U.S. April Nonfarm Payroll Preview: Any Short-Term Stock Market Dip Is a Buying Opportunity

Tradingkey - The April Nonfarm Payroll (NFP) report, due on 2 May 2025, is expected to show a slowdown in job growth, which may temporarily pressure U.S. equities. However, a weaker labour market could prompt the Federal Reserve to resume its rate-cutting cycle, providing a tailwind for stocks. For investors with a 1-3 month horizon, any near-term market pullback presents a compelling buying opportunity.

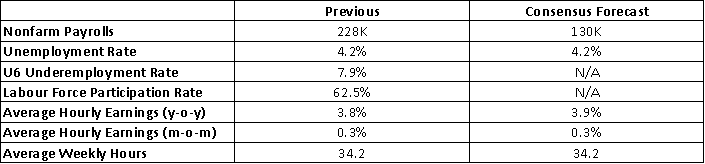

On 2 May 2025, the U.S. Bureau of Labor Statistics will release the April NFP report. Market consensus anticipates nonfarm job additions of approximately 130,000, a significant decline from March’s robust 228,000 (Figure 1). We align with this consensus forecast.

Figure 1: Consensus Forecasts

Source: Refinitiv, Tradingkey.com

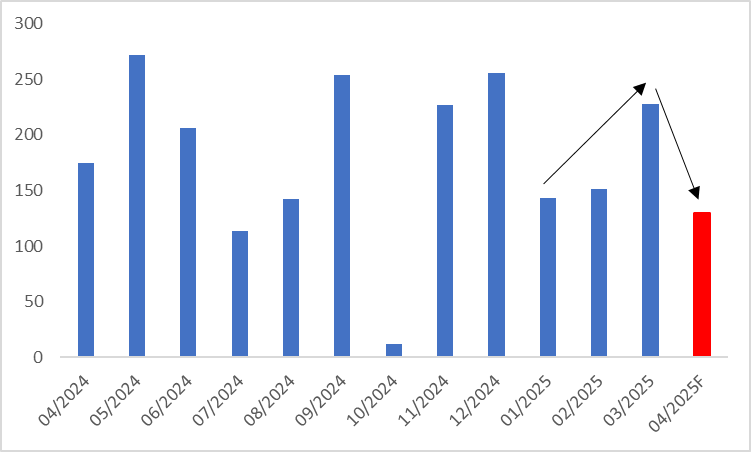

March’s strong employment growth (Figure 2) was driven by three key factors: (1) the dissipation of adverse weather effects from January and February, (2) the resolution of strikes in the healthcare and retail sectors, and (3) the delayed impact of government layoffs, which were not yet fully reflected in the data.

Figure 2: Nonfarm Payrolls (000)

Source: Refinitiv, Tradingkey.com

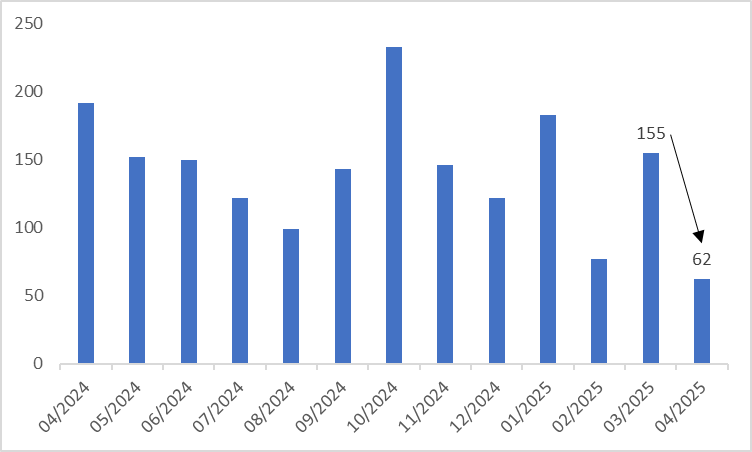

Looking ahead, the emerging effects of President Trump’s tariff policies reduce the likelihood of sustained job growth in April. Supporting this view, the ADP Employment Change report—often considered a “mini-NFP”—dropped sharply from 155,000 in March to 62,000 in April (Figure 3), signalling potential weakness in the official NFP data.

