Visa Q2 FY2025: Infrastructure-Grade Moat or Earnings Mirage?

Key points:

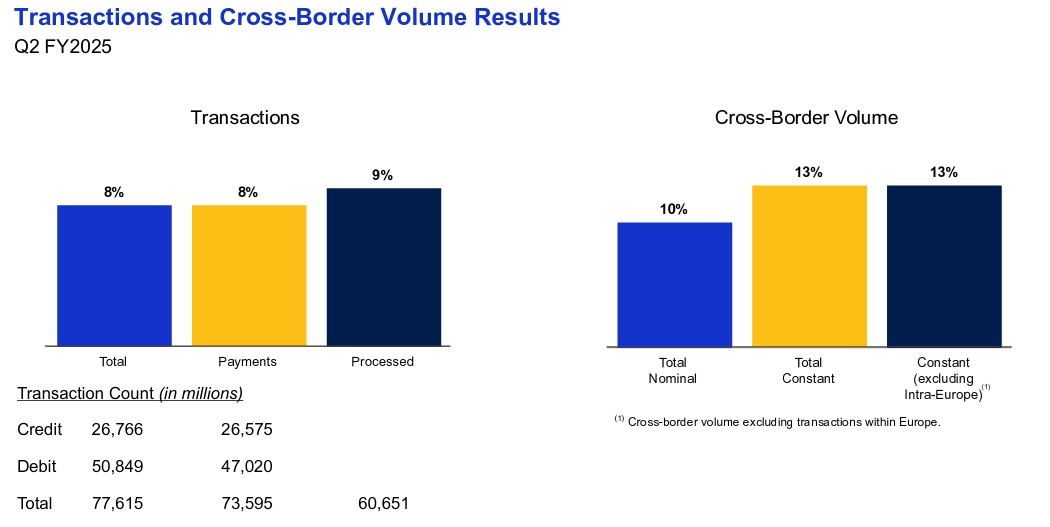

- Visa processed 60.7 billion transactions in Q2, up 9% YoY, with cross-border volumes rising 13% in constant dollars.

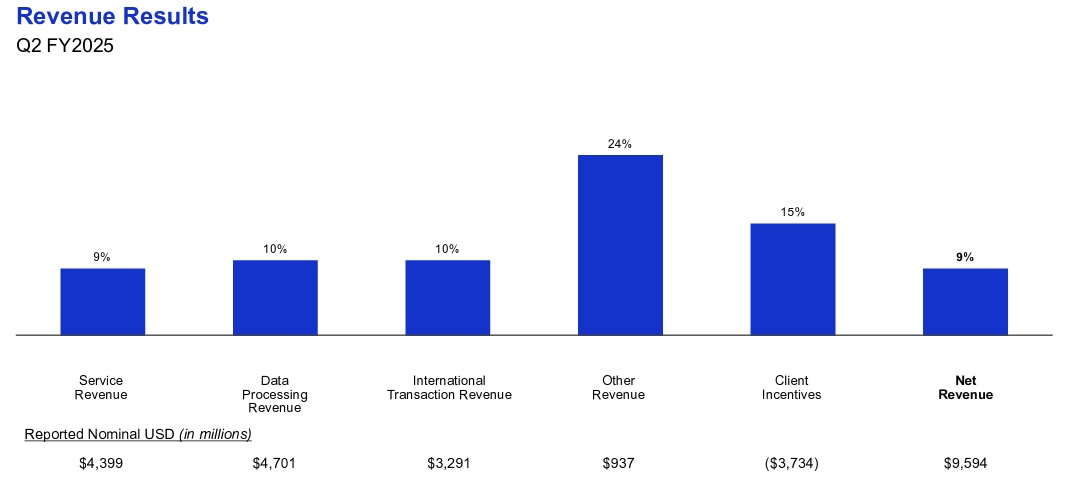

- Net revenue grew 9% to $9.6 billion, while constant-currency growth of 11% highlights demand resilience beyond FX impact.

- Free cash flow reached $4.37 billion, with $5.6 billion returned to shareholders through buybacks and dividends in Q2.

- “Other revenue” rose 24% YoY, reflecting growth in risk, consulting, and embedded APIs that boost customer stickiness.

