DOJ vs. Fed: Why the Stock Market is Applauding the "End of Independence"

AI Podcast

The DOJ's investigation into Fed renovations, while triggering concerns about central bank independence and reminiscent of the Arthur Burns era, may signal a shift toward a "known evil" of controlled inflation. This contrasts with the "unknown evil" of U.S. solvency risk due to its $38 trillion debt and high interest payments. The market's positive reaction suggests a preference for a dovish Fed that can devalue debt and redirect funds to future investments, rather than face potential collapse from unmanageable interest obligations. This represents a move from a "risk-free" paradigm to one prioritizing government solvency.

The News

On Friday, January 9th, the United States Department of Justice did something that would have been unthinkable just two years ago. They served Jerome Powell, the Chair of the Federal Reserve, with grand jury subpoenas. The official reason? A criminal investigation into a $2.5 billion office renovation at the Fed's Eccles Building.

Powell didn’t stay quiet. On Sunday night, he released a video statement that felt more like a declaration of war. He called the investigation a 'pretext'—a smoke screen designed to intimidate the central bank into lowering interest rates.

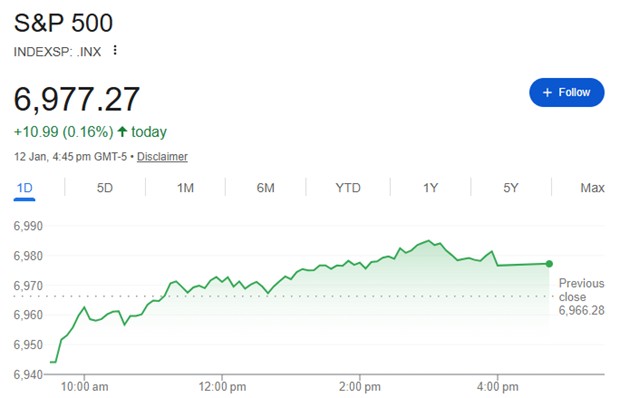

The mainstream media is in total panic. They’re calling this the end of American credibility. They’re saying the Fed has fallen, and the 'Banana Republic' era has begun. But if you look at the markets the following day, something strange happened. The S&P 500 didn't crash. They started weak but finished at +0.16%.

Today, we’re moving beyond the headlines to the math that the media is too afraid to touch.

Why is everyone so bearish? Because the standard economic playbook says that Central Bank independence is the 'Holy Grail.' If the President can bully the Fed, the logic goes, then investors lose trust, the currency becomes worthless, inflation goes infinite, and invested money flees.

Historic Similarities

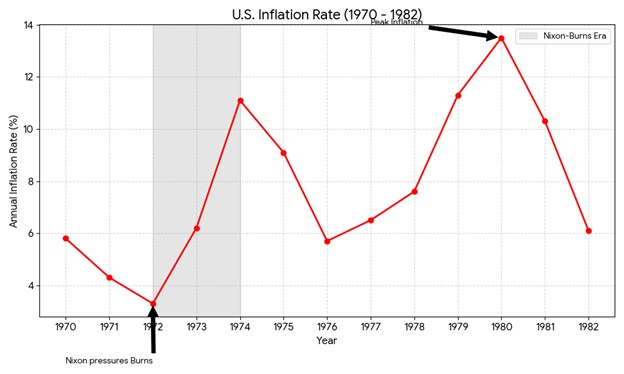

You’ve heard one name over and over again: Arthur Burns. He was the Fed Chair in 1972, and he is the reason every 'independent' central banker has nightmares.

Back then, President Richard Nixon was facing a re-election campaign. He didn't care about the long-term health of the dollar; all he wanted was a landslide election victory. He famously pressured Arthur Burns, telling him to keep the interest rates low so the economy would feel upbeat and keep the voters satisfied.

Despite his resistance at first, Burns folded, and Nixon got his win. But the cost was a decade of elevated inflation that almost destroyed the American middle class.

Source: US Census

And look, if you only read the headlines, that’s exactly what it looks like. We have subpoenas, DOJ pressure, and a Fed Chair trying to stay independent.

But here’s the contrarian truth: The market isn't closing in the green because it’s 'ignoring' the drama. It’s closing in the green because it wants the Fed to lose. We are witnessing a fundamental shift in the American financial architecture.

