Home Depot: Seizing Growth Opportunities in the Home Improvement Market

Investment Thesis

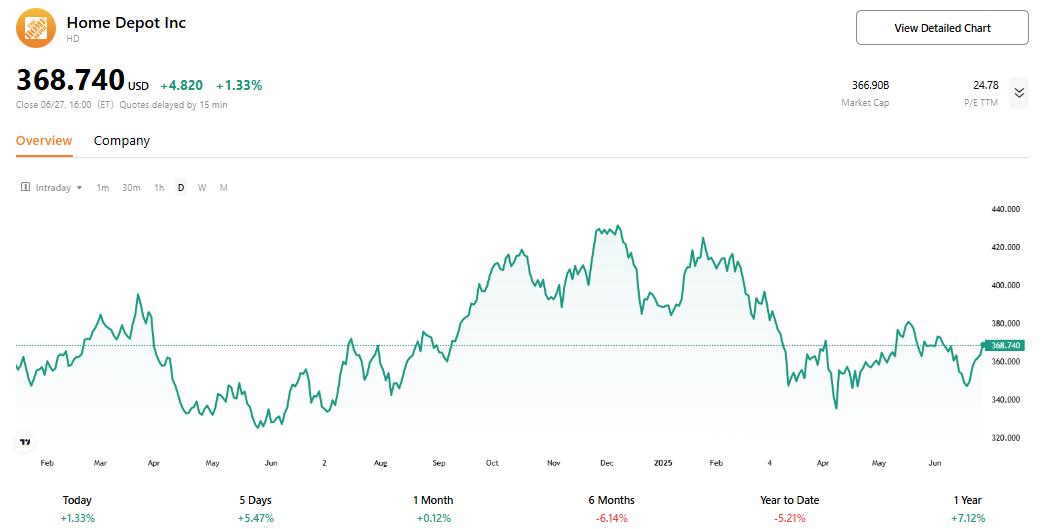

TradingKey - Home Depot (HD.NB) solidifies its leadership in the global home improvement retail market with over 2,300 stores in North America and a strategic focus on professional customers. Despite short-term demand suppression for building materials due to high interest rates and inflation, its diversified supply chain, robust e-commerce growth, and AI technology adoption effectively mitigate risks and drive profitability. Strategic acquisitions in 2024 and 2025 (SRS Distribution and GMS) further strengthen its competitiveness in the professional market. With over 90% of revenue from the U.S. market, combined with easing inflation and declining interest rates, Home Depot is poised for future growth. DCF valuation suggests a target stock price of $403.09 to $415.39, reflecting strong financials and sustained growth prospects, making it a top investment choice in the home improvement sector.

Source: TradingKey

Source: The Home Depot, TradingKey

Company Overview

The Home Depot, Inc., founded in 1978 and headquartered in Atlanta, Georgia, is the world's leading home improvement retailer, operating in the United States, Canada, and Mexico. With its innovative big-box store model, the company has over 2,300 stores and approximately 475,000 employees, making it the largest home improvement retailer in the U.S. market. Its products and services include building materials, tools, appliances, installation services, and equipment rentals, catering to DIY (Do-It-Yourself) enthusiasts, professional contractors, and DIFM (Do-It-For-Me) customers. Additionally, through its robust e-commerce platform and mobile app, the company is actively pursuing digital transformation, adopting an omnichannel strategy to meet consumer needs and maintain a leading position in the highly competitive market.

