AMD’s Q1 Earnings Preview - Undervalued Inflection

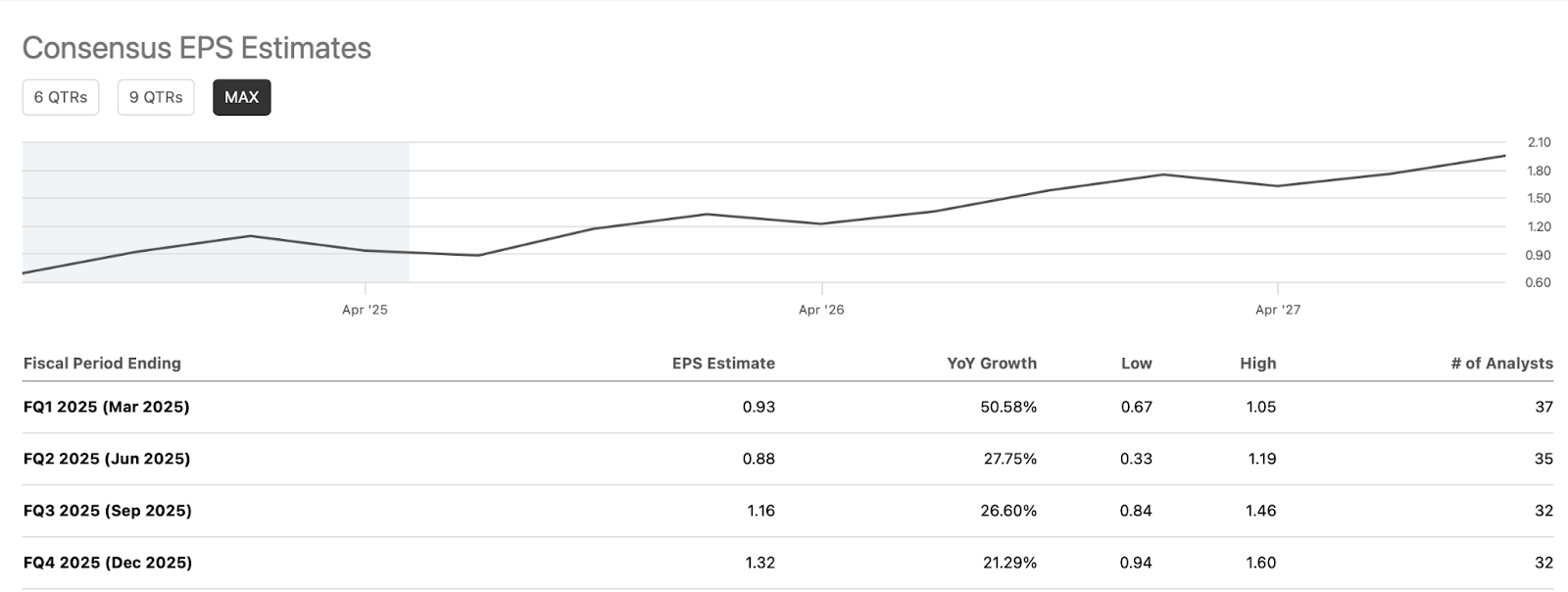

- AMD is set to report Q1 2025 results post-market on May 6, with expected EPS of $0.93 (+50.6% YoY) and revenue of $7.12B (+30.2% YoY). Despite flat sequential earnings, strong topline growth and margin signals from MI300X and EPYC could drive a valuation re-rating.

