Coinbase: The Crypto Stock Even BTC Skeptics Can’t Ignore

Key Takeaways

· Deribit Acquisition: Deribit acquisition expands Coinbase’s dominance in crypto derivatives, adding institutional clients and global reach.

· USDC Revenue: USDC drives steady revenue, with expanding use cases like cross-border payments.

· Valuation Potential: Fair value ranges from $224–$299 based on current growth, with $500+ reflecting long-term growth potential but significant uncertainty.

TradingKey - Picture this: You’re shopping, tap your phone, and buy a coffee with crypto from your digital wallet. Then, you send a payment to a client in Europe, with zero fees, instant transfer. This may sound futuristic, but crypto payments make this happen, although at small scale for now. Step by step, we're building a world where crypto connects everything, and Coinbase is quietly becoming your passport to it.

Source: TradingKey

Deribit Acquisition: A Game-Changer in Derivatives

Coinbase just made a major move acquiring Deribit, the world’s largest crypto options exchange for $2.9 billion. That’s a steal, Coinbase only pays $700 million cash and $11 million shares, when Deribit generates over $100 million each year by estimation. Deribit dominates 80%+ of Bitcoin and Ethereum options trading, with annual volumes exceeding $1 trillion. What does this mean for Coinbase?

· Institutional Clients Boom: Deribit’s users are big players: hedge funds, high-frequency traders, and pro derivatives investors. Coinbase instantly gains these high-value clients. Plus, Deribit’s license helps Coinbase expand into 160+ countries, especially the Middle East and Southeast Asia.

· Profit Boost: Platforms like Deribit usually have 20-40% net margins by industry standard, basically a money printer. This deal will quickly boost Coinbase’s earnings and cash flow.

· Product Suite: With Deribit, Coinbase now covers spot, futures, perpetual contracts, and options, transforming into a full-service crypto financial platform.

Business Segment | Key Move | Why It Matters |

Trading Platform | Integrating Deribit’s derivatives | Now offers all major trading products |

Asset Services | Custodying about $300B+ in assets | Strengthens institutional services & staking |

Lending | Bitcoin-backed loans | Reduces BTC sell pressure while earning interest |

Payments | B2B cross-border settlement network | Bridges crypto and traditional finance |

