Buffett’s Billion-Yen Bet: Why Global Capital Is Flowing Into Japan

TradingKey - Since April, the Nikkei 225 has surged from 32,000 to nearly 38,000 points—a 15% gain that sharply outpaces the S&P 500’s performance over the same period. Beyond the uptick in local investor engagement, global funds have also renewed their interest in Japan’s markets.

At Berkshire Hathaway’s 2025 annual shareholder meeting, Warren Buffett reaffirmed his long-term bullish view on Japan, citing his sustained investments in the country’s five major trading houses. This endorsement has reignited global investor interest in Japanese equities.

Macro View: Policy Tailwinds Meet External Drivers

Japan has emerged as a key beneficiary of the U.S.-led restructuring of global supply chains. As a historic manufacturing powerhouse, Japan’s strengths in high value-added sectors—semiconductors, precision instruments, and advanced machinery—combined with a politically stable and business-friendly environment, have made it a prime destination for supply chain rebalancing.

In the semiconductor equipment segment, for example, Japan’s exports to China surged 84.7% year-on-year in 2024. Tokyo Electron now derives 46.9% of its total revenue from China—an all-time high—solidifying Japan’s strategic position in global tech supply networks.

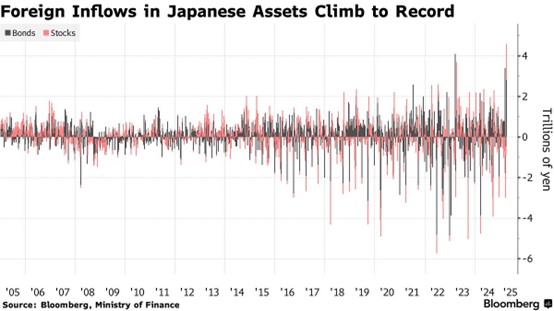

As market volatility reshapes global asset maps, Japan is looking more and more like a sheltered port for global funds. According to Japan’s Ministry of Finance, foreign inflows into domestic equities turned positive in the week ending April 4 for the first time since January, with net purchases totaling ¥1.81 trillion. Including bond purchases, total net inflows reached ¥2.8 trillion—an all-time record.

Source: Bloomberg

The Bank of Japan maintaining ultra-loose monetary policy has further supported equity markets. The country’s benchmark interest rate remains below 0.50%, among the lowest globally, keeping corporate financing costs at low level. This has helped sustain capital expenditures and boost corporate earnings.

Japanese stocks remain undervalued compared to global peers. as of Q2 2024, the average price-to-earnings (P/E) ratio for companies listed on the Tokyo Stock Exchange Prime Market was approximately 16.2x—well below the S&P 500’s 26.8x over the same period. This valuation gap offers investors potential upside for a re-rating and makes Japanese equities more appealing as capital searches for undervalued markets.

Source: World PE Ratio

Meanwhile, Japan’s corporate governance reforms have been gaining real traction in recent years. Updates to the Corporate Governance Code are pushing more companies to focus on shareholder returns, with rising dividends and more share buybacks. For example, Mitsubishi has raised dividends for 10 straight years, and Sojitz plans a 49% increase by FY2025. These actions are boosting ROE and supporting a structural re-rating of Japanese equities.

Sector-Level Strength: Japan’s Industrial and Strategic Assets

Japan plays a vital role in the global automotive industry. In auto parts, Denso holds a 23% share of the global automotive semiconductor market, while Mitsubishi Electric leads in high-end vehicle sensors with a 31% share. It also remains a major player in complete vehicle manufacturing. Toyota sold 10.45 million units in the fiscal year ending March 2025, accounting for 18.3% of global vehicle sales. Moreover, Japan is a global front-runner in hydrogen vehicle technology, with the long-term potential to outperform both China and the U.S.

In artificial intelligence-related technologies, Japan boasts deep expertise, particularly in industrial robotics and optical components. Companies like Fanuc and Canon hold over 50% share in their respective global segments. Tokyo Electron’s Q1 FY2025 earnings showed a 21% YoY revenue increase in semiconductor etching equipment, giving it a 38% share in logic chip tools. Its advanced <5nm etching technology underscores Japan’s strategic depth in key verticals.

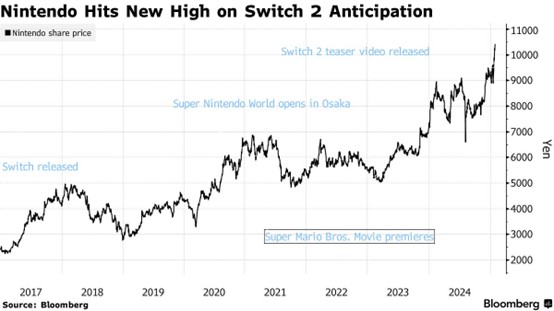

Cultural influence remains a key element in the evolution of Japan’s gaming and media industries. Nintendo stands as a leading force in global gaming. The 2025 global launch of the Switch 2 console (integrating VR capabilities and backward compatibility) is expected to drive significant upgrade demand from a 150-million-user install base. Goldman Sachs forecasts this release to push user engagement to new highs, assigning a 12-month target price of ¥13,600—a potential upside of 14%.

Source: Bloomberg

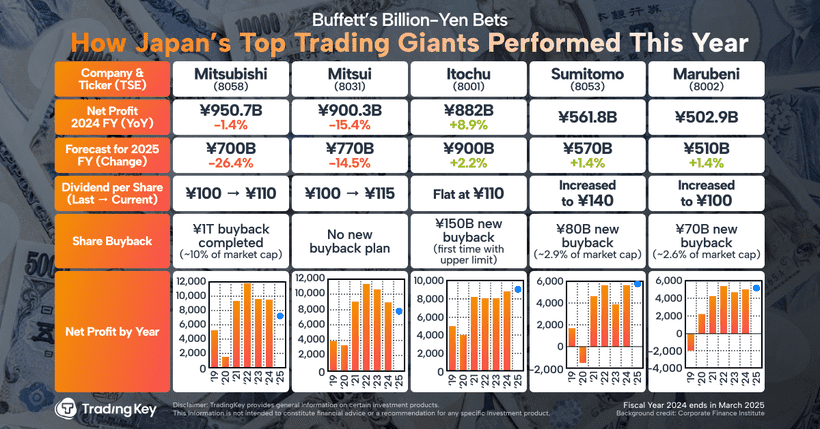

Buffett’s favored five trading giants—Itochu, Marubeni, Mitsubishi Corp, Mitsui & Co., and Sojitz—operate across a wide range of sectors including energy, metals, machinery, chemicals, and food, forming a vertically integrated industrial ecosystem. Meanwhile, in 2024, the average dividend yield among the five exceeded 5%, compared to the S&P 500’s 1.5%. Their collective share buybacks reached ¥2.2 trillion for the year, offering investors a compelling “high dividend + aggressive buyback” profile ideal for income-seeking portfolios.

The Other Side of the Story: Risks to Watch

First, Japan’s auto export machine could stall under the weight of new U.S. tariffs. With upstream and downstream linkages across steel, logistics, and electronics, the sector employs more than 5.58 million people—roughly 10% of Japan’s workforce. Trade frictions risk disrupting this critical ecosystem.

Second, a structural weakening of the U.S. dollar or anticipation of Federal Reserve rate cuts may exert upward pressure on the yen. That could harm Japanese exporters, especially trading houses, as more than 70% of their revenue comes from abroad. Currency volatility poses a serious threat to profitability.

Notably, Japan’s long-standing demographic challenge—an aging population—continues to limit the growth potential of domestic demand, posing a structural constraint on medium- to long-term economic expansion.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.