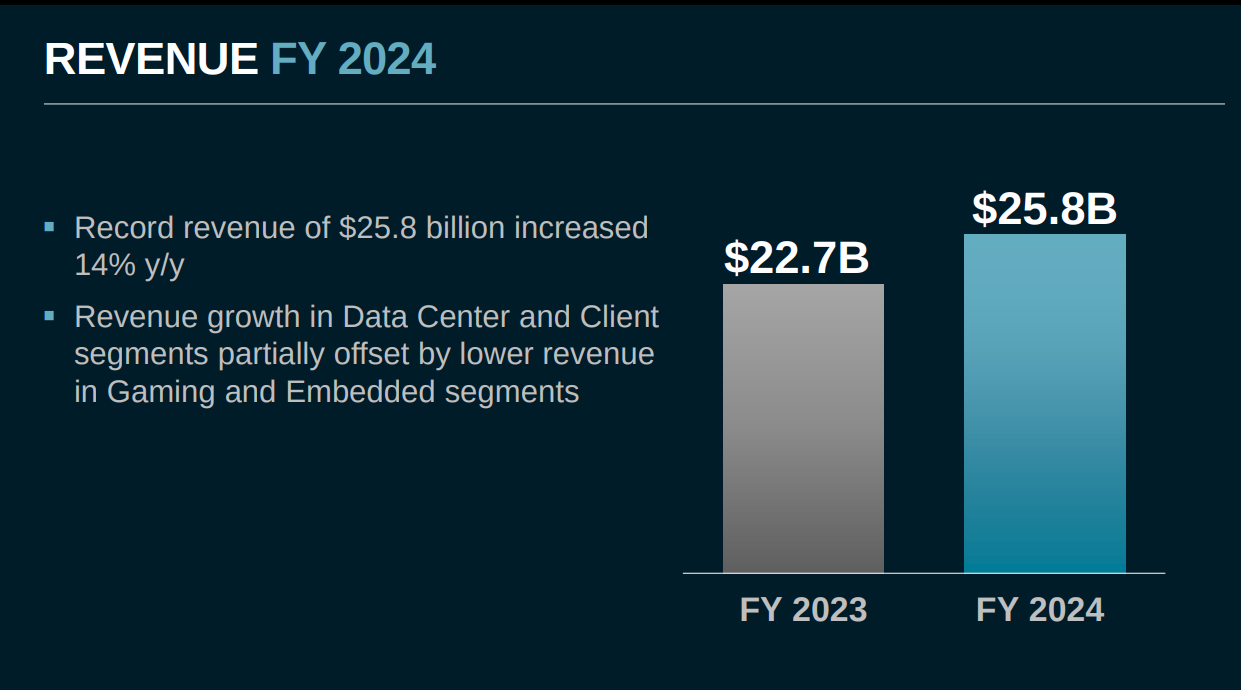

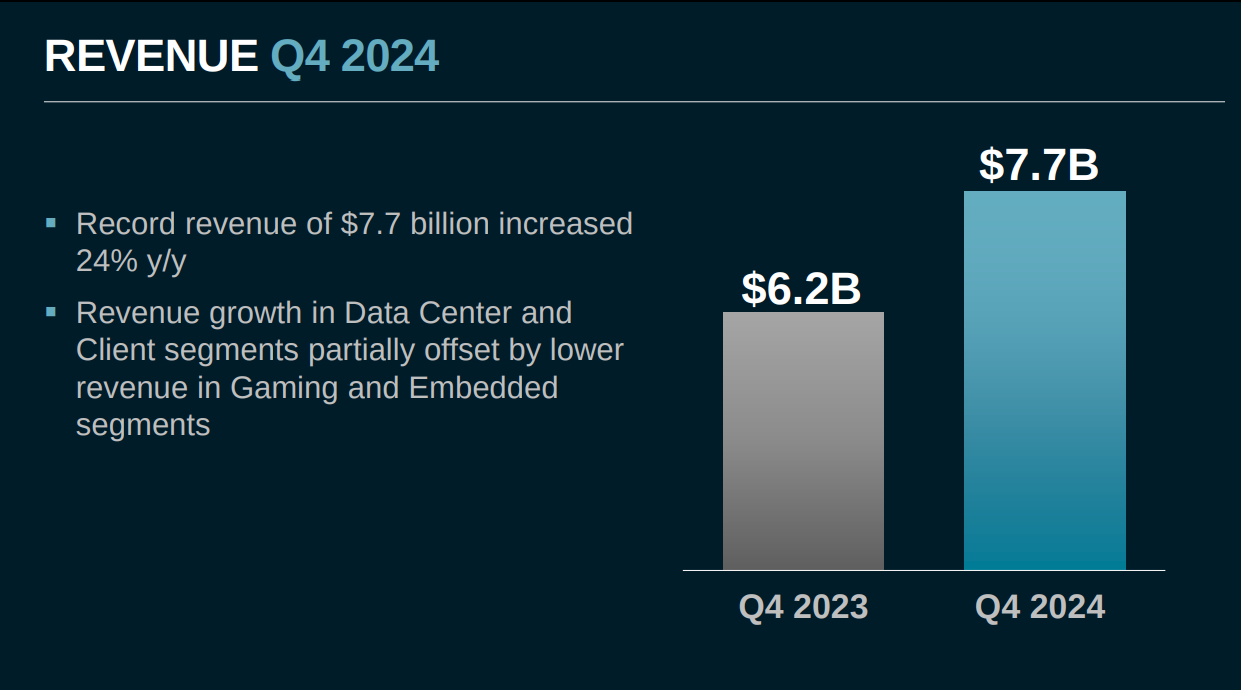

- AMD posted FY2024 revenue of $25.8 billion and non-GAAP EPS of $3.31, with Q4 revenue up 24% YoY to $7.7 billion, but long-term sustainability hinges on cost management and margin dynamics.

- The Data Center segment doubled to $12.6 billion, led by EPYC and Instinct AI chips, but Embedded and Gaming segments fell 33% and 58% YoY, undermining AMD’s overall margin consistency.

- Despite strong earnings, Q4 free cash flow declined 12% YoY to $831 million, highlighting AMD’s front-loaded AI investments and raising questions about near-term financial flexibility.

- Trading at ~47x non-GAAP earnings and ~11x price-to-sales, AMD’s stock reflects high expectations. Our DCF fair value is $150/share, about 15% below market, implying execution risk is underpriced.

AMD Q1 2025 Earnings Preview: The Valuation Gap May Finally Close

TradingKey - Advanced Micro Devices will release its Q1 2025 results after the close on May 6. Street consensus is $0.93 in normalized EPS, +50.6% YoY, on $7.12B in revenue, up 30.2% yoy. In spite of the mixed revisions in EPS (14 up vs. 15 down), the positive bias in revenue revisions (21 up to 5 down) augurs well for the topline momentum of AMD, driven by MI300X accelerator sales and EPYC data center CPU platforms.

In the last year, AMD has consistently hit revenue expectations in a 100% consensus-beating run and has surpassed EPS expectations in 88% of quarters. The stock continues to be fundamentally misunderstood. AMD only goes for 21.9x forward non-GAAP earnings and 0.78x PEG, far lower than high-growth comparables such as Nvidia despite the fact that the company has a 30%+ EPS CAGR that is expected through 2026. The market still perceives AMD through a chip-centric cyclical lens and pays no attention to the structural change occurring as the company transitions to a high-margin, platform-based AI computing contender.

