GM’s Great Disconnect

- GM trades at a steep discount, with a forward P/E of 5.0x—67% below sector median and 32% under its 5-year average.

- FY2025 EBIT-adjusted guidance was cut by $3 billion –$4 billion due to a projected $4–$5B tariff impact, despite strong U.S. margin performance at 8.8%.

- EV transformation is gaining ground, with 94% YoY EV volume growth, 10.4% U.S. EV share, and 60% conquest customers in Q1 2025.

- AI investments are materializing, with a Chief AI Officer, Super Cruise expansion, and NVIDIA partnership—but monetization remains an open question.

TradingKey - Upon first inspection, General Motors (GM) appears to be a traditional deep value play, priced at 5.0x forward non-GAAP earnings and 0.9x forward EV/sales, and 3.0x forward price-to-cash-flow. On a relative basis, GM finds itself among the cheapest large-cap industrials and far below its historical norms and sector averages. Albeit, valuation in and of itself is not often an actionable catalyst. The question for investors is if GM's low multiples are due to temporary macro distortions, or something of a Upon first inspection,

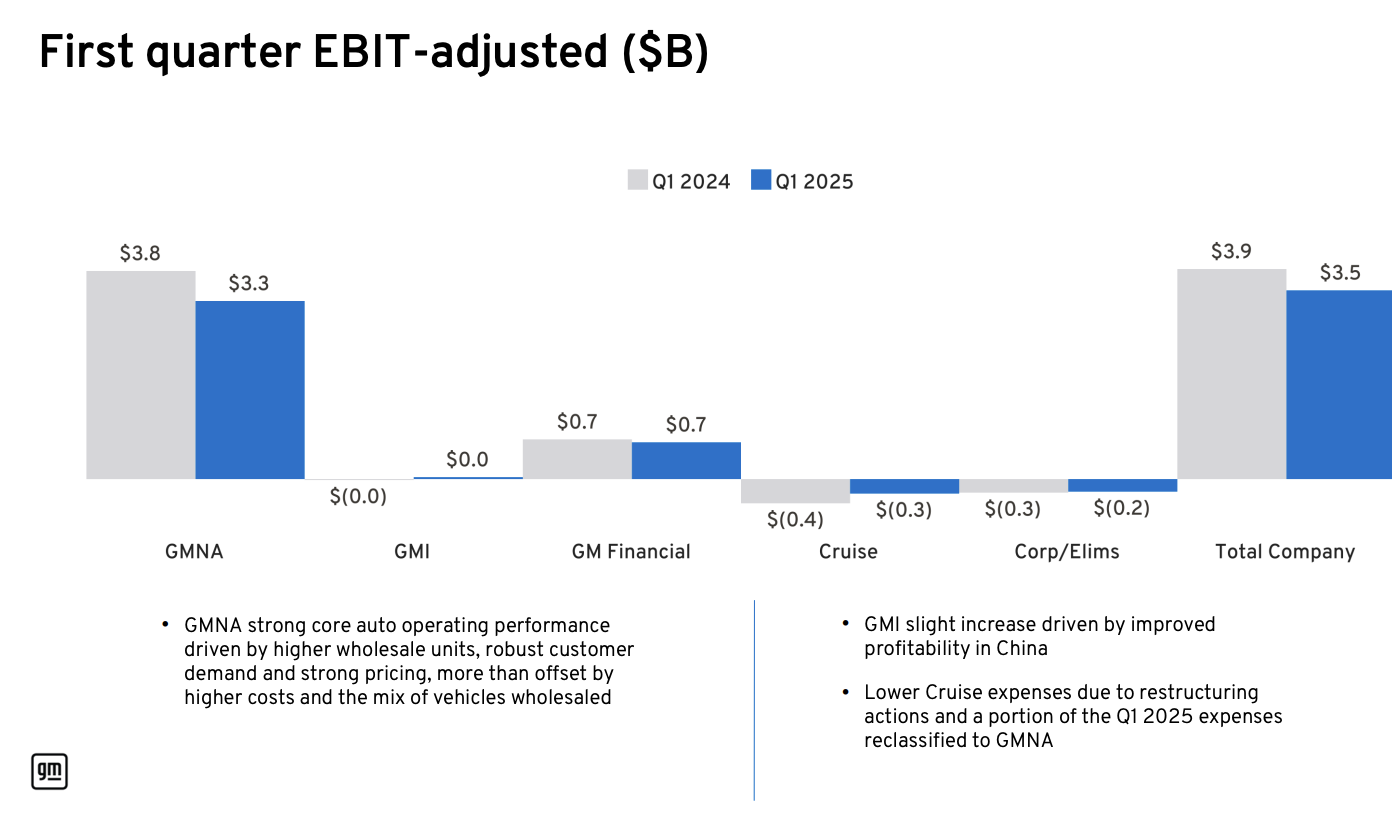

With an increased EBIT-adjusted guide of $10–$12.5 billion for FY2025 reduced from an earlier $13.7–$15.7 billion due to an estimated $4–$5 billion tariff impact,

Source: General Motors Q1 2025 Earnings Presentation

GM is operating in political tailwinds while facing operational headwinds. North America margins remain robust at 8.8%, while in Q1 2025 it registered a YoY market share gain of 180bps in the U.S.

