Van Duyn Dodge and E. Morris Cox Portfolio

.png)

TradingKey - In the early 1930s, amidst the ruins left by the Great Depression, Van Duyn Dodge and E. Morris Cox tried to build something different, an investment firm led not by trends or commission, but by discipline, humility, and exhaustive research. Born out of that ideal was Dodge & Cox, the name that would come to be associated with steady-handed value investing and one of the few heritage firms that was able to uphold the original ethos for nearly a century.

In contrast to the great majority of its contemporaries, Dodge & Cox has been purposefully lean. With over 500 employees and hundreds of billions under care, it resists the heavyweight organizational modalities typical of companies the size of itself. Its investment approach, highly team-centric, long-term-focused, contrarian, has not simply survived but thrived over market cycles.

Rather than relying upon a star manager or top-down directive, the firm acts as a series of closely configured committees with a focus upon group judgment and bottom-up research. This group decision-making process has produced very low portfolio churn and superior capital preservation over the decades.

Gradual Progression, Considered Changes

That philosophy is still very much evident today. In the second quarter 2025, the firm had $233.4 billion in assets under management, a 2.84% increase for the period, spread across 569 positions. Down one position, from 576, this is modest tightening, not across-the-board reallocation. In the same period, the buys increased significantly, from 133 to 219, and sales increased from 165 to 186, a sign of a controlled shift toward rearranging positions, not expanding portfolios. It’s the kind of data that indicates a thoughtful development of conviction, rather than a reactive chasing trends.