The Q1 print marks a pivotal inflection point. Community expansion of the ROCm developer ecosystem, as well as AI PC commercialization and custom silicon R&D, should keep OpEx elevated sequentially vs. $1.09 in Q4, even as EPS holds steady. These expenses, successful as they might prove to be, establish the foundation for long-term monetization optionality far in excess of hardware unit sales. A beat-and-raise on gross margins, perhaps particularly in the case of MI300X adoption driving recurring inference or platform revenue, would indicate that the operating leverage that this implies will only continue to accelerate.

Source: Seeking Alpha

Key risks include: Gaming and Embedded segments are in a secular decline, including 66%+ of revenue derived from export-sensitive geographies. But in spite of this, Data Center expansion of +94% YoY in Q4, elevated client segment profitability and hyperscaler traction indicate that the underlying story is margin durability rather than cyclicality.

Assuming AMD leads strongly on margin expansion, ROCm activations and ongoing AI demand, its multiple will look conservative today. This quarter's results might prove to be the trigger for a much-needed re-rating.

Peeling Back the Layers: What AMD's Earnings Aren't Saying Loud

AMD’s FY2024 profit awed investors with $25.8 billion in revenue and a robust $3.31 non-GAAP EPS, but the mechanics underlying them are more complex. Even if Q4 revenue increased 24% year over year to $7.7 billion and non-GAAP margins remained steady at 51%, the extent to which that was sustainable will be determined by whether AMD can overcome intensifying cost pressures and segment divergence.

