Pop Mart (9992 HK): How Long will the Sensation Last

Source: TradingView

Thesis

With its well-designed collection of Intellectual Properties (IPs) and collaboration with in-house and third-party designers, Pop Mart rides the consumer trends leading to this high level of growth. The company has plenty of opportunities in a more lucrative overseas market. Despite being up 180% in 2025, the stock is traded at 25x the 2027 forward earnings, which is reasonable if we compare it with more mature peers such as Sanrio (Hello Kitty) at 40x PE.

Company Overview

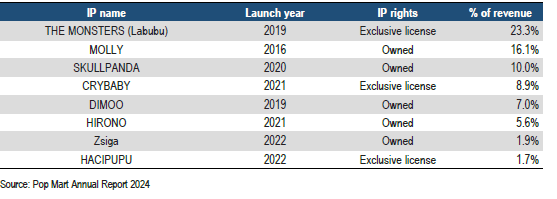

Pop Mart is a Chinese company that produces designer figures and toys. It has recently become a global phenomenon with one of its major IPs – Labubu. However, Pop Mart also has other popular product lines such as Molly, Skull Panda and Crybaby.

Source: JP Morgan

The core of Pop Mart is the sale of action figures in blind boxes, where the buyer does not know what figure is in the box - this brings an element of surprise and also sets the foundation for established resale market. Half of the revenue comes from action figures, while the other half is mainly from plush toys, accessories and MEGA (big size action figures).

Pop Mart mainly utilizes direct-to-consumer strategy with physical stores and an e-commerce website, and in order to keep the excitement and the interest high, they use gamified sales channels like Roboshop vending machines and lucky draw. As of 2024, there are 521 retail stores and 2,472 roboshops.

Source: JP Morgan

(popmart-revenue-breakdown)

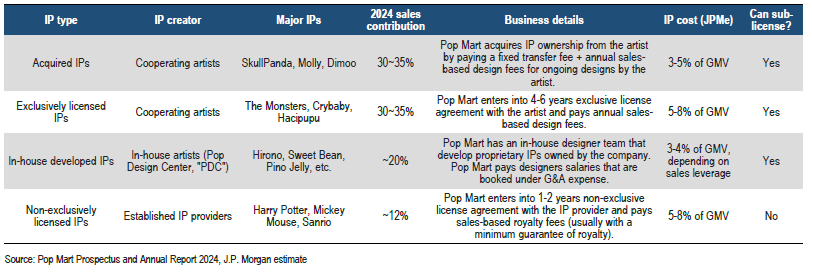

Relationship with Designers

Pop Mart has its own in-house design team, but they also collaborate with other designers. In fact, Monsters (Labubu) is designed by a Belgian-based Hong Kong designer Kasing Lung, and the collection is exclusively licensed to Pop Mart.

Source: 2024 Annual Report

Source: 2024 Annual Report

The Consumer Appeal

There are many reasons why Pop Mart IPs are so desirable:

Element of surprise: The blind boxes and the fact that buyers do not know what figures they are getting bring a feeling of scarcity and surprise, encouraging to purchase more and create a solid secondary market (think NFTs).

Celebrity endorsement: Lisa and Rose form Blackpink, as well as Rihanna were all spotted with Labubu toys, helping with the popularity of the characters across a very wide fan base.

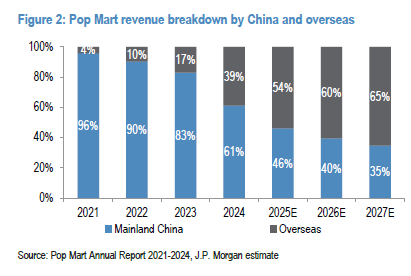

Adapting to local cultures: Pop Mart uses quite localized strategies in overseas market. We can see this in Thailand, which is already the second biggest market after China, and the fact that overseas revenue will be larger than Chinese revenue. All this with the help of understanding the sentiments within the targeted demography. For instance, in China, Crybaby resonates with the desire of young people to express vulnerability, which is not common for the older generations.

Riding a macrotrend: Unlike traditional toy companies like Hasbro or Mattel targeting children primarily, Pop Mart main customers are women in their twenties and thirties, living in urban areas. These women are more likely to work in white-collar jobs and not have children, hence they have extra disposable income to afford the more high-end-priced Pop Mart products. Also, the reason why Labubu plush toys are the fastest-growing SKU is because in the age of global uncertainty and women taking more responsibilities in the daily work life, they need an outlet of affection, making the cute and fluffy toys very suitable.

Global ambitions

Pop Mart is a typical Chinese homegrown brand, however due to its major success in Southeast Asia and breakthrough globally, the overseas revenue is growing at a much higher rate, and this year is expected to overtake the revenue generated in China.