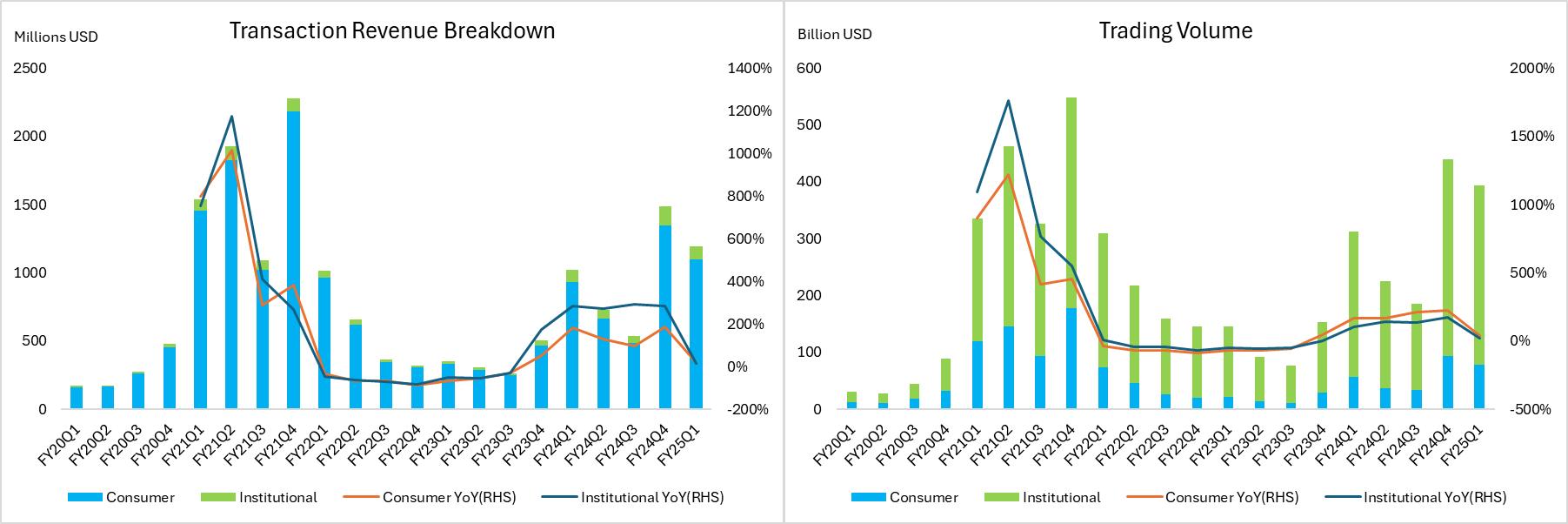

Derivatives are the future of crypto trading, 10 times larger than spot markets. In Q1 2025, Coinbase’s derivatives volume hit $800 billion, although accounting for less than 10% of global crypto derivative market, but growing fast. Full year 2024 Coinbase derivatives volume was only $800 billion.

Still, there are significant challenges. In Q1 2025, Coinbase's institutional trading revenue (including derivatives) dropped 30%, much worse than the 9% decline in trading volume. Their aggressive rebate program to attract clients is the reason, Coinbase offered big discounts to institutional traders, sacrificing short-term revenue. It's a risky move, betting on market share over immediate profits.

Source: Coinbase Earnings Report, TradingKey

Integrating Deribit's technology, team and customer base will also take time, and poor execution could hold them back. Plus, Deribit hasn't entered the U.S. due to strict regulations. But with Coinbase's own compliant options products and the Trump administration's crypto-friendly approach in 2025, new opportunities might open up. If Deribit's options can enter the U.S. legally, Coinbase's revenue could get another big boost. It's a high-risk, high-reward bet that's worth watching.

USDC: The Cash Cow Defying the Market Downturn

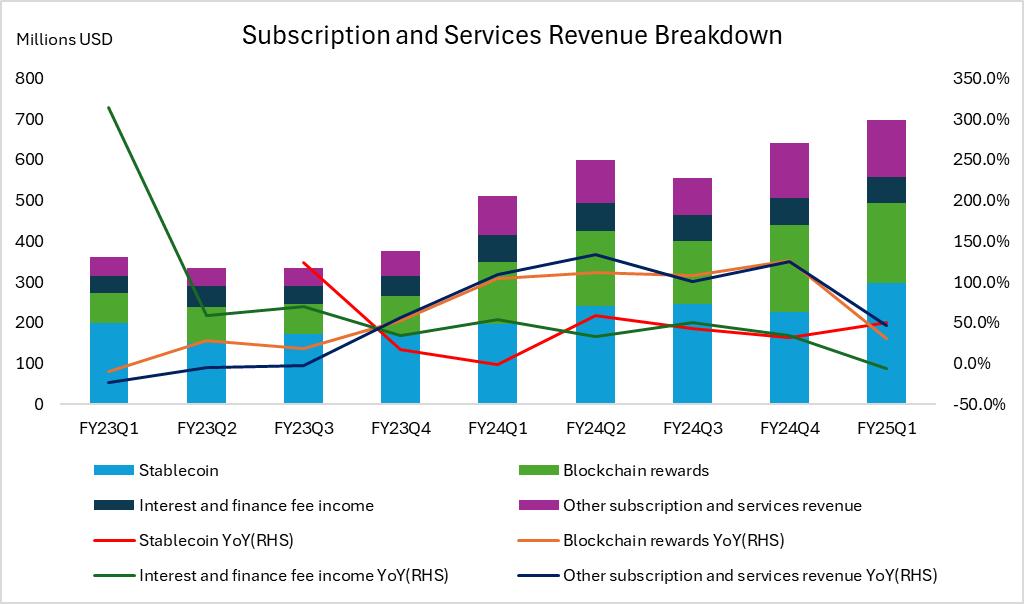

Let’s talk about USDC, the stablecoin that’s been carrying Coinbase’s earnings this quarter. The crypto market has been in a bear market since December. Bitcoin and altcoins went down nearly 20% and trading volume shrank, while USDC’s holdings and circulation have exploded. Why? Because when markets get shaky, investors rush to stablecoins for safety, and USDC, as the most transparent and compliant option, becomes the go-to shelter.

Source: Coinbase Earnings Report, TradingKey

In Q1 2025, USDC balances on Coinbase skyrocketed to $123 billion, up 50% YoY. That directly boosted revenue, making it a true cash cow. Importantly, Coinbase’s own USDC holdings, those not loaned out or pledged as collateral, also saw a significant increase, nearly doubling from $743 million in Q4 to $1.86 billion in Q1. Even as trading fees dipped in the weak market, USDC-related income dominated Coinbase’s non-trading revenue, keeping things steady.