Source: General Motors Q1 2025 Earnings Presentation

With underlying issues arising in compression of free cash flow, China margin vulnerability, and a prudent capital allocation shift, investors need to assess if GM's expanding U.S. EV share and investments in AI can structurally re-rate the business, or if the company is still hobbled by commoditization and geopolitical vulnerability that restrain its valuation multiple.

This piece deconstructs that tension through interrogating GM’s valuation in context: combining Q1 financial performance, operational execution, strategic positioning, and risks associated with political turmoil and technological shift.

Made in America, Fighting Overseas: GM's Strategic Placement Under Pressure

General Motors continues to base its identity in engineering and domestic manufacturing leadership. With 11 assembly plants and more than 50 facilities for manufacturing and parts in 19 states in America, GM has pushed hard into a “Made in America” message, nowpolitically bolstered by recent actions from the Trump administration. These policy changes, to cut tariff stacking and encourage U.S. production, were not simply symbolic victories for GM but necessary offsets. Management projects a $4–$5 billion tariff effect in 2025 but says it can recapture 30% of that cost pressure in production localization and executive exemptions.

This nationalist approach is consistent with GM's five-year investment in U.S. operations of $60 billion and its $10–$11 billion 2025 CapEx plan unaffected by macro uncertainty. Additionally, more than 85% of GM R&D is conducted locally worldwide, and only 3% of direct materials for U.S. production are sourced in China. With one wave of global supply de-risking underway in today's environment, GM looks ahead of the curve in reshoring.

Simultaneously, its international business is also functioning in a vulnerable environment. Though China recovered in Q1 in response to new product offerings and restructuring benefits, its $45 million in equity earnings is a slim addition against a backdrop of increasing geopolitical risk.

.png)

Source: mitrade.com

Outside of China, GM International (GMI) just about broke even in Q1, producing $30 million in EBIT-adjusted. Should China equity earnings or South America growth falter, GM can rapidly see its non-U.S. operations being dilutive rather than additive. The company's balance of domestic strength and global fragility supports its necessity for margin control in its home market in order to counterbalance global volatility.

