Howard Marks Portfolio

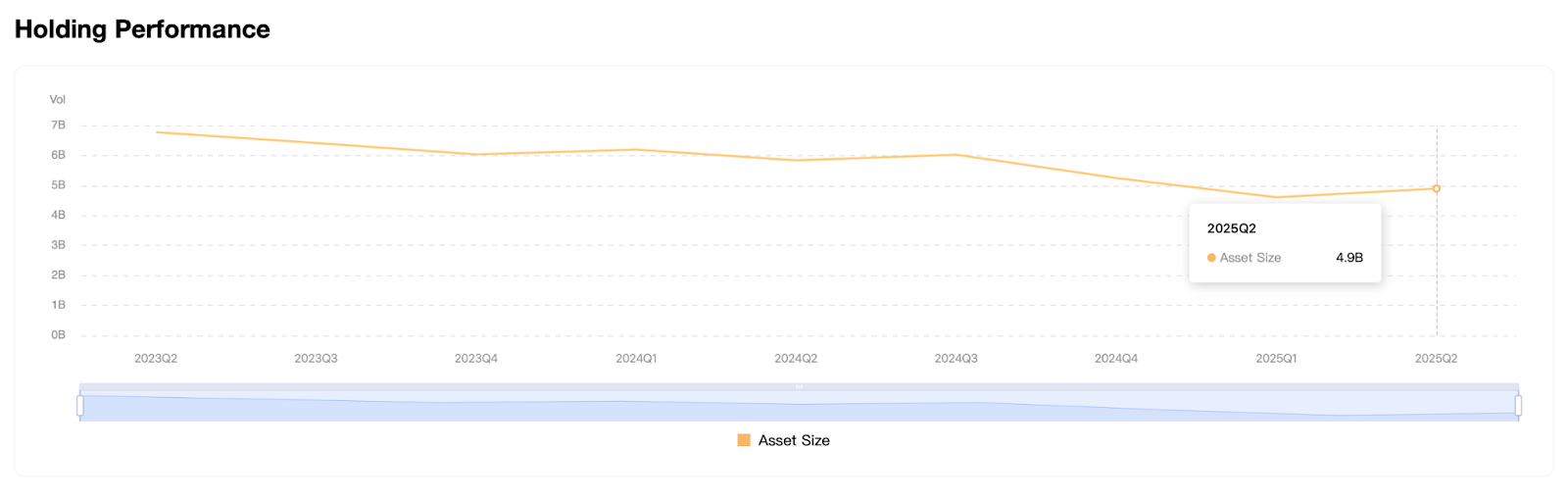

TradingKey - Howard Marks has been praised for a decade for his uncanny ability to distill complex market environments down to the simple, risk-aware judgments. Through his position as co-founder and Chairman at Oaktree Capital Management, he has gained fame not with showy profits or public trades, but with a consistent and disciplined focus on the management of risk and value-focused investing. The same philosophy remains the foundation for Oaktree's equity portfolio at the close of the second quarter 2025, which closed the period with $4.9 billion under management.

Oaktree’s approach still is based on contrarianism, buying when others are selling, going into areas avoided by momentum players, and finding spots where dislocation generates long-term asymmetricity. The Q2 report records a modest appreciation in asset value, advancing 6.15% to $4.61 billion compared with the previous quarter. Positions declined, however, from 325 to 309, a reflection of a narrow focus narrowing, fewer names with increased conviction.

Further, buys declined dramatically from 38 to 15, while sales rose to 73, a strong suggestion that Marks and colleagues are trimming exposure in areas where they believe overvaluation exists and redeploying capital into single-name, deeply mispriced situations

