Is Plug Power (PLUG) Stock a Buy Now?

Key Points

Plug stock has dipped almost 60% from its 52-week high.

The company has grown revenue at an impressive clip over the past decade, but profits have remained elusive.

Unlike Plug, Bloom Energy has generated consistent revenue.

Tumbling more than 16% over the past month, Plug Power (NASDAQ: PLUG) stock has fallen out of favor over the past few weeks. With the recent plunge, shares of the fuel cell and hydrogen specialist are now down about 59% from their 52-week high as of this writing.

But smart investors know that simply because the market has taken a bearish stance on a stock doesn't mean it's unworthy of being added to their portfolios. With this in mind, let's take a closer look at the bull and bear arguments.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Getty Images.

Bulls believe...

The recent drop in Plug stock belies the fact that many investors recognize it as a great growth opportunity, a route to gain exposure to the burgeoning hydrogen industry.

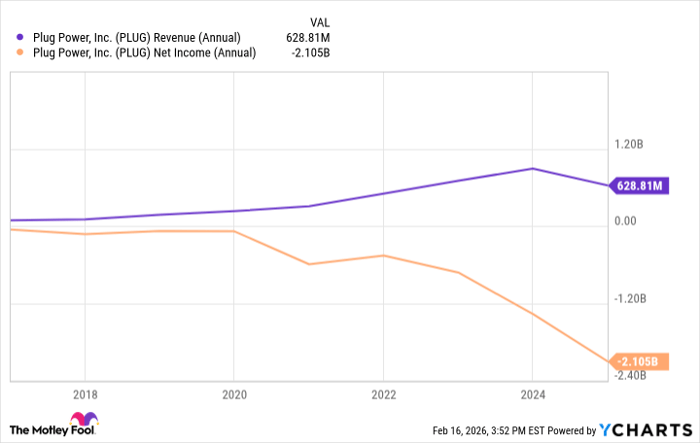

For several years, the company has demonstrated success at attracting customers and growing revenue. From 2014 through 2024, for example, Plug has grown its top line by about 880%.

This sales growth is complemented by the company's progress toward profitability. In March 2025, Plug Power announced a cost-savings initiative dubbed Project Quantum Leap. Already, the company is recognizing benefits from the program's implementation. For the nine-month period ending Sept. 30, 2025, Plug reported a gross profit margin of negative 51.1%, an improvement from the negative 89.3% it reported during the same period in 2024.

Optimistic about further progress toward profitability in the coming years, management laid out a timeline during an October investor presentation that included a target of achieving breakeven on a gross profit basis by the end of 2025, and achieving positive earnings before interest, taxes, depreciation, amortization, and share-based expense (EBITDAS) by the end of 2026. Ultimately, management foresees Plug achieving overall profitability by the end of 2028.

With Plug shares trading at 2.9 times trailing sales, a discount to their five-year average price-to-sales ratio of 3.9, bulls are positive that now's a great time to pick up Plug stock.

But bears contend...

Sure, revenue growth is great, but bears aren't impressed. Those pessimistic about Plug's prospects focus on the company's bottom line rather than the top of the income statement. While Plug's advocates contend that the company is a growth stock, skeptics refute that claim, pointing out that the company, founded in 1997, has been around for nearly three decades. The company's persistent lack of profitability, therefore, isn't as understandable as it is with upstart companies that are making material progress toward generating profits.

PLUG Revenue (Annual) data by YCharts.

And while management has provided an auspicious timeline that projects the company breaking even on gross profit, EBITDAS, and net income bases over the next three years, those who have followed Plug for several years know that management has a long history of underdelivering on expectations.

Plug's profitability problems are even more glaring when juxtaposed with Bloom Energy's (NYSE: BE) success. Like Plug, Bloom Energy is one of the leading hydrogen stocks available to investors, but unlike Plug, Bloom has demonstrated the ability to consistently generate profits. Earlier this month, Bloom Energy reported fourth-quarter 2025 financial results, which included diluted earnings per share (EPS) of $0.45. Bloom has reported adjusted diluted EPS of $0.76 and $0.28 for 2025 and 2024, respectively.

Whether it's an investment in a hydrogen stock, such as Bloom Energy, or in a hydrogen exchange-traded fund, Plug bears recognize a variety of options to gain hydrogen industry exposure.

Forget the bulls' beliefs -- watch Plug from the sidelines

While Plug deserves credit for growing sales over the past few years and for implementing its cost-reduction initiative, Project Quantum Leap, it seems a little hasty to deem the stock a buy right now. For most investors, the best approach is to see if the company continues achieving success in reducing expenses and driving closer toward profitability, or if it falters as it has done so many times in the past.

Should you buy stock in Plug Power right now?

Before you buy stock in Plug Power, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Plug Power wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $415,256!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,151,865!*

Now, it’s worth noting Stock Advisor’s total average return is 892% — a market-crushing outperformance compared to 194% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of February 21, 2026.

Scott Levine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bloom Energy. The Motley Fool has a disclosure policy.

Related Articles

Nikkei Index Heading Toward 60,000? Why Is Global Capital Betting on Sanae Takaichi? Will Japan’s Stock Market Continue to Hit New Highs in 2026?

TradingKey - In February 2026, the Tokyo stock market once again became the epicenter of global financial markets. Following a landslide victory by the Sanae Takaichi-led Liberal Democratic Party in the Lower House elections, the Nikkei 225 Index hit consecutive record highs within just a few days, targeting the 60,000-point milestone.

Will Micron Be the 2026 AI Winner as the Memory Supercycle Begins?

Recently, Micron has focused on premium areas such as High-Bandwidth Memory that plays alongside accelerators to feed AI models, and adding capacity with an eye on pricing discipline.

NFT Price Collapse 2026: Full Market Analysis and Digital Asset Recovery Forecast

Analyze the 2026 NFT price collapse and the pivot to digital utility. From Bored Ape floor stability to Solana NFT news and NFT credit cards, explore the recovery forecast.