Source: General Motors Q1 2025 Earnings Presentation

Technology or Transformation? GM's Platform Strategy Put to a Critical Test

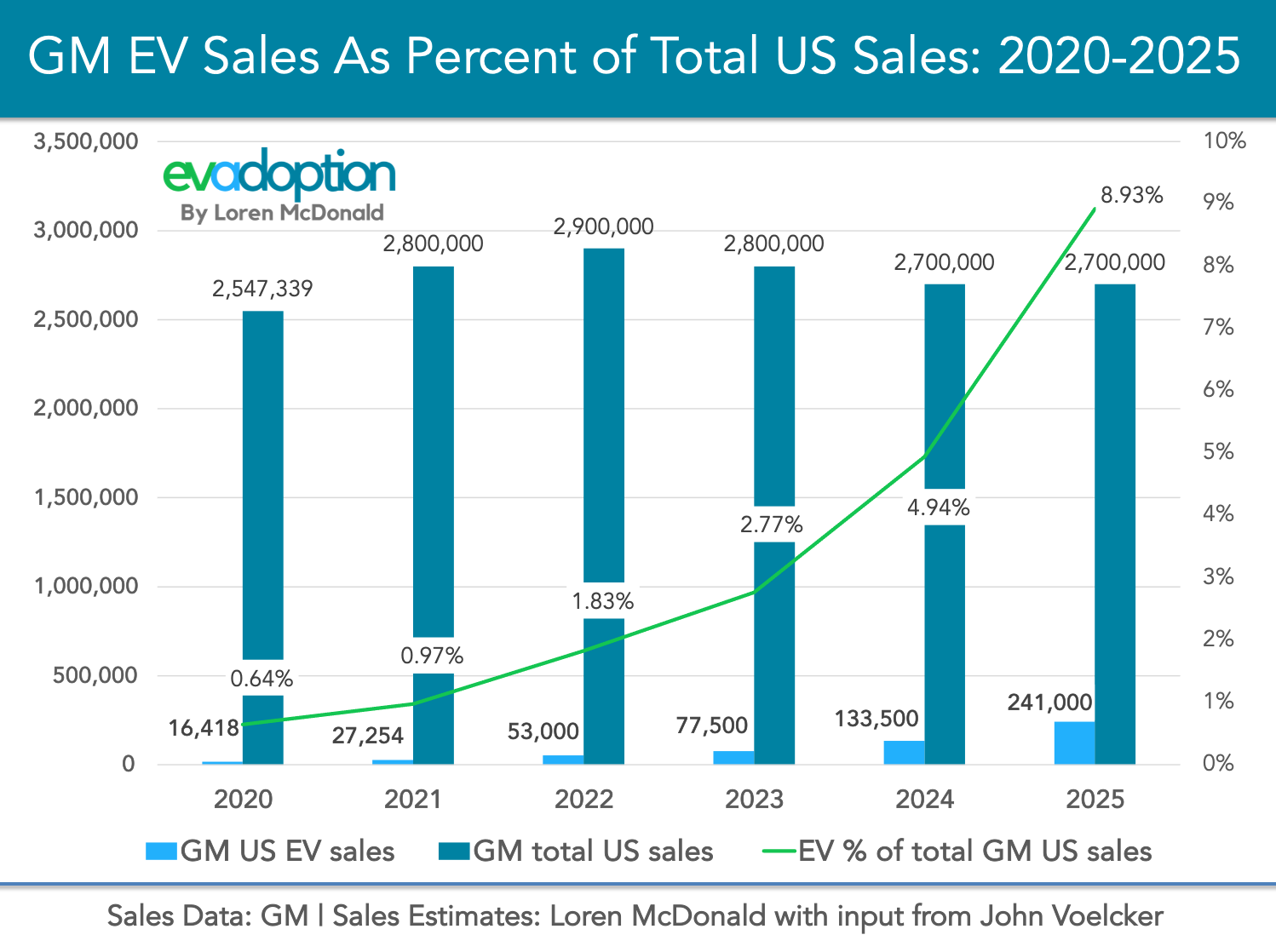

Beneath its historical ICE dominance is an unfolding story about its EV and AI transformation. In Q1 2025, GM captured the #2 U.S. EV sales position, increasing EV volume 94% YoY and achieving 10.4% market share.

Source: evadoption

Chevrolet was particularly notable as it was the fastest-growing EV brand thanks to its Equinox and Blazer EVs. Perhaps most encouraging for GM is that 60% of EV customers were conquest customers, previous non-GM vehicle owners, implying GM’s play is building out its TAM rather than cannibalizing its own base.

Also noteworthy is the traction in Cadillac’s EV pivot, where EVs account for ~20% of U.S. sales and help drive record-high average transaction prices for the brand. The concomitant strength in both luxury and mass-market EVs supports GM’s dual-segment approach. Nevertheless, profitability on EVs continues to elude it. Though management reaffirmed its resolve in preserving EV margins, even if that means forgo short-term volume, the profitability in the full year hinges significantly on volume scaling and optimizing battery cost structures.

Pairing its EV plan is a subtle yet crucial shift toward software-defined vehicles and AI adoption. GM has hired a Chief AI Officer and expanded its alliance with NVIDIA for using AI in simulation, testing, and production processes. Super Cruise, a Level 2 driver assist system, had 100% YoY growth in enabled units and received MotorTrend’s Best Tech Award. GM has also partnered with Cruise for building out L3+ autonomous systems, a significant shift from its earlier robotaxi focus to embedded autonomy.

.png)

Source: evadoption

However, while these AI programs are in place, near-term monetization is limited. GM's actual challenge is one of converting these capabilities into increased revenue per vehicle and reduced production cost, a playbook Tesla has learned but legacy OEMs have not yet cracked.

A Deeper Forensic Reading of GM’s Valuation: The Value Gap Relative to its peers and its historical cost structure, GM appears ridiculously inexpensive. Its forward Non-GAAP P/E of 5.37x is a 67.97% discount to its sector median (16.77x) and 27.11% below its 5-year average. Even its GAAP forward P/E of 5.55x is nearly 69.36% below historical levels. EV/sales forward is 0.93x, substantially below peers and far below 1.16x sector median. Price/book and price/cash flow multiples also reside in the bottom decile of large-cap auto universe.

