[IN-DEPTH ANALYSIS] McDonald's: The Property Empire Buffett Kicks Himself for Missing

TradingKey - When you hear the name McDonald’s, who doesn’t think of crispy golden fries, the mouthwatering Big Mac, or those irresistible Chicken McNuggets? It’s not just the “big brother” of the global fast-food industry—it’s a culinary symbol etched in countless memories. But for investors, McDonald’s is far more than a burger joint. It’s a “landlord,” steadily collecting “rent” by leasing out its brand and operating rights. Perhaps even the Oracle of Omaha, Warren Buffett, regrets not snapping up this stock sooner. Why? Because McDonald’s has mastered a unique business model—franchising—that has blossomed globally, raking in profits hand over fist.

Source: TradingKey

Who Is McDonald’s? The Fast-Food “Landlord”

Picture this: you walk into a McDonald’s, order a classic combo, and take that first bite of fries. In that moment, do you realize that behind McDonald's success lies a secret more lucrative than burgers? McDonald's owns 57% of its restaurant land and 80% of its properties, with land and properties, accounting for roughly 60% of its total assets—a true wealth cornerstone. Nearly 95% of McDonald's restaurants worldwide are operated by franchisees, who pay rent and royalties to McDonald's. Rent alone makes up 64% of franchisee revenue, equating to about 40% of total revenue. McDonald's business model goes beyond selling fast food; through franchising and real estate, it transforms into a "savvy landlord." By leasing its brand and properties to franchisees, McDonald's secures steady income, thriving in any economy, with rent flowing in even while the world sleeps.

Source: Price to Wealth

So, how does this “landlord” operate? To understand McDonald’s money-making magic, we need to dive into its two operating models: company-operated and franchised. These are like McDonald’s “dual identities,” each with its own strengths, but franchising is the true core of its empire.

McDonald’s “Dual Identities”

McDonald’s restaurants come in two flavors: those it runs itself (company-operated) and those it “leases” to others (franchised). These two approaches shape McDonald’s profitability in distinct ways.

Company-Operated Restaurants: These are restaurants McDonald’s owns and operates, footing the bill for opening, staffing, and sourcing ingredients. The upside? Full control over quality, ensuring every burger tastes authentic and every fry is perfectly crisp. The downside? High costs and slow expansion. It’s like running your own restaurant—potentially profitable but labor-intensive.

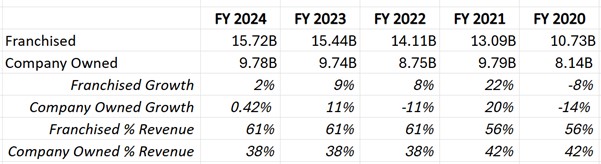

Franchised Restaurants: Franchising is a different beast. McDonald’s “leases” its brand, menu, and operational know-how to franchisees, who pay an initial franchise fee, a percentage of sales as royalties, and, in many cases, rent for properties owned by McDonald’s. As of Q1 2025, over 95% of McDonald’s nearly 44,000 global restaurants are franchised. In other words, most of its revenue doesn’t come from selling burgers but from “collecting rent.”

Source: MCD, TradingKey

Company-Operated vs. Franchised: Which Is More Profitable?

Clearly, franchised restaurants outshine company-operated ones in profitability. Company-operated restaurants face volatile profit margins due to bearing all costs—labor, ingredients, and rent—resulting in razor-thin margins. In contrast, franchised restaurants boast profit margins five to six times higher, resembling a smooth, high-speed highway with minimal fluctuations. Since Q2 2024, franchised margins have stabilized around 84%, while company-operated margins have been declining. Even amid rising costs and intensifying competition, franchised restaurants remain rock-solid, while company-operated ones struggle to keep up, highlighting the power of the “landlord” model.

Source: MCD, Bernstein analysis

This trend makes it clear: franchising is McDonald’s “money tree.” Why? Let’s break it down:

Stable Revenue: Franchising is like collecting monthly rent—franchisees must pay royalties and rent regardless of economic conditions. Over the past few years, McDonald’s has reaped massive profits from this stream, as steady as a bond.

Source: MCD, TradingKey

Low Costs: Unlike company-operated restaurants, where McDonald’s foots the bill for all expenses, franchising outsources these costs to franchisees. As McDonald’s scale grows, it relies on standardized processes and oversight systems, slashing administrative costs as a percentage of revenue.

Source: MCD, TradingKey

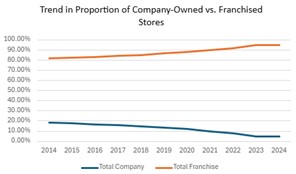

Rapid Expansion: Franchising allows McDonald’s to expand globally at lightning speed. Over the past decade, McDonald’s has steadily reduced the proportion of company-operated restaurants while boosting franchised ones. Data shows the franchised restaurant share rose from about 81% in 2014 to 95% in 2024, while company-operated restaurants dropped from 18% to 5%. With franchisees’ capital, McDonald’s expansion is like riding a SpaceX rocket.