Known vs Unknown Evil

The administration has made a calculated choice. They are choosing the “Known Evil” by forcing the Fed to be more dovish, leading to a higher inflation—over the “Unknown Evil” which is higher interest rates leading to higher interest payments.

Think about it. If the Fed is 'captured' and forced to lower rates, yes, we get inflation. Your groceries get more expensive, the market may get corrected, and your dollar loses value. It sounds bad, but we know how to handle that. We've lived through it before; we saw this in the 1970s, and we also saw it in 2022. Did we survive? Obviously.... and that’s why this is the “known evil”.

Source: US Census

But the 'Unknown Evil'? That would be a world where the U.S. government can’t pay its interest, or where the public spending goes to repaying debt instead of healthcare, infrastructure and defense. That might be a Pandora's box that can trigger the collapse of the entire global financial system.

And in terms of debt, the situation in 1972 has quite a stark difference from what we are seeing now – less than half a trillion of national debt in 1972 versus 38 trillion now. Also, back then, the debt-to-GDP ratio was just 34% compared to 124% now.

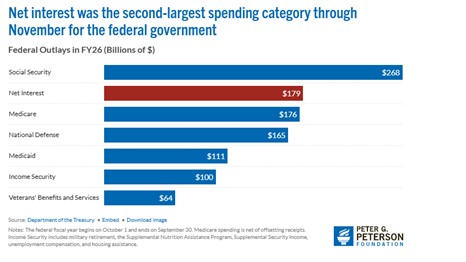

This gigantic debt obligates the government to pay high interest payments, and as we see from the November data from the Peter G. Peterson Foundation, this is already the second largest source of spending of the government, just behind social security, but larger than higher than healthcare and defense.

Source: Petar G. Peterson Foundation

Currently, interest payments represent around 20% of the US fiscal revenue, or simply speaking, for every 5 dollars the government collects from taxes, 1 dollar will go for repayment of debt. And according to the World Bank in 2022, the average ratio globally was 5%, or 4 times smaller than in the US.

So, what does a debt-strained U.S. actually look like? We don’t know. Because we have never reached a point where the Treasury cannot cover its interest payments, this is the true 'Unknown Evil'. What we do know is that a debt crunch triggers a total collapse of confidence. When 20% of every tax dollar goes to servicing past debt rather than serving the citizens and the economy. For investors, this shift from 'Risk-Free' to 'Solvency-Risk' would trigger a mass abandonment of U.S. assets as they flee a system that can no longer afford its own future. This is way worse than inflation.

When you see the DOJ going after Powell over 'renovations,' don't get distracted by the marble floors. They are removing the man who represents 'Higher for Longer' because 'Higher for Longer' will literally break the United States.

By forcing the Fed under the dominance of the white house, keeping rates low, the government can 'melt' the real value of that $38 trillion debt, by replacing previously high-interest debt with a newer low-interest debt, and that also means suppressing the soaring interest payments.

The Effect on US Stocks

Now, here is the most contrarian part. Why would the U.S. stocks benefit from this?

Because the alternative is worse. In a world of global chaos, investors don't look for 'perfect'—they look for 'liquid' and 'solvent.' If the U.S. government guarantees its own solvency by capturing the Fed, it becomes a safe port in the storm.

Monday’s green closing proves it. While the mainstream was crying about 'lost independence,' the big money was realizing that a Fed that 'folds' is a Fed that provides a permanent floor for asset prices.

For the tech-heavy S&P 500 and Nasdaq, this is a massive win. Lower rates don't just protect valuations; they allow the government to stop wasting tax dollars on 'dead' interest payments and start pouring that capital into the Chips Act, AI initiatives, and national infrastructure. We are moving from a regime of 'paying for the past' to 'investing in the future’.

The battle for the Fed isn't over. Between now and May, the DOJ pressure will ramp up. You will see more headlines about building renovations, 'lost' emails, and ethics violations. Don’t fall for the noise.

The 'independence' of the central bank was a luxury of the 20th century, when debt was low, and the world was stable. In 2026, with $38 trillion on the line, that luxury is gone, and interest payments eating out 20% of the fiscal revenue, Trump cannot afford such luxury.

The market has already made its choice, and it seems like it chose the ‘Known Evil.'

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.