- Visa trades at 29.94x forward P/E, 191% above sector median, while its price-to-book exceeds peers by over 1,400%.

TradingKey - Visa's (V) Q2 FY2025 results reinforce its position not only as a payments processor, but also as the embedded trust layer of global commerce. While the market views Visa as a mature, low-growth financial stock, its fundamentals highlight a platform increasingly integral to cross-border money movement, fraud detection powered by AI, and tokenized authentication.

This is not merely about transactional scale, it's about infrastructural salience. Processing 60.7 billion transactions during the quarter, a 9% year-over-year increase, and cross-border (excluding intra-Europe) up 13% in constant dollars, Visa continues to entrench itself geographically and by vertical.

Source: Visa IR

Yet, investors need to balance this remarkable operating rhythm with rising litigation provisions, regulatory headwinds, and a more contested value chain. Visa's $992 million quarter-ending litigation charge, its highest in years, diluted GAAP income growth and obscured perceptions of earnings quality. After adjusting for that noise, the company still delivered 12% constant-currency EPS growth and $4.4 billion in free cash flow, affirming monetization strength. In an era dominated by AI-native platforms, Visa's transformation from a payments gatekeeper to data, security, and network-services platform demands a reframed investment thesis.

The market's valuation assumptions, usually driven by narratives of decelerating total payment volume growth and regulatory pressure, do not fully reflect Visa's reinvention. This quarter's 8% constant-dollar payment volume growth was not influenced by inflation, but instead by commercial flow expansion and structural growth through embedded finance partnerships. As capital rotates toward generative AI and fintech infrastructure, Visa merits reclassification, not as a slumbering cash cow, but as a smart allocator of capital with a widening algorithmic moat.

From Plastic to Protocol: Visa's Reinvention Engine

Visa’s business model remains deceptively simple: monetize each interaction in a four-party framework of issuers, acquirers, merchants, and cardholders. But the architecture is undergoing a strategic overhaul. Growth at the core is no longer driven by incremental card issuance or geographic expansion. Instead, Visa is now rolling out network intelligence to guard its future in a tokenized, cross-platform environment.

On the surface, the figures appear stable. Net revenue climbed 9% year-over-year to $9.6 billion. More significant, however, is the 11% constant-currency growth, a clear sign that macro FX noise is not hindering demand. International transaction revenue increased 10% to $3.3 billion on the back of 13% cross-border volume growth. Alpha lies in the processed transactions - 60.7 billion during the quarter - demonstrating Visa’s operating depth and technical scalability.

Source: Visa IR

What separates Visa structurally is its capacity to turn volume into margin-laden revenue without proportional CapEx. For instance, on 9% revenue growth, operating expenses in constant currency increased just 7%, underscoring cost discipline even with international expansion. Particularly notable is 24% year-over-year growth in “other revenue,” which signals increasing traction from non-transactional offerings such as risk management, consulting, and embedded APIs. These drive stickiness without displacing existing products.

Source: Visa IR

One core strategic strength is Visa’s ability to serve as the default switch for fintechs and wallets. In the CEMEA region, payment volume rose 15.3%, while overall volume increased 10.2% this quarter. Geographic diversification is reinforced by AI-driven fraud analytics and intelligent routing, effectively guarding against disintermediation. As digital wallet adoption accelerates and real-time payment spread, Visa's software-first, tokenization-based architecture remains a defensible moat.