Source: MCD, TradingKey

Low Risk: Franchising turns McDonald’s into a “light-asset” company, with franchisees bearing opening and operating risks. Often, McDonald’s doesn’t even need to buy land or build restaurants—franchisees handle that. Even when McDonald’s owns properties, it can shift risks through long-term leases. This model significantly reduces capital expenditures (e.g., for new stores), keeping costs low.

McDonald’s “Health Check”

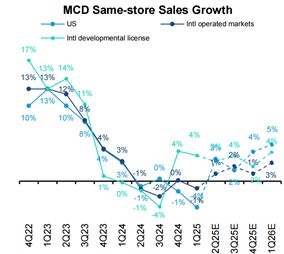

Same-Store Sales Expected to Rebound: Q1 2025 started on a weak note, with global same-store sales (SSSG) declining 1.0%. The U.S. market fell 3.6%, driven by reduced traffic from low-income consumers. The International Operated Markets (IOM) also dropped 1.0%, dragged down by weak U.K. performance, while the International Developmental Licensed Markets (IDL) grew 3.5%, fueled by strong results in the Middle East and Japan, with China remaining stable. Franchised revenue remained robust. Management noted significant improvement in April, signaling the year’s low point has passed, with the U.S. $5 Meal Deal showing early success and new products expected to drive a rebound.

Source: MCD, Bernstein analysis

Source: MCD

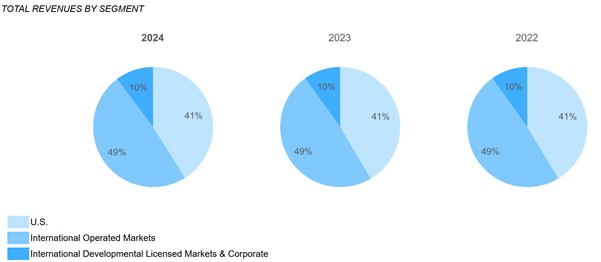

Global Expansion Continues: McDonald’s global expansion shows no signs of slowing, aiming for 50,000 restaurants by the end of 2027. In 2025, the company plans to open 2,200 new restaurants, with over 1,600 in IDL markets, led by China’s projected 1,000 openings. The U.S. and IOM markets will add 180 and 420 restaurants, respectively, accounting for 8% and 19% of the total. Net additions of about 1,800 restaurants will drive a 4% increase in total units. This expansion will significantly boost franchised revenue, particularly in high-potential markets like China, injecting new momentum into 2025 performance and further solidifying McDonald’s global market position.

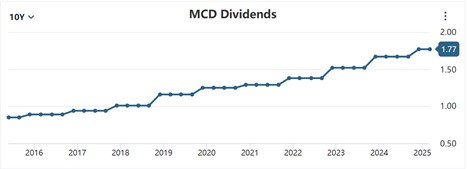

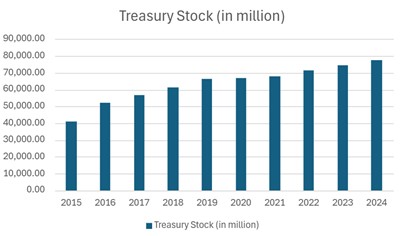

Shareholder-First Approach: McDonald’s dividend policy and share buyback strategy reflect its commitment to long-term shareholder value. In September 2024, the company raised its quarterly dividend by 6% to $1.77 per share, equating to an annualized $7.08, maintaining a 49-year streak of increases since 1976, underscoring financial stability. Additionally, ongoing share buybacks reduce outstanding shares, boosting earnings per share and stock price. Even during the 2020 pandemic, when buybacks were paused, dividends remained intact. This dual strategy of dividends and buybacks delivers consistent returns, ideal for investors seeking stable, long-term gains.

Source:Stockanalysis

Source:MCD, TradingKey

McDonald’s Valuation and Risks

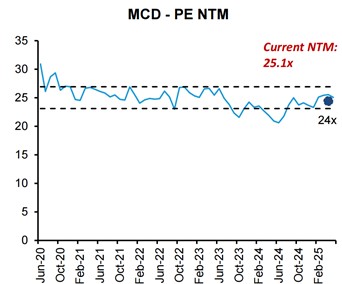

Despite recent softness in revenue and same-store sales (SSS), McDonald’s remains a rock-solid giant, thanks to its “landlord” franchising model. This model makes McDonald’s more resilient than peers during economic volatility, a true “anchor” in the fast-food industry. Even as industry traffic faces pressure, McDonald’s leverages cost-effective promotions (like “Buy One, Add One for $1”) and innovative menus to attract customers and gain market share. We maintain a neutral-to-optimistic rating on McDonald’s, projecting a 12-month target price of $350 based on a 25x P/E ratio.

Of course, investing in McDonald’s isn’t without risks. A worsening macroeconomic environment could tighten consumer wallets, intensified industry competition may pose challenges, and geopolitical or regulatory changes (especially in IDL markets like China) could impact expansion plans. However, with its powerful brand and flexible operating strategy, McDonald’s has a knack for weathering storms.

Source: MCD, Bernstein analysis

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.