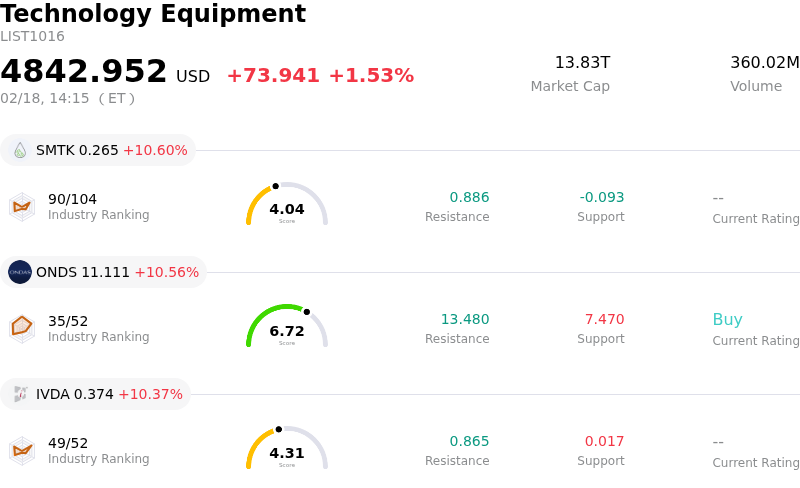

Micron Technology Inc Stock Moved Up by 5.80% on Feb 18: Facts Behind the Movement

Micron Technology Inc (MU) moved up by 5.80%. The Technology Equipment industry is up by 1.53%. The company outperformed the industry. Top 3 gainers of the industry: SmartKem Inc (SMTK) up 10.60%; Ondas Holdings Inc (ONDS) up 10.56%; Iveda Solutions Inc (IVDA) up 10.37%.

Micron Technology (MU) experienced significant upward movement, driven primarily by positive developments in the high-bandwidth memory (HBM) market and strong analyst sentiment. The company announced that it has officially entered volume production for its next-generation HBM4, a full quarter ahead of its previous guidance, solidifying its position in the rapidly expanding artificial intelligence (AI) infrastructure market. Furthermore, Micron confirmed that its entire HBM capacity for the 2026 calendar year is already 100% sold out, indicating robust demand and strong forward visibility for this high-margin product.

This positive news around HBM production and sales aligns with broader industry trends indicating a worsening shortage of DRAM and NAND flash memory, driven by surging demand from high-margin AI server segments. Prices for memory are expected to continue rising, with supply constraints potentially persisting even if costs peak in the first half of 2026. Several market researchers and analysts forecast memory shortages to persist well into 2027, with server-centric DRAM demand directly tied to competitiveness and not easily reduced. This environment of tight supply and increasing prices is highly favorable for memory manufacturers like Micron.

Analyst forecasts have also been overwhelmingly positive, with a consensus "Buy" rating from 28 analysts as of February 18, 2026. Multiple analysts have recently raised their price targets and earnings estimates for Micron, citing the tightening memory market and significantly higher pricing. For example, a top analyst recently increased fiscal year 2026 and 2027 revenue and adjusted EPS estimates, assuming substantial quarter-over-quarter increases in blended DRAM and NAND average selling prices. These upward revisions reflect confidence in Micron's ability to capitalize on the sustained demand for memory, particularly from the AI sector. The company's strategic decision to exit the consumer PC memory market in late 2025 and refocus on AI demand for memory further supports the bullish outlook, as AI customers typically bring higher margins.

Technically, Micron Technology Inc (MU) shows a MACD (12,26,9) value of [23.01], indicating a neutral signal. The RSI at 55.80 suggests neutral condition and the Williams %R at -60.83 suggests oversold condition. Please monitor closely.

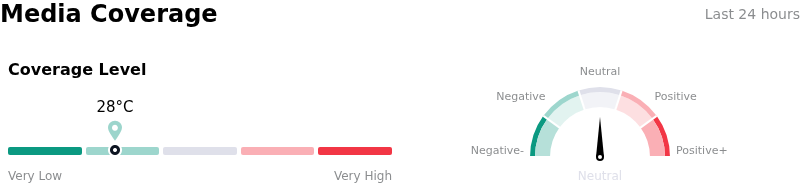

In terms of media coverage, Micron Technology Inc (MU) shows a coverage score of 27.68, indicating a low level of media attention, with neutral sentiment.

Micron Technology Inc (MU) is in the Technology Equipment industry. Its latest annual revenue is 37.38B, ranking 6 in the industry. The net profit is 8.54B, ranking 5 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as BUY, with an average price target of 366.65, a high of 523.00, and a low of 86.28.

Company Specific Risks:

- Analyst consensus price targets, including the average and several low-end estimates, suggest a significant potential downside from Micron's current stock valuation.

- The highly cyclical nature of the memory industry exposes Micron to rapid market fluctuations and the risk of future oversupply and price corrections, despite current strong demand and reported AI memory shortages.

- Micron's operations are capital-intensive, necessitating substantial ongoing investments in manufacturing and technology, which can strain financial resources and impact profitability during periods of market contraction.

- Intense competition from key rivals such as Samsung and SK Hynix in critical advanced memory markets, including High-Bandwidth Memory (HBM), poses a continuous threat of pricing pressure and potential market share erosion.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.