Scale vs. Disruption: Redefining the Market in Progress

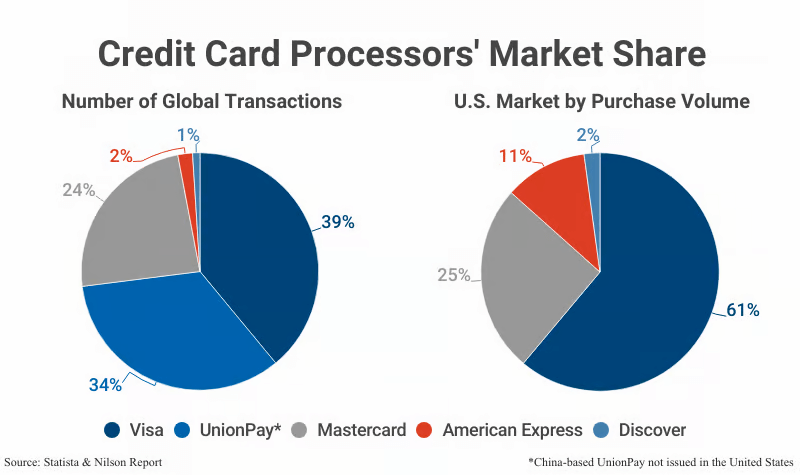

Competition in payments has never been more intense. From Apple Pay’s rising contactless share to Stripe’s programmable infrastructure dominance and regulator-backed real-time payment schemes, Visa’s dominance is being challenged. But Q2 results reveal that Visa is not merely maintaining its share, it’s subtly redefining it.

Source: Capital One Shopping

International debit programs expanded 9.8% YoY in constant currency, even outpacing credit volume. This is significant as debit is more defensible against disruptors due to regulatory and clearing barriers. Visa is also gaining share in commercial payments, a high-margin space often overlooked by consumer-facing metrics. Embedded finance partnerships with Shopify and Square give Visa a “silent protocol” advantage. Even when not visible to users, Visa often powers the underlying rails.

Pricing-wise, Visa is handling fee compression better than peers. Client incentives rose 15% YoY, yet total revenue outpaced incentives, implying higher pricing leverage or improved volume mix. This is in contrast to PayPal where branded checkout is eroding and take rates are falling. Visa’s processing cost-to-revenue growth remains consistent, unlike Stripe, which is scaling with declining contribution margins.

AI further reinforces Visa’s moat. Visa's use of AI across fraud detection, tokenization and transaction monitoring at scale distinguishes it from incumbents and upstarts alike. While many startups promote automation, few deliver Visa's combination of low latency and high trust, qualities that matter most to large financial institutions and regulators.

Cash Flow, Return of Capital, and a Latent Layer of Efficiency

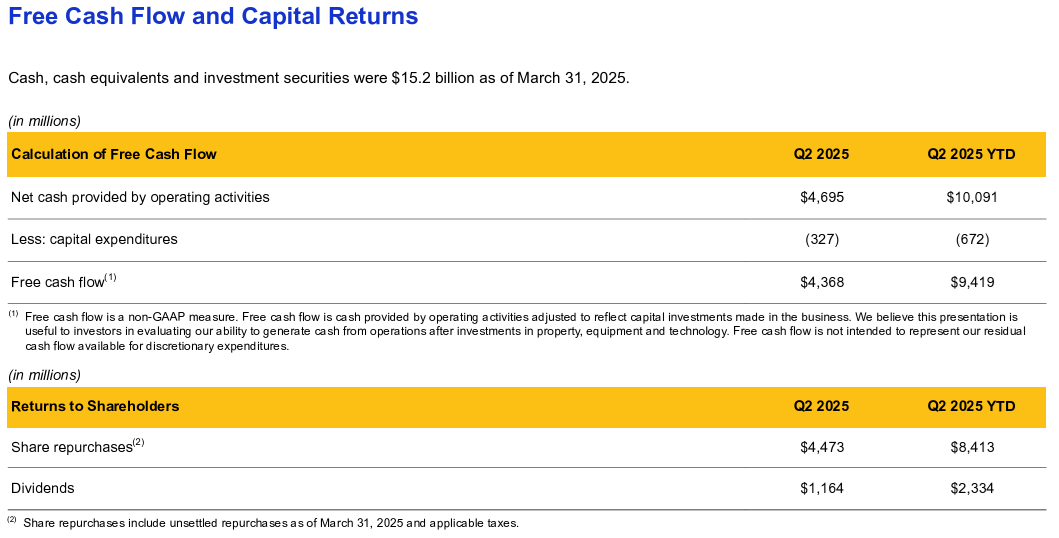

Visa’s platform strength is matched by disciplined capital deployment. Free cash flow in Q2 reached $4.37 billion, up 9.4% YoY, driven by $4.7 billion in operating cash flow and just $327 million in CapEx. WIth over 45% FCF margins, Visa converts volume into cash more efficiently than almost any platform business out there, including Apple and Meta. This isn't just operational discipline, it's financial precision.