Competitor Analysis

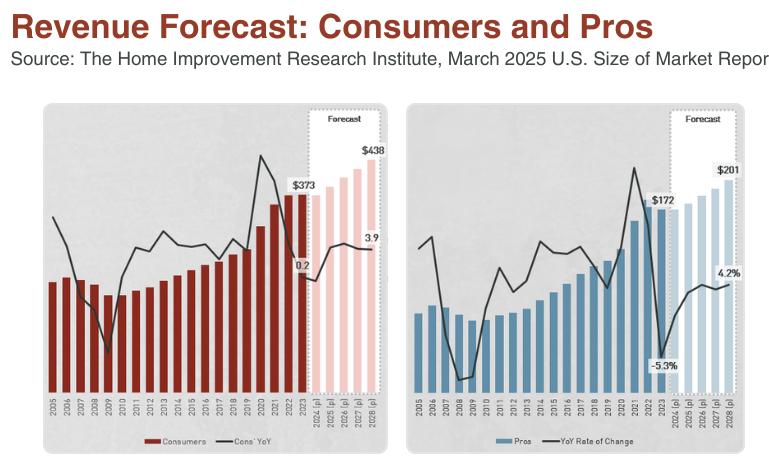

- Market Structure and Trends: The home improvement retail market is highly concentrated, with growth primarily driven by the professional market and e-commerce. According to the Home Improvement Research Institute (HIRI), consumer spending on home improvement products is projected to grow steadily, recovering in 2026 and reaching $449 billion by 2028. Revenue for professional contractors and remodelers is expected to see significant growth starting in 2025, reaching $2.28 billion by 2028. Sustainability and smart home technology drive the home improvement market, with strong consumer demand for eco-friendly and smart products. Home Depot promotes energy-saving products (e.g., LED lighting, water-saving devices) through its Eco Actions program and offers diverse smart home products (e.g., smart lighting, thermostats, security systems), partnering with Google Home and Amazon Alexa for compatibility, aligning with market trends.

Source: Home Improvement Research Institute,thefarnsworthgroup

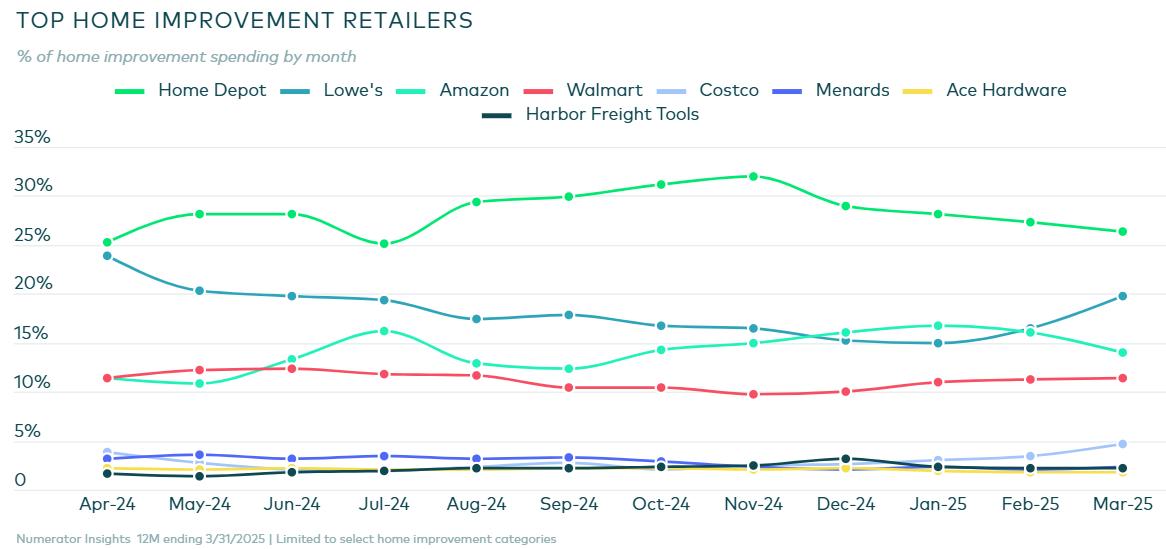

- Key Competitors: The Home Depot’s main competitors include Lowe’s, Amazon, Walmart, and Menards. Lowe’s, the second-largest home improvement retailer in the U.S., operates over 1,700 stores, serving both DIY and professional customers with appliances, tools, and building materials. Menards, a family-owned Midwest chain, runs over 300 stores and attracts DIY enthusiasts and contractors with its low-price strategy, though its reach is limited to the Midwest. Amazon offers a wide range of home improvement products through its online platform, leveraging convenience to draw customers. While not a specialized home improvement retailer, Walmart competes in the DIY market with its extensive network and low-price strategy.