Energy Dominance and the Case for Hard Assets

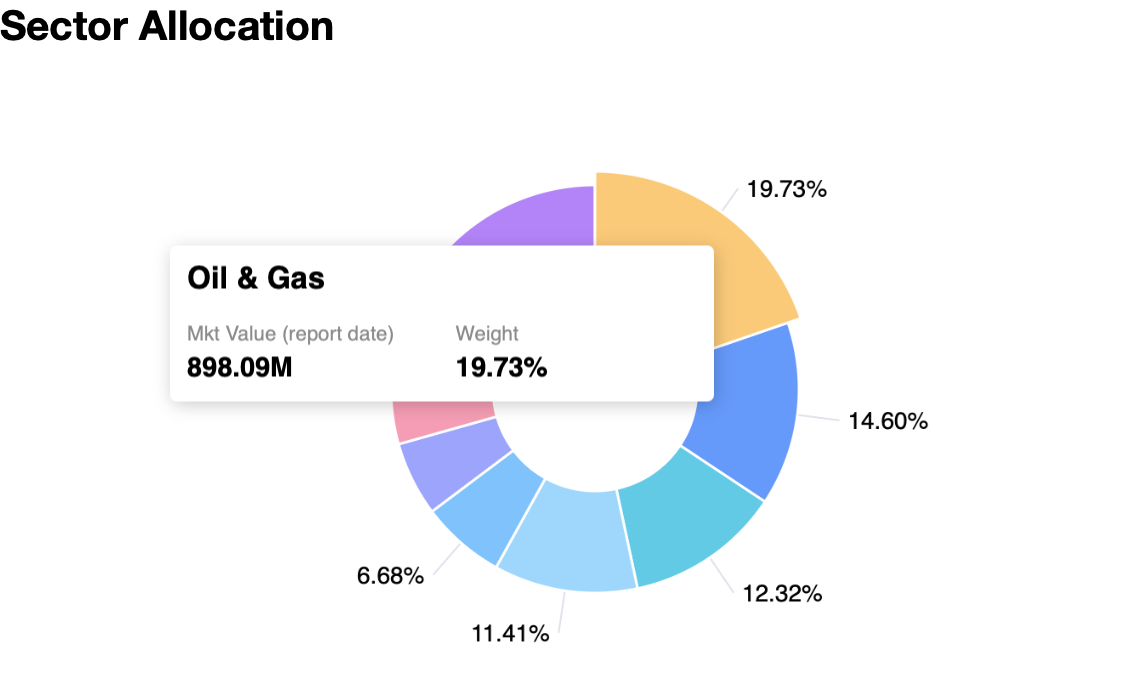

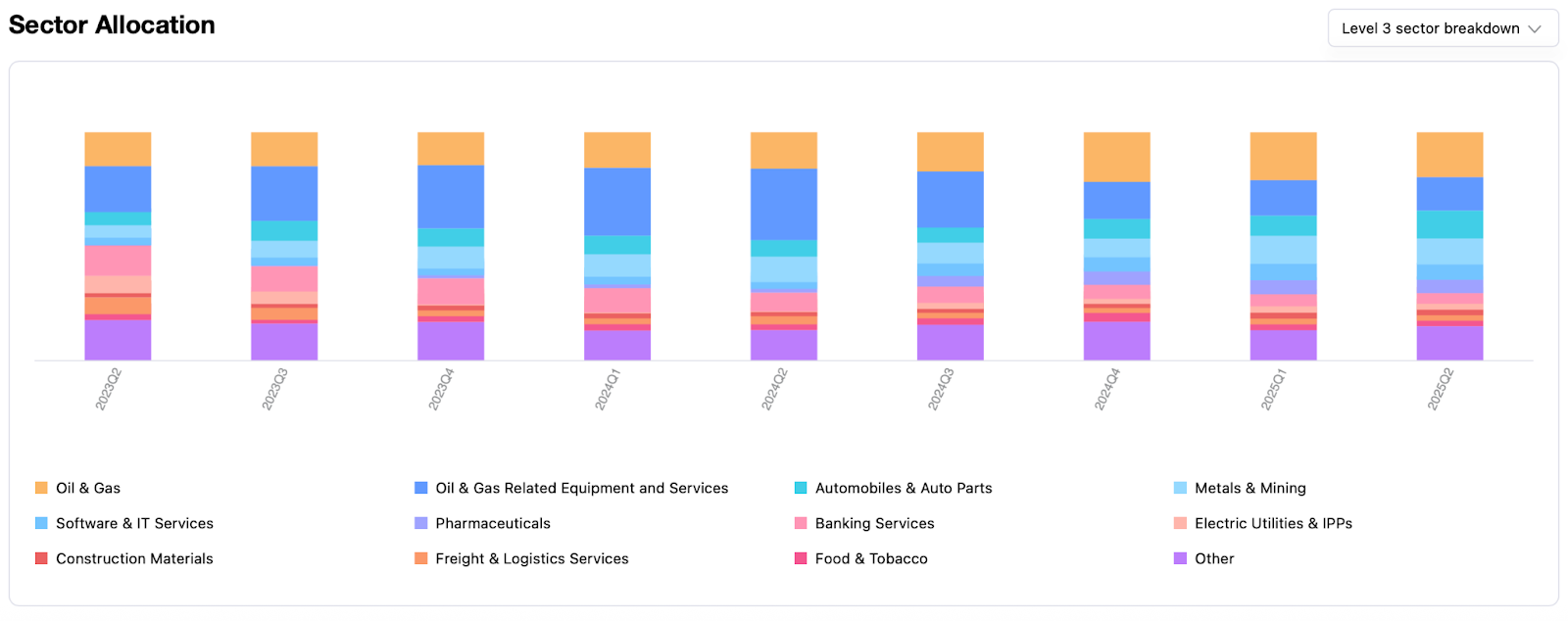

What’s most striking here is how focused the portfolio is in energy. Energy names now comprise essentially 20% of the whole portfolio. With oil & gas-related equipment and service names included, that number goes well beyond 30%. This is not a speculative bets-on-commodities type game. This is a deliberate allocation into an industry in which valuations are at below-historical averages and in which cash flows are actually improving due to capital discipline across the industry.

In addition to upstream names, the portfolio includes service providers, midstream entities, and royalty-based businesses. Including Sitio Royalties and Chesapeake Energy suggests gentle exposure, not just to revenue based on volume, but the type of asset-light business that benefits off the mineral rights or the tolling economics. In an inflationary or rate-sensitive economy, real asset-linked businesses enjoy predictable returns and the inflation hedging that so many of the high-growth tech names lack.

Apart from energy, another significant theme is metals and mining. AngloGold Ashanti’s continued ranking within the top holdings indicates bullishness for equities related to gold, perhaps functioning as protection against geopolitical tensions or ill-timed monetary policy movements. The movement toward hard assets more generally is a reflection of Oaktree’s confidence in physical value, businesses grounded in real-world production, supply-demand dynamics, and lasting cash flows.

A Tight Core of High-Conviction Bets

Whereas managers diversify for the sake of diversification, Oaktree continues to focus around a small number of strong convictions. The biggest position at the latest quarter was TORM, the Danish product tanker company now representing over 13% of the equity portfolio. This big position is a thematic bet on shipping constraints, supply chain normalization, and tanker deficiencies. The shipping sector remains underinvested, and Marks appears to be positioning before the globe experiences a logistics bounce back.

Coming second is Expand Energy, another energy-weighted name with over 12% weight in the portfolio. Garrett Motion, a well-liked industrial name that is in the process of financial and operating restructuring, is at just under 8%. All these positions show the theme: cyclical exposure with underappreciated upside, plus good balance sheets and improving fundamentals. While institutions rush in herds to the megacap growth names, Marks again tips his portfolio back down the less-traveled road.

Other significant holdings such as ENDO and ABC Technologies show that even beyond the natural resource sector, the strategy remains the same, targeting those companies that have market overhangs, underrated earnings capability, or recovery in the post-distress sector. They are not name companies, per se, but the kind that could silently triple in a cycle if rightly re-priced by the market.