Capital returns remain aggressive and calculated. Visa repurchased $4.5 billion in stock at an average price of $340.26 and approved a fresh $30 billion buyback. Combined with a $1.16 billion dividend payout, Visa returned $5.6 billion to shareholders, nearly 60% of quarterly revenue. With $15.2 billion in cash and investments and a conservative leverage profile, Visa has flexibility for acquisitions or accelerated buybacks if valuation dips.

Source: Visa IR

The $992 million litigation reserve, while intimidating on the surface, reduced GAAP profits by just 2%. GAAP profits by just 2%. On a normalized basis, non-GAAP EPS rose 10% year-over-year. Visa has built a litigation escrow fund to shield core shareholders from MDL risk. In March, it added $375 million to that fund and retired shares through accounting adjustments tied to B-1 and B-2 share classes.

As for expenses, Visa is containing cost pressure with scalpel-like discipline. While GAAP operating expenses rose 22% due to litigation, non-GAAP expenses increased just 7%, mainly from marketing, personnel, and depreciation. Notably, Visa maintains one of the lowest CapEx-to-revenue ratios among large-cap tech, reflecting high incremental margins and minimal reinvestment drag.

Rerating Potential: Unpacking the Valuation Enigma

Even with operational power, Visa trades at a rich premium. This raises questions about margin of safety and upside potential. On every significant metric, Visa is trading above both its sector median and its own 5-year average, with a valuation profile that is closer to that of high-growth tech business than a stable compounder.

Visa’s trailing 12-month non-GAAP P/E of 32.48 is 197% above the sector median. Forward non-GAAP P/E sits at 29.94, also reflecting a 191% premium. These are close to Visa’s 5-year average of 31.26, but still imply near-flawless execution.

GAAP-based multiples are similarly elevated. Visa’s forward GAAP P/E of 30.66 is 187% higher than the sector median. These valuations price in perfect continuity, downplaying regulatory risk or potential margin erosion.

The PEG ratio, which is a useful gauge of valuation vs. growth, tells a similar story.isa’s GAAP PEG (TTM) of 2.40 is 267% higher than the sector average. Its forward non-GAAP PEG of 2.35 suggests that growth is fully priced in. This is important because Visa’s core growth drivers - cross-border, AI implementation, and commercial flows - are yet to overcome macro, regulatory, and competitive risks.

The most glaring signal is Visa’s price-to-book: 17.65x trailing and 17.41x forward, that is more than 1,400% above the sector median. Such valuations are rarely sustained without significant growth inflection or margin expansion. Visa’s forward dividend yield of just 0.68%, versus a sector median of 3.49%, adds to the valuation risk for income-oriented investors.

Source: Guru Focus

In sum, Visa’s premium valuation reflects its quality, but leaves little room for positive surprises. For investors focused on margin of safety, these multiples may justify trimming and reallocating to similarly advantaged names with better entry points.

Risk Factors: Regulation, Litigation and Disintermediation

Visa's investment case is not without its risks.Regulatory scrutiny is intensifying in the U.S. and EU, especially around interchange fees and anti-steering rules. Visa’s current antitrust lawsuits, particularly its MDL case, could lead to fee caps or forced unbundling of value-added services.

Moreover, real-time payment schemes like FedNow (USA), PIX (Brazil), and UPI (India) may also circumvent Visa's rails in case of government-sponsored schemes. In case such models gain broad traction, Visa’s domestic transaction margin may be compressed meaningfully, especially in debit-dominant markets. TTechnological disruption from programmable protocols and stablecoin networks presents long-term risk. While Visa is piloting stablecoin settlements, and tokenized payment transactions, the risk of being outrun by open-source networks exists. Last, Visa's reliance on third-party processors, banks, and ecosystem partners exposes it to slowdowns in fintech growth or general banking crises.

Conclusion: Visa Remains An Infrastructure Compounder In Disguise

Visa's Q2 FY2025 results reaffirm its status as a high-margin, capital-light compounding platform masquerading as a financial stock. Beneath the litigation noise is an asset-light network monetizing scale, trust, and latency with unrivaled efficiency. With an expanding AI-enabled service layer, disciplined capital returns, and growing international presence, Visa remains structurally advantaged, even in an era of disintermediation.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.