Source: numerator

- Competitive Advantage: Home Depot holds a competitive edge with over 2,300 stores across North America and a strong focus on professional customers (contractors and builders). In 2024, its professional customer segment accounted for over 50% of revenue, with a higher profit margin and a growth rate of 4.4% (compared to 2.8% for the DIY market). Its modernized supply chain and digital capabilities, such as efficient online ordering and fast delivery, create a competitive moat. Through bulk purchasing, customized installation services, and technological innovations (e.g., AR tools and a mobile app with over 1,000 tutorial videos), Home Depot achieves differentiation. Unlike Lowe’s, which focuses on DIY customers, or Menards’ low-price strategy, Home Depot targets high-value customers with premium services and technology-driven experiences.

Revenue Breakdown

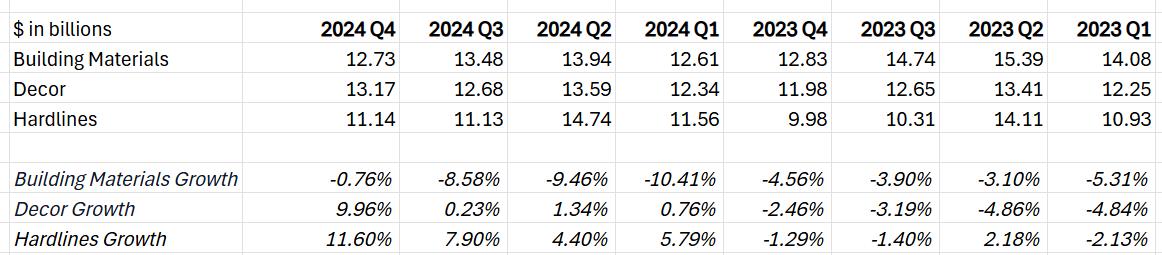

Below is the revenue overview for Home Depot, categorized by major product lines and services:

- Building Materials: High interest rates and inflation have increased borrowing costs, suppressing demand for new home construction and large-scale renovations, putting pressure on sales of building materials such as lumber and masonry. Consumers are leaning toward smaller, less material-intensive home improvement projects, further compressing demand. However, as inflation eases and interest rates gradually decline, the decline in building materials revenue has significantly narrowed, indicating that this segment may have bottomed out and is poised for stabilization and recovery in the future.

- Decorative Materials: In a high-interest-rate environment, consumers are postponing major renovations and shifting toward decorative upgrades, such as smart lighting and modular furniture, driving gradual positive growth in decorative product revenue. In Q4 2024, the decorative category achieved robust growth of 9.96%, with holiday decorations (e.g., Halloween and Christmas products) performing strongly. To reduce reliance on seasonality and attract younger homeowners and renters, Home Depot continues to introduce stylish and convenient decorative products, enhancing market competitiveness.

- Hardlines: Hardware sales are heavily influenced by DIY customers' sensitivity to economic fluctuations, while demand from professional customers remains relatively stable. Home Depot has driven hardware sales growth by strategically focusing on the professional market. The Q4 2024 acquisition of SRS Distribution, followed by the acquisition of professional building products distributor GMS (Gypsum Management and Supply) on June 30, 2025, through SRS, significantly strengthened its service capabilities for professional builders and contractors. This not only enriched the hardware product line but also expanded market share, effectively mitigating risks from seasonality and economic uncertainty.

Source: The Home Depot, TradingKey

From a geographical perspective, Home Depot's revenue is highly concentrated in the U.S. market, accounting for over 90%. The U.S. market has maintained steady revenue growth, driven by the company's increased investment in e-commerce platforms and AI technology, as well as strategic acquisitions (such as the 2024 acquisition of SRS Distribution and the June 30, 2025 acquisition of GMS), which have strengthened its market position. These initiatives have effectively boosted revenue and market share, countering pressures from macroeconomic factors such as high interest rates and inflation.

In contrast, international market performance is limited. A stronger U.S. dollar has reduced the real value of international revenue, while slower economic growth and intensified competition in some regions have further constrained growth. Nevertheless, Home Depot is working to enhance its competitiveness in international markets through optimized supply chains and localized strategies.