The Data Center segment was the undisputed star, more than doubling to $12.6 billion in revenue annually led by demand for EPYC CPUs and Instinct MI300 GPUs, with hyperscaler customers leading take-up. This hid a worrying slide elsewhere. The Embedded and Gaming segments reported precipitous revenue declines of 33% and 58% YoY, reducing their relative contributions to overall margin resilience. As lower-margin consumer units slowed, the mix turned to high-R&D AI units, squeezing operational leverage.

More illustrative was the decoupling between net income and free cash flow. As earnings-per-share rose on a non-GAAP basis, FCF dipped 12% YoY to $831 million in Q4, a signal that AMD is front-loading spend to lock down its AI roadmap, spending before revenue. That dynamic, although strategic, is risky if execution stalls. Further, historical patterns of guidance caution should be noted. Guidance tends to be aggressive during periods of expansion, albeit seen previously over the Zen 3 launch phase, and calls into question the realizability of 2025’s ambitious growth targets in a still-turbulent macro backdrop.

In essence, headline numbers were promising, but the internals suggest a firm balancing ambition with discipline on the balance sheet. Strength in revenue exists, but so do margin pressures, inventory accumulation, and fluctuations in the cash flows, all of which investors will want to monitor closely in the coming quarters.

Source: Q4 Deck

Beyond the Print: Key Strategies That May Reshape AMD's Future

While the majority of coverage focused on revenues, AMD was stealthily pursuing a more fundamental strategic realignment in 2024, one that has the potential to redefine its long-term position within the AI framework. Two front-page moves were notable: the purchase of Finland-based AI research front-runner Silo AI and the anticipated takeover of hyperscale server supplier ZT Systems. Both are, although under the spotlight to some, a purposeful shift to full-stack AI offerings and more stringent control of the ecosystem.

Silo AI is not a symbolic acquisition. It includes AI model training capability and software IP that directly complements AMD’s ROCm stack and Instinct GPUs. Silo’s software-native, AMD silicon-based trained LLMs provide a software-native advantage in a category that has been NVIDIA’s CUDA-centric stronghold. With AI software now becoming the new battlefield, this acquisition puts AMD in a position to level the developer adoption and optimization playing field, something that is necessary if it is to gain substantial training share within hyperscale.

ZT Systems, in turn, would be AMD’s path to vertical integration. As a substantial OEM supplier to cloud providers, ZT has the kind of infrastructure-level experience that would cut deployment cycles and help reduce AMD’s need to rely upon third-party integration firms. AMD has indicated that it intends to spin off the manufacturing portion of ZT’s business, meaning integration, by implication, and not fabrication. This also indicates a strategic desire to provide end-to-end solutions to hyperscalers, directly to compete with vertically integrated companies like Nvidia, that both make and sell chips and servers.

But execution is paramount. Integrations like this carry actual risk, and at scale. Silo and ZT both have to match AMD’s vision and pace culturally and operationally. Missteps in integration will be costly, both in reputation and market share. But the direction of the strategy is aggressive, and in an AI arms race, that's probably the only play that makes sense.

Source: Q4 Deck

Final Thoughts: Balancing Hype with Hard Metrics

AMD is at a turning point: full of momentum but under a cloud of complexity. Its AI story is unequivocally compelling. With surging Instinct GPU momentum, strategic purchases, and early wins with collaborators like Google Cloud, the firm is staking a real position in the AI infrastructure contest. But now, by extension, it’s not only a matter of hardware, it’s delivering solutions that scale, software that adheres, and value that compounds.

But this change is accompanied by tension. Such a quick shift in AMD’s business model, toward a vertically integrated AI platform from a CPU/GPU supplier, demands new muscles. The firm will have to deepen developer associations, strengthen its software stack, and maintain operational discipline alongside ballooning investments. That is no easy accomplishment.

For long-term investors, there is promise in the story. AMD’s product pipeline is full, its R&D is targeted, and its Lisa Su-led leadership is keen and visionary.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.