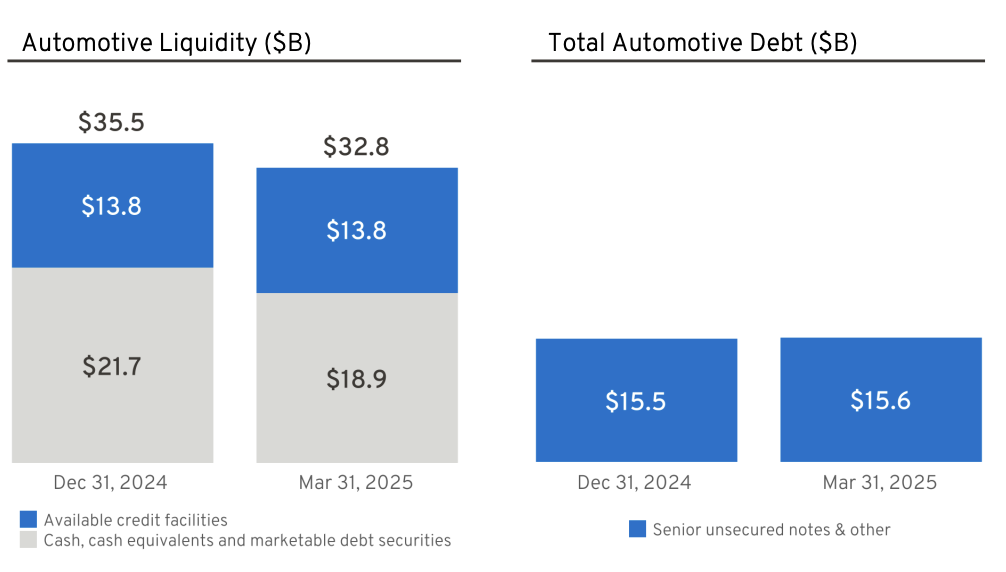

So what accounts for this discount? Some of it comes from GM's dividend yield of just 1.01%, below half of 2.5% for its sector. With just $0.15/share paid for Q2, GM is communicating capital restraint in uncertain times. Meanwhile, its adjusted automotive FCF showed just $0.8 billion in Q1, off 26% from last year due to negative working capital activity related to dealer inventory drawdowns.

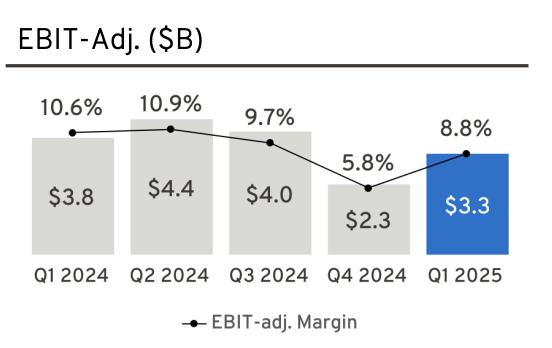

Another hint comes in the form of modest erosion in EBIT-adjusted performance: $3.49 billion in Q1, down 9.8% on a YoY basis. Even as earnings-per-share increased to $2.78 (+6.1% YoY), that increase was fueled more by a declining share count than by organic margin strength. Adjusted return on invested capital skyrocketed to 20.7%, impressive performance, but it’s being helped by declining capital base rather than blowout earnings growth. The threat is that GM’s profitability starts to top out at precisely the time macro risks (tariffs, inflation, global demand) begin compressing free cash flow yield.

A forward-looking perspective should alter GM’s valuation through a sum-of-the-parts framework. If North America continues to yield 8–10% margins and EV mix gets better, one can argue for a target P/E in the 9–10x range based on $9–$10 in EPS. That would suggest a $81–$100-per-share valuation range. But geopolitical surprise, an underwhelming EV ramp-up, or slower AI monetization can keep GM stuck in the 5–6x P/E range, leaving room for downside potential around $40.

Risks: Political Leverage Cuts Both Ways

GM’s near-term perspective is inextricably linked to policymaking. The Trump administration’s announced tariff relief provides precious runway time but also ties GM’s performance to political uncertainty. A shift in the policy landscape, especially if a future administration changes course on tariffs or EV subsidies, would have a material impact on GM’s margins and cash generation.

Also, while Cruise restructuring lowers near-term losses (to -$273 million EBIT in Q1), long-term AV monetization uncertainty persists unresolved. GM steering Cruise toward a support function for Super Cruise and ADAS may cap upside once envisioned through robotaxi platforms.

There is also an underlying risk in EV demand elasticity. GM did take share from its rivals, but its capacity for volume growth while not compromising price is not a certainty as competition increases and wars break out over prices. Cost reductions in batteries will benefit it, but only insofar as volume scales, and GM still lags Tesla and BYD in its integrated battery cost competitiveness for now.

Conclusion

GM’s valuation is cheap but rerating needs proof General Motors is performing in the short term as it captures U.S. market share, rationalizes costs, and maintains healthy EBIT margins. Its EV expansion is tangible, its AI investments legitimate, and its balance sheet is robust. Unless GM can demonstrate sustainable EV profitability and platform leverage through AI and software, the market can all but assign it a structurally discounted multiple. The opportunity is asymmetric, but conviction depends on viewing GM not simply as an automaker, but as a technology-enabling platform company. Only then can valuation alone fuel rerating.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.