Source: Coinbase Earnings Report, TradingKey

How Does Coinbase Make Money with USDC?

For every USDC issued, there’s real USD and U.S. Treasury bonds backing it, and those assets earn interest. Coinbase has a nice deal with Circle (USDC’s issuer):

· USDC in Coinbase Products: Coinbase keeps 100% of the interest

· Off-platform USDC: Coinbase gets 50% of the interest

Source: Coinglass

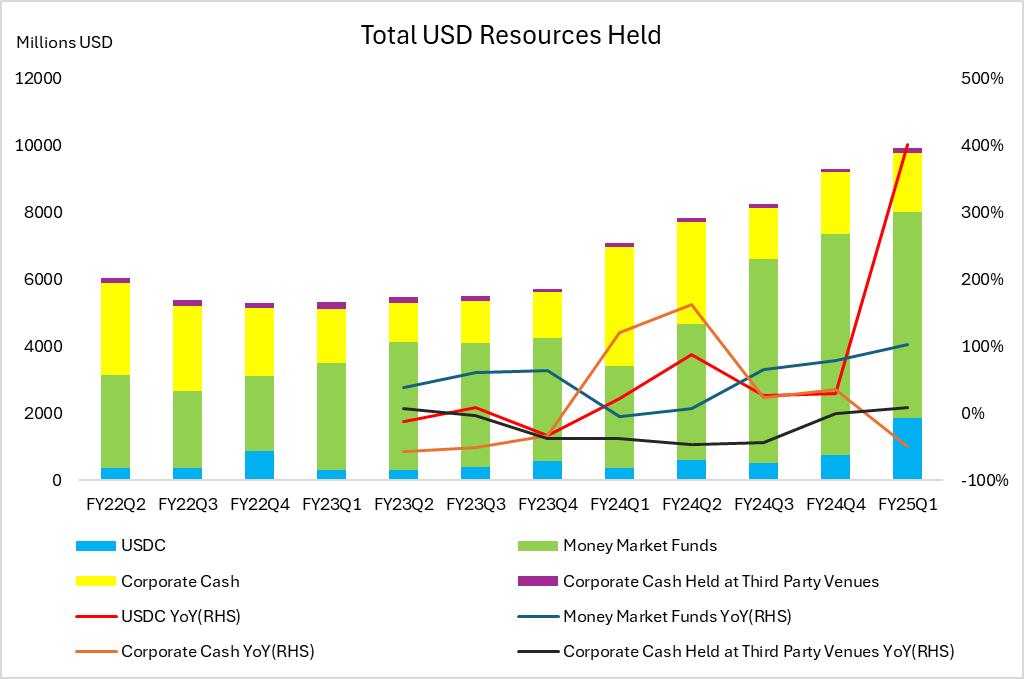

That’s huge money. Compared with USDT, there is still a lot of room to grow. With USDC’s weekly trading volume hitting $24 billion, the more it circulates, the more interest piles up, and the more Coinbase earns.

More Than Just a Safe Haven

Coinbase’s vision for USDC is very big. They are building a global payment network. Traditional dollar transfers rely on banks which have slow networks, taking days with high fees. USDC payments are peer-to-peer, settling in seconds at a fraction of the cost.

In Q2 2025, Coinbase is testing USDC payments for businesses. Imagine an e-commerce store using USDC for cross-border orders, instant, cheap, no bank hassle. That’s their Crypto as a Service play: turning USDC into an everyday tool.

Additionally, there is another innovation here: crypto loans. Got Bitcoin but don’t want to sell? Use it as collateral on Coinbase to borrow USDC, up to 70-80% of your BTC’s value. You keep your coins, and Coinbase earns interest. It can also stabilize BTC price, but there’s a catch: If BTC price drops, the value of the collateral may no longer cover the loan amount, triggering forced liquidation.

Looking ahead, USDC has the potential to become the de facto digital dollar. Coinbase is working with BlackRock, Stripe and other institutions to promote its application in mainstream finance. The expansion of stablecoin use cases has enabled Coinbase to gradually transform from an exchange to a core provider of crypto financial infrastructure.

