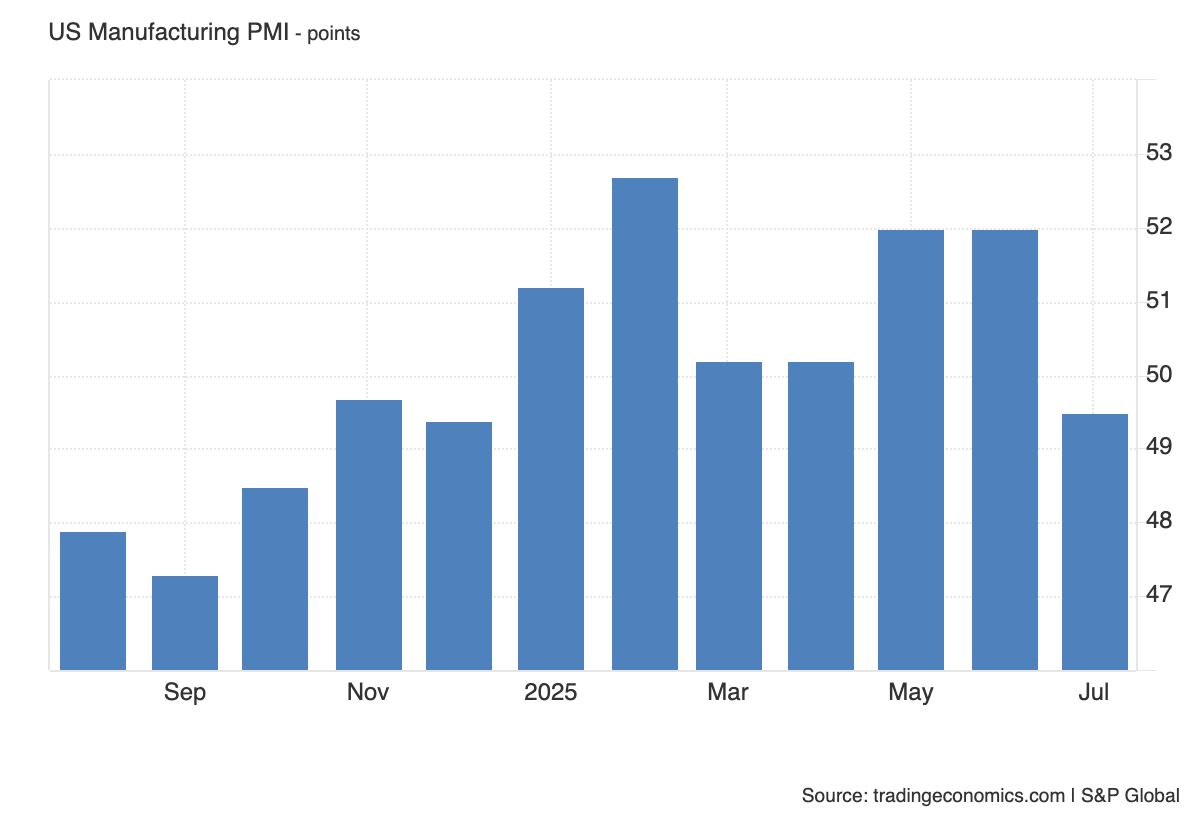

Some of the more obvious beneficiaries of this industrial revival are advanced manufacturing, energy infrastructure, aerospace, engineering services, etc. Participants in the power equipment segment have been key beneficiaries, with benefits stemming from increasing energy efficiency, electrification, as well as demand for grid modernizations. Not only are they selling into strong backlogs, they are also benefiting from AI's energy profile, which is forcing governments and data centers to redeploy at scale in power systems.

Source: https://tradingeconomics.com

Aerospace too is making a robust recovery, both defence as well as commercial demand gathering steam. Order-driven entities having strong global linkages are primarily beating estimates hands-down, continuously tweaking their estimates of profits upwards. Engineering as well as construction gamers are supported with order backlogs premised on mega-scale infrastructure as well as energy initiatives, creating operating leverage as well as investor interest.

Steel and mining stocks, particularly insulated from tariff risk or with strong domestic exposure, are quietly delivering double-digit returns. Repricing of contractuals as well as optimisation of production makes them surprisingly agile amidst turbulent macro headwinds.

Even traditional industries are going through valuation re-ratings. Names that were once slow-moving are now viewed through the lens of cash flow reliability and optionality, especially if they show capacity for transformation or leaner capital allocation. Since industrial policy is invoked as a tool of national strategy, they are highlighted as secular as opposed to cyclical growth.

Risks Beneath the Surface

No sector moves linearly, however. Industrial economics is cyclic at its very fundamentals. Freight and logistics, for instance, have been a little softer, and heavy equipment-focused enterprises can face margin pressures should input costs increase or order inflations get started. Deteriorating warehouse leasing as well as logistics REITs as well suggest a demand frenzy of pandemic aftershocks in certain verticals could be dying down or mellowing.

Monetary policy is still a wild card. As long as interest rates are high and inflation suggests stickiness, some of the corporations would delay capex cycles, especially those who depend on debt funding or government orders. Slow-downs in Europe or unexpected slow-downs in China would further dampen demand for industrial exports, affecting internationally vulnerable players.

Another big risk is end-cycle overconfidence. While inflows are going into industrials, you want to resist going for returns without distinguishing between structurally robust names and cyclical beta plays. Those who over-expose to the right names at the wrong time get caught offsides when the momentum fades.

Strategic Outlook for Investors

Investing in industrials in 2025 demands sophistication. It is not a broad-based rally where everything moves equally. There are winners who merge deep sector expertise with operating versatility, technology resurgence, as well as exposure to themes that have endured for a long time - energy transition, defence modernisation, as well as AI infrastructure.

Successful investors will be able to differentiate between structurally compoundable names, those with moats, cash generation, and pricing power, and short-cycle names that move with the tide of economics. Exposure to the sector can provide a useful hedge against tech or consumer discretionary overexposure, and selectively done, can unlock enduring cash flow streams.

The genius plays are in those companies walking the tightrope between old and new. Those are the corporations reengineering their operations, digitalizing their processes, and infusing intelligence into their equipment and logistics. Industrial isn’t about smoke stacks anymore, it’s about intelligent factories, clean grids, autonomous systems, and multipolar-world-ready supply chains.

Conclusion

Industrials are often overlooked during bull markets and overbought during downturns. But in 2025, they are neither boring nor outdated. They’re redefined, leaner, smarter, and central to how the global economy is being rewired. For investors seeking exposure to real-world growth, tangible productivity, and secular transformation, industrials may well be the foundation layer of the next decade’s portfolio. The opportunity lies not in chasing momentum, but in owning the capacity that powers progress.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.