In 2024, roughly 60% of the revenue came domestically, 30% came from the rest of Asia and 10% from other regions globally.

Source: 2024 Annual Report

.png)

Source: 2024 Annual Report

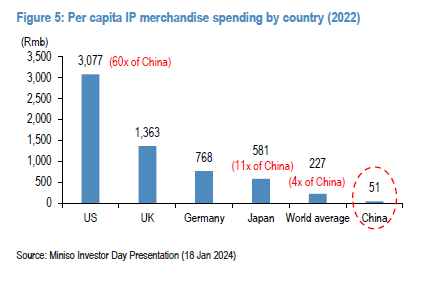

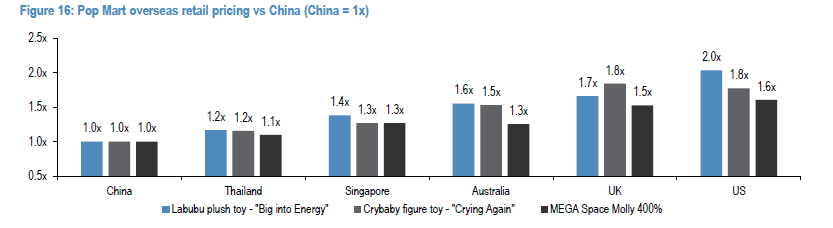

The overseas expansion will bring a number of benefits for the company. First, the average spending on IP is four times higher than in China, and for developed markets like US it can reach sixty times. This implies a huge total addressable market (TAM).

Second, the increase in overseas revenue as a percentage of total revenue will have a positive effect on the margins, as the company will be willing to price its products higher.

Source: Miniso Investor Day Presentation

Source: JP Morgan

Financials

Source: 2024 Annual Report

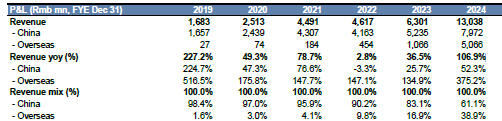

In 2024 we saw the total revenue almost doubled, mostly driven by overseas expansion. We do expect the domestic revenue to grow at around 20% CAGR in the coming years (5% will come from store expansion, and 15% will come from average sales per store).

The overseas growth will be even more explosive probably 40-50% year-over-year, in the coming three years, primarily driven by store expansion and the higher willingness of overseas customers to spend on IPs.

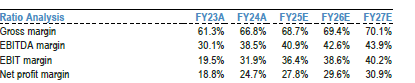

We expect margins to go up, as the company get further exposure to overseas markets – currently at around 66.8%, but can easily hit the 70% mark.

For reference, LEGO gross margin is at 68.3% and Lego is not even considered high-end, implying that Pop Mart margins can go beyond that.

Source: 2024 Annual Report

Little Exposure to Tariffs

Pop Mart has its production chains almost entirely in China but Currently, just 6% of the revenue comes from the US. The company has already raised the prices of its products there, however the demand far outweighs the supply, thus price increases will not affect the sales there.

Valuation

With 2.35 RMB earnings per share (2.57 HKD), the current trailing PE ratio of Pop Mart is around 100x. Considering the underlying growth ahead will push the EPS to almost 10.00 RMB, the 2027 forward looking PE will be around 25 times.

In order to get an idea of the valuation of an established IP company, we take a look at Sanrio. Sanrio is a Japanese company mostly famous for owning the IP of Hello Kitty. They also hold the rights for other famous characters like My Melody, Kuromi, Cinemonroll and Gudetama. In the past 10 years the company has been trading at around 40x PE on average, excluding the period during COVID.

We believe the 2027 valuation of Pop Mart should be close to that number, implying a target price of around 400 RMB or roughly 440 HKD (+70% upside).

Risks

Underwhelming performance of future IPs: Companies in the IP industry always have the problem of short lifecycles of their product series, thus they need to constantly innovate and launch new products. If a new product launch does not perform up to standard, this may hurt the company in the long run.

Change in preferences: Related to the risk above, consumer preferences are often quite unpredictable. Pop Mart successfully rode the viral wave with Labubu, but we simply cannot predict where the new viral trend will come from.

Cracking down on mystery boxes: The lack of transparency of what is inside the mystery boxes brings certain level of regulatory risk and we already saw this in China.

Risk of license renewal: Another major issue is the risk of not being able to renew some of the IP license agreements. As we saw above, Monsters (Labubu) is not an owned IP but an exclusively licensed one. Upon the expiry of the agreement between Pop Mart and the designer Kesin Lung, there is a chance of both parties not being able to reach an agreement on renewal, which might be a major hit for the revenue of the firm.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.