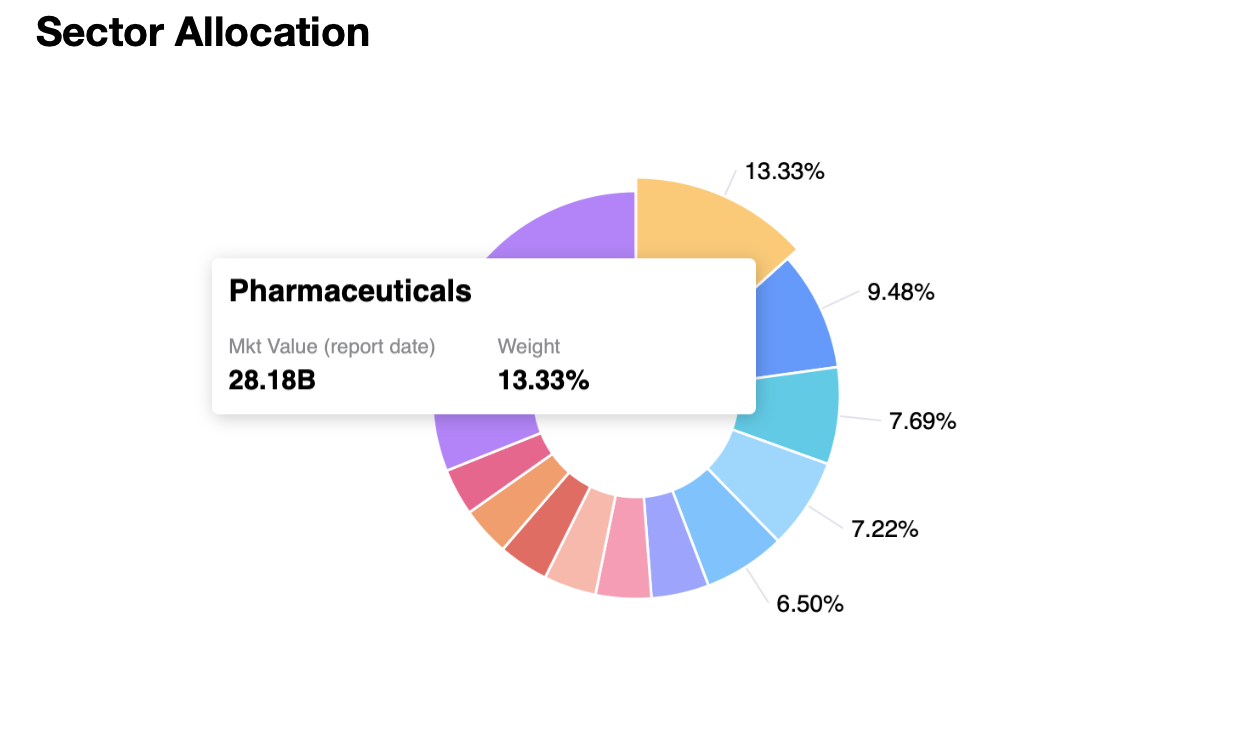

Sector allocation again reveals this balancing between persistence and tacit rotation. Pharmaceuticals lead with 13.3% allocation, followed by bank services with 9.5%, investment banking and other services with 7.7%, and software and other information technology-related services closely following with 7.2%. On its own, the allocations related to healthcare, including providers and healthcare-related services, hint that Dodge & Cox is convinced the sector possesses structural defensiveness and ultimate demand, a prudent call under today’s uncertain macro atmosphere.

Another interesting feature is the persistent diversification across sectors. Though healthcare and financials form the foundation, coverage for the sectors such as aerospace and defense, insurance, industrial machinery, and energy keeps the portfolio agile and resilient.

Based on Blue-Chip Security

Reviewing the firm’s largest holdings, a pattern emerges: mature cash-generating businesses in industries offering defensive characteristics with economic leverage. Its largest holding is in Charles Schwab, accounting for just under 3% of the portfolio and carrying $8.1 billion market value. Next are Fiserv and Johnson Controls, signaling a strong lean toward financial infrastructure and industrial stalwarts.

Other largest holders include RTX Corporation, CVS Health, MetLife, and Charter Communications, each an industry titan with a long history of business and durable free cash flow. Ownership positions in Sanofi and Occidental Petroleum show Dodge & Cox’s openness to cyclical industries, as long as valuation and balance sheet quality render the risk worthwhile.

These top names lean not towards fashionable tech disruptors, but towards good compounders. Their representation in the portfolio underlies Dodge & Cox’s preference for companies with economic moats, good management, and compelling long-term risk-reward profiles.