Figure 3: ADP Employment Change (000)

Source: Refinitiv, Tradingkey.com

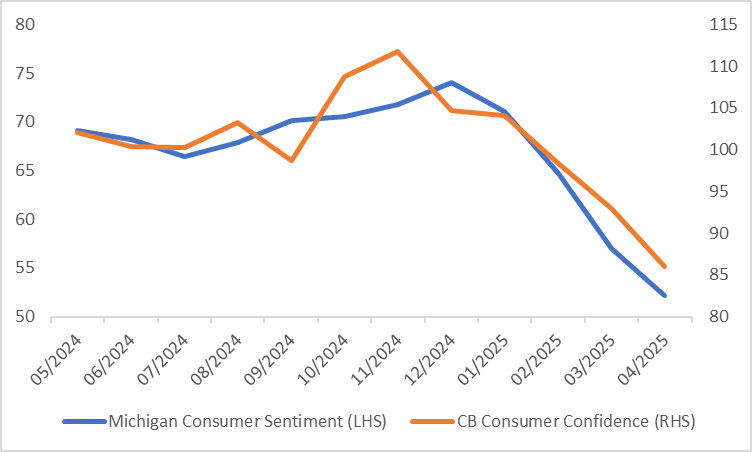

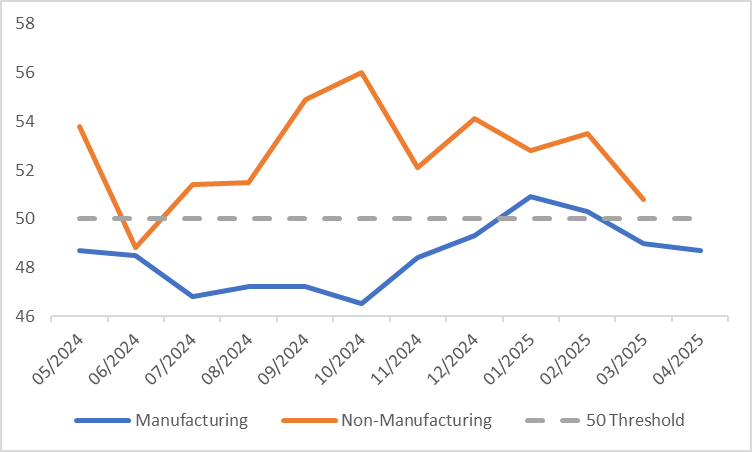

The U.S. real GDP growth for Q1 2025 was negative, underscoring economic challenges. Recent high-frequency economic indicators provide further insight into April’s labour market outlook. On the demand side, the April Consumer Confidence Index fell significantly (Figure 4). On the production side, the ISM Manufacturing PMI remained below the 50-expansion threshold for March and April, while the ISM Non-Manufacturing PMI, though still above 50, declined notably from 53.5 in February to a lower level in March (Figure 5). These weakening economic signals are likely to weigh on the labour market from both demand and supply perspectives.

Figure 4: Consumer Confidence Index

Source: Refinitiv, Tradingkey.com

Figure 5: ISM PMI

Source: Refinitiv, Tradingkey.com

Should the April NFP data undershoot market expectations, U.S. equities are likely to experience a short-term sell-off following the release. However, a softening labour market, coupled with slowing economic growth and inflation trending toward the Fed’s 2% target, will likely give the Federal Reserve both the incentive and the flexibility to restart its rate-cutting cycle. Lower interest rates would inject additional liquidity into financial markets, creating a favourable environment for equities.

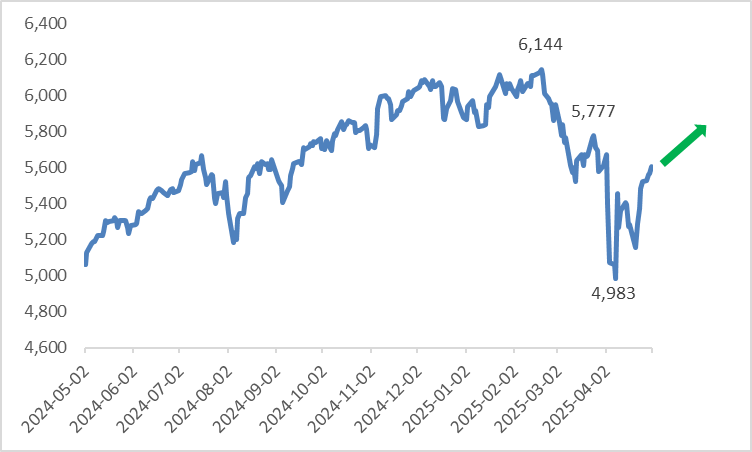

Consequently, for investors with a 1-3 month outlook, any near-term decline in U.S. stocks triggered by a weak NFP report should be viewed as a strategic buying opportunity (Figure 6).

Figure 6: S&P 500 Index

Source: Refinitiv, Tradingkey.com

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.