Crypto-as-a-Service: Coinbase's Infrastructure Ambition

Coinbase isn't just an exchange anymore. It’s building the infrastructure of the crypto economy. Their Crypto-as-a-Service strategy works like SaaS, providing ready-made blockchain infrastructure to businesses. Here's how it works:

· Payment Network: Stablecoin-powered global settlement system

· White-label Solutions: Companies can rebrand Coinbase's tech to launch their own crypto products overnight (e.g. banks launching wallets without building from scratch). Coinbase makes money through licensing fees and service fees.

· Developer Tools: APIs/SDKs for easy integration of USDC payments, crypto loans, and trading (e.g. an e-commerce site can add crypto payments with just a few lines of code)

· Compliance Hub: Leveraging licenses Coinbase have to help clients navigate global regulations.

This turns Coinbase into the “pickaxe seller” of crypto. Businesses save millions on development costs. Developers build dApps faster, and Coinbase collects recurring service fees, which is more predictable than volatile trading revenue, like SaaS subscription fees.

Valuation: What's Coinbase Really Worth?

Coinbase's real strategic ambition is to become a leading infrastructure provider in the field of crypto. This is very similar to AWS's role in the field of cloud computing. AWS has grown from a business unit within Amazon to a global leader in cloud computing infrastructure, completely changing the IT architecture of enterprises. Similarly, Coinbase is committed to building the blockchain infrastructure of Web3 to support the underlying operation and innovative development of the decentralized ecosystem. Both provide essential basic resources and technical support for applications and services. AWS enables enterprises to quickly build and deploy Internet services, while Coinbase enables blockchain applications and financial services to run securely and efficiently.

When valuing Coinbase's future potential, Amazon's P/E valuation method can act as reference when AWS became well-known in 2015-2016. In 2015, the market began to pay close attention to the explosive potential of high-growth businesses such as AWS. Although Amazon's e-commerce business was still in loss at the time and AWS's profits were not that significant, the market was willing to pay a very high premium for such growth businesses, resulting in Amazon's overall P/E exceeding 500x in 2015. By 2016, AWS began to make a substantial profit, with the company's overall net profit reaching $2.37 billion. AWS's net profit was about $2 billion, which almost contributed to all Amazon's profits. Therefore, Amazon's overall 150 times P/E in 2016 reflects the growth value of AWS. Although it is still high, it was more reasonable.

This analogy is not only because both are infrastructure platforms that support the prosperity of applications and ecosystems, but also because they are at the forefront of technological innovation and market change. The complexity and innovation needs of blockchain infrastructure are similar to the technical challenges and market opportunities faced by early cloud computing. Coinbase's infrastructure business is still in a very early stage, with huge opportunities, but it also faces high risks such as crypto market volatility, regulatory uncertainty and competitive pressure.

Considering these factors, the market's recognition of Coinbase's valuation is still cautious. Historically, Coinbase's P/E has fluctuated between 30 and 40 times.

In the most optimistic scenario, Drawing from AWS's early high-growth phase has a P/E ratio of around 150 times as the market recognizes its disruptive potential. In contrast, we set a more conservative P/E range of 70 to 100 times for Coinbase. This reflects Coinbase's huge growth opportunity as a Web3 infrastructure provider, but also explains its smaller scale, regulatory risks, etc.

Scenario | P/E | Target Price | Conditions |

Conservative | 30x | $224 | Market cautious due to crypto volatility, regulatory uncertainty, and intense competition; limited growth expectations |

Base Case | 40x | $299 | Assumes stable growth with easing regulatory risks and manageable competition |

Growth Premium | 70x-100x | $520-740 | Market fully values Coinbase’s potential as a leading Web3 infrastructure provider |

Under Growth Premium Scenario, high valuation range reflects the theoretical value if the market fully recognizes the potential of Coinbase's infrastructure business, Coinbase as the AWS of Web3, while also reflecting the constraints on valuation imposed by current industry volatility and regulatory risks. The gap between current and potential valuation reflects the debate.

Conclusion: Coinbase Is Your Ticket to Crypto's Future

At current prices, Coinbase looks undervalued. It is pivoting from being just an exchange to becoming a full-spectrum crypto financial services provider. Cooperation with Circle on USDC allows it to make steady profits amid market turmoil, the Deribit acquisition opens the door to the derivatives market, and the infrastructure potential puts it at the forefront of the global financial game. Yes, risks exist, but if you believe in crypto’s long-term potential, Coinbase offers a clear path to exposure. Think of it as guaranteeing early access to the next financial system.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.