Latest Transactions and Strategic Positioning Changes

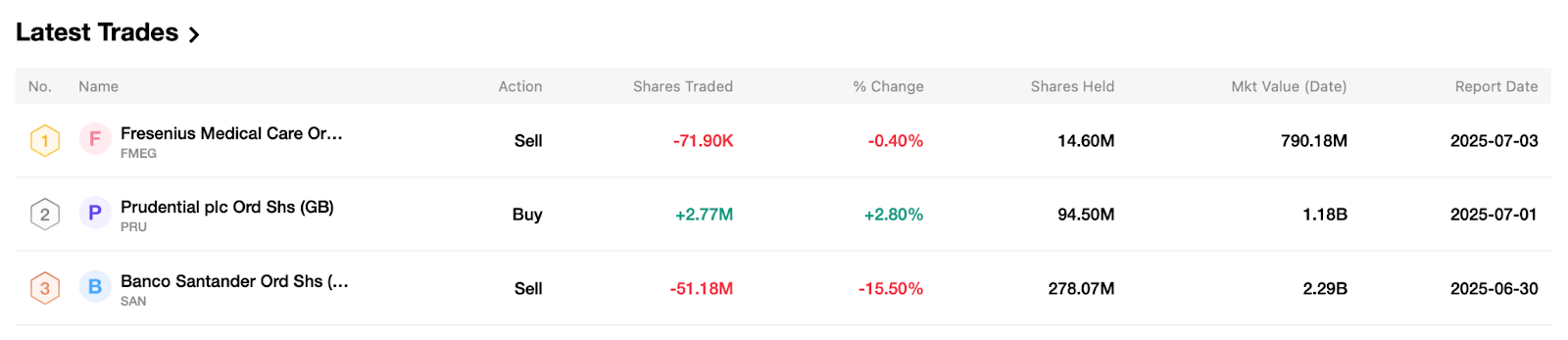

Recent transactions give additional clarity into the firm’s evolving disposition. On the buy side, Taiwan Semiconductor, Glencore, and AIA Group were all significantly added with double-digit increases in the share count. These transactions suggest an international exposure-focused interest, perhaps at the expense of regionally focused tailwinds or valuation resets. On the other side, the firm significantly reduced or closed positions like Banco Santander, Mitsubishi Chemical, and Honda Motor, presumably indicating decreased enthusiasm for companies facing margin pressures or macro uncertainty.

At the holding level, there are some interesting changes. A firm purchase of Baxter International in the previous quarter represents new confidence in the medical sector, specifically for companies at favorable valuation troughs. A massive selling off of Fidelity National Information Services, on the other hand, indicates an overvaluation call or migration back toward more confident ideas. Dodge & Cox sold all positions in Occidental Petroleum, too, a large retreat from the energy space, a potential signal for more caution around the cyclicality or volatility in the commodity space.

Navigating Market Headwinds with Core Principles

Despite its traditionalist roots, Dodge & Cox has been anything but inactive amidst the structural market shifts. The company has steadily incorporated more international and tech-heavy names, though still through its own litmus filter of valuation restraint. Though its history of underweight holding in growth-focused tech names might have resulted in relatively underperforming during occasional bull phases, the firm has remained committed to its values: focus on normalized earnings, sticky cash flows, and conservative assumptions.

Performance-wise, the portfolio’s slow climb in assets over recent quarters suggests this discipline still rewards the patient investor. While those other funds that chase quarterly trends never themselves played short games, Dodge & Cox never did. Even as other markets yo-yo back and forth with shifts in geopolitics, rate indecision, or AI-driven speculation, the firm’s portfolio is based on fundamental value. Its capital-compounding mastery over multi-year time horizons, incurred at reasonably low fees, makes it an ideal template for active management at a time when the industry becomes more and more dominated by passive flows.

Stability Through Structure and Stewardship

Most notable is the persistence of the firm’s stewardship. With committee members holding seats for lengthy time spans and institutional knowledge embedded, the portfolio’s DNA has not been diluted by turnover over the generations. Managers at the firm often invest personal capital in the same portfolios they run, with the result of making incentives aligned with clients and instilling a culture of responsibility.

This structure keeps Dodge & Cox immune to the personality-related fluctuations that plague other fund managers. It also ensures that the decision-making is ever guided by long-term value, not by headlines, quarterly earnings pressure, or fiat of an individual voice within the room.

Next Cycle: Prepared for the Next Cycle

Down the road, Dodge & Cox is well equipped for an industry that might increasingly come back to valuation-sensitive strategies. In the worst-case scenario, if interest rates remain higher or the price of goods and services is sticky, the overweight position in financials and healthcare would serve the firm well. If the pendulum shifts back away from growth euphoria and back to the basics, the underweight position in speculative tech turns weakness into strength. In either scenario, the firm’s sole focus on capital preservation and intrinsic value creates an enduring advantage.

Even when short-term cycles are temporarily biased in favor of high-beta momentum names, the embedded value in Dodge & Cox’s portfolio affords significant protection, and patient appreciation. Their careful, disciplined approach is geared not toward chasing hot trends, but toward riding through what’s inevitable: mean reversion,macro surprises, and sentiment shifts by investors.

Concluding Remarks

In an era where stories of investment are so often controlled by algorithms, influencers, or crowd sentiment, Dodge & Cox is reassuringly unassuming. Its portfolio is not here to excite, it’s here to endure. And for long-suffering investors who still retain any confidence in the gentle power of compounding and the buy-low proposition of buying fifty cents for the dollar, few names within the industry tip the scales the same or possess the same history. At its core, Van Duyn Dodge & E. Morris Cox is a testament to the argument that good investing is not flashy. It’s considerate. It’s enduring. And it’s incredibly personal.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.