Source: The Home Depot, TradingKey

Growth Potential

- Macroeconomic Factors: Easing inflation and declining interest rates are critical to Home Depot's future growth. As interest rates are expected to continue falling and inflation gradually improves, increased consumer disposable income may stimulate housing demand and home improvement projects, directly driving sales growth. In addition, Home Depot's supply chain is highly diversified, sourcing from over 30 countries, with an expectation that no single country's procurement share will exceed 10% in the next 12 months, demonstrates flexible pricing capabilities and resilience to global supply chain fluctuations.

- E-commerce Development: Home Depot continues to invest heavily in e-commerce, particularly in distribution and supply chain management. In Q1 2025, online same-store sales grew approximately 8%, accounting for 15.1% of total revenue. This growth is driven by the company’s optimization of omnichannel services, such as Buy Online, Pick Up In-Store (BOPIS), Buy Online, Deliver From Store (BODFS), Buy Online, Return In-Store (BORIS), curbside pickup, and self-service lockers. These services enhance customer experience and showcase strong inventory integration capabilities. With lower operating costs, e-commerce delivers higher gross margins than physical stores, contributing to overall gross margin and net profit margin improvement.

- AI Technology Applications: AI plays a significant role in Home Depot’s customer service and operational efficiency. In Q1 2025, the company launched “Magic Apron,” a generative AI tool that assists customers with home improvement queries, summarizes product reviews, and provides real-time support, driving an 8% increase in online conversion rates and significantly enhancing the online shopping experience. Additionally, AI tools used by store associates provide quick access to inventory status and product information, improving service efficiency and customer satisfaction. These initiatives not only optimize operations but also indirectly boost overall profitability by increasing gross margins and operating profits.

Source: The Home Depot, TradingKey

Valuation

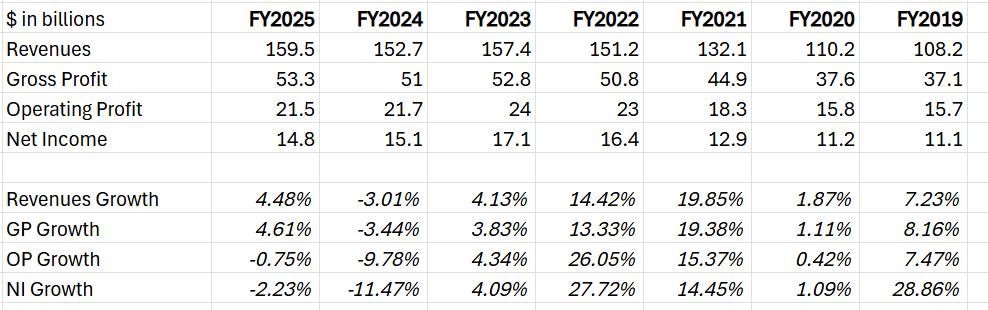

Based on a three-year Discounted Cash Flow (DCF) model, Home Depot has an estimated Enterprise Value (EV) ranging from $401.072 billion to $413.310 billion, comprising a Present Value (PV) of $53.588 billion to $54.477 billion and a Terminal Value (TV) of $395.442 billion to $406.790 billion. The model assumes a revenue growth rate of 2.08% to 3.27%, an operating profit margin of 11.84% to 11.92%, and a discount rate based on U.S. Treasury yields of 3.84% to 4.20% plus a 2% premium. After deducting net debt of $50.897 billion from the EV and dividing by 995 million outstanding shares, the fair value range is $403.09 to $415.39. This valuation fully reflects Home Depot's robust financial fundamentals and sustained growth potential.

Home Depot, with its robust financial performance and consistent growth potential, has garnered significant attention from major institutional investors, including global giants such as The Vanguard Group Inc., BlackRock Inc., and State Street Corporation. Their substantial holdings underscore strong confidence in Home Depot’s long-term value. To explore more about these institutional investors and their investment strategies, stay tuned to TradingKey’s “Star Investors” column.

Risk

- Economic Fluctuations: An economic recession or reduced consumer spending could impact demand for home improvement.

- Supply Chain Disruptions: Global supply chain issues (e.g., transportation delays or raw material shortages) could lead to inventory shortages.

- Competitive Pressure: Intense competition from Lowe’s, Amazon, and others may erode market share.

- Interest Rates: High interest rates could suppress consumer spending on large home projects.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.