Trades That Have a Tale

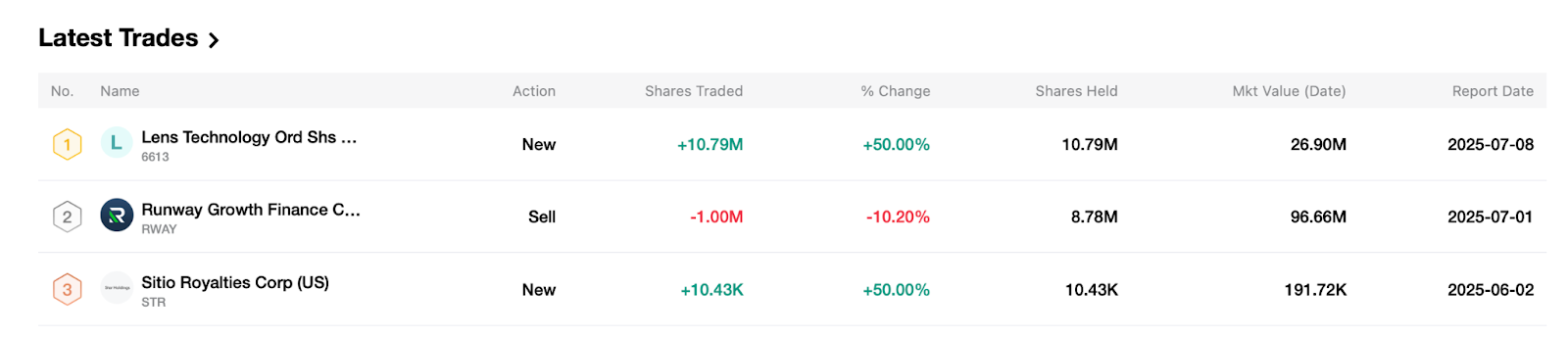

This latest action provides color to the larger picture. While aggregate positions decreased, new entries were taken. Lens Technology, Contemporary Amperex Technology, and Jiangsu Hengrui are just a few of the spotlighted new entries, each entering the portfolio with the full 50% increase in share number from zero. These names span industrials, renewable battery technology, and drugs, obliquely hinting at selective new entry back into Asian and developing market equities, namely in regions where supply chains or population trends bode prospective long-term growth.

At the same time, decreases and exits speak to sharper reductions. Garrett Motion, once a solid holding, was cut by 16%, and Runway Growth Finance was cut by 10%. The outright elimination of Vacasa indicates Marks is not very patient with companies that are not converging on cash flow sustainability. While no sector rotation was newsworthy, the nuance is revealing a bias for capital redeployment back into names with more asymmetric downside protection and shorter-duration upside visibility.

Resilience in Portfolio and Holding Performance

Despite ongoing macro turbulence, Oaktree’s equities recovered modestly in Q2 after a multi-quarter loss. Asset size had declined from over $6.5 billion in early 2024 to below $4.6 billion in Q1 2025. The rebound in Q2 back to $4.9 billion is significantly less for the size and more for the timing: it was done while the world was confronted with hawkish prints for inflation, volatile energy markets, and strength in the credit markets. Oaktree’s positions, particularly ships, energy, and resource equities, have been more resistant than average to the influences of the macro turbulence.

This is no accident. Marks has repeatedly emphasized that success in investing is not avoiding volatility come what may, but controlling it. His risk-first approach is not market timing, but constructing portfolios resilient enough to survive drawdowns and profit from panic-induced mispricings. That underlining philosophy still finds expression in the manner Oaktree has switched back into more defensive stocks and hard asset proxies in this context.

Why Thinking Differently Is Enduring

Howard Marks' method is unlike the majority of the modern-day asset management industry. While others chase beta, size with passive offerings, or race into high-multiple growth at the hint of momentum, Marks raises bets against inefficiencies. Still happy with unfashionable positions if the value disconnect justifies it, he is okay with volatility as friend, not enemy, and loves repeating “you can’t take advantage of irrational behavior unless you’re willing to act differently.” This Q2 2025 equity portfolio is an expression of that philosophy at work. It’s based upon patience, judgment, and strong faith that value eventually is going to come through, almost always in the very corners most investors steer clear of.

While the headlines are touting AI and cloud infrastructure, Marks is quietly building a stake in energy infrastructure, cyclical recovery, and industrials in emerging markets. For investors seeking insights into how experienced professionals manage through changing market regimes, Oaktree’s equity orientation is a playbook worth reviewing. It illustrates the reality that capital needn’t hurry off the sidelines, it must move judiciously. And with the help of a good framework for considering risk, the best trades frequently reside less in pursuing the tried and true and more in leaning into the untested, though still good ideas.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.