Is Wall Street Wrong About Amazon Stock?

Key Points

Amazon's stock is down amid Wall Street fears of a large capital-spending cycle in 2026.

This happened to the business before in the COVID-19 pandemic and led to long-term earnings and cash-flow growth.

The stock looks cheap for investors who have a multiyear time horizon.

Investors know Amazon (NASDAQ: AMZN) as one of the best-performing stocks of the 21st century. However, the trillion-dollar technology giant has actually severely underperformed the stock market indexes in recent years. Amazon stock is up just 22% cumulatively in the last five years, while the S&P 500 index has produced a total return level of 87%.

After its fourth-quarter earnings report earlier this month, Wall Street has soured on the e-commerce and cloud computing giant once again. Why? Because of its ambitious capital spending plans, which could have the business burning free cash flow in 2026.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Here's why investors may be wrong about Amazon stock, and why it is a buy today.

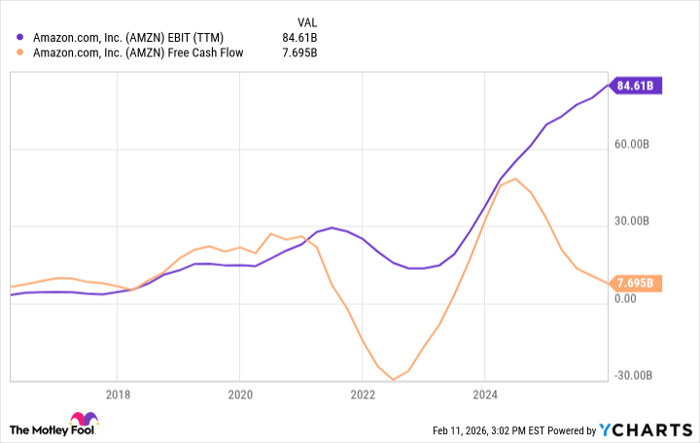

Data by YCharts.

Capital expenditures and the long-term vision

Amazon Web Services (AWS), the company's cloud infrastructure division, is seeing resurgent demand because of the insatiable spending needs of artificial intelligence (AI) start-ups. Companies like Anthropic, with fast-growing revenue, spend billions of dollars with AWS each year, and plan to spend more in the future.

Last quarter, AWS revenue grew 24% year over year to $35.6 billion, with expectations for further revenue acceleration in 2026. To build enough data centers to meet customer demand, Amazon needs to spend aggressively up front, which is why it plans to spend $200 billion on capital expenditures this year, up from $132 billion last year and $83 billion the year before.

Investors are scared because this exceeds Amazon's 2025 operating cash flow of $140 billion, likely leading to negative free cash flow in 2026. However, I believe this should be seen as bullish for the company, as it suggests Amazon sees a massive runway to reinvest and expand its revenue base. This happened during the COVID-19 pandemic, when the company needed to invest in additional cloud and delivery infrastructure to support its e-commerce business, temporarily leading to negative free cash flow.

Then, in a few years, Amazon was back to generating record free cash flow. The same should be expected a few years from now.

Image source: Getty Images.

Amazon is a cheap stock for patient investors

Right now, Amazon's free cash flow is moving in the wrong direction due to heavy upfront investments in data center infrastructure. At the same time, operating earnings keep growing, hitting a record high of $85 billion over the last 12 months.

This is due to rising AWS revenue and margin expansion in its retail operations. Both trends should continue in 2026 due to the AI infrastructure build-out and the rapid growth of Amazon's high-margin businesses, such as advertising. Consolidated operating margin was 11.8% in 2025. I expect this figure to eventually reach 15% or even higher over the next decade.

Once these accelerated AI investments are finished, free cash flow should begin to converge back with operating earnings. If Amazon can grow its consolidated revenue by 15% a year over the next three years (it grew 14% last quarter, with accelerating AWS growth), the business will be doing over $1 trillion in revenue by the end of the decade.

A 15% profit margin on $1 trillion in revenue is $150 billion in bottom-line earnings, or around double today's levels. Follow this trend, don't worry about a short-term hit to free cash flow, and watch Amazon stock crush it for your portfolio over the next five years.

Should you buy stock in Amazon right now?

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $414,554!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,120,663!*

Now, it’s worth noting Stock Advisor’s total average return is 884% — a market-crushing outperformance compared to 193% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of February 15, 2026.

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon. The Motley Fool has a disclosure policy.

Related Articles

This Is Why I’m Buying Taiwan Semiconductor Stock in 2026

TradingKey - Taiwan Semiconductor Manufacturing (TSM) is part of a rapidly growing sector in AI.

January CPI Revives Rate-Cut Hopes; Gold and Silver Rebound, But Is the Bull Run Intact?

TradingKey - During Friday's US session, spot gold surged back above $5,000 to close at $5,043, while silver resumed its rally, breaking through the $75 mark to peak near $79 before closing at $77.43. This movement was primarily driven by data from the U.S. Bureau of Labor Statistics that significan

Bitcoin Price Prediction 2029-2035: Institutional Accumulation and the U.S. Treasury’s Strategic Reserve Pivot

Explore the 2026 Bitcoin landscape: From the U.S. Strategic Reserve and Michael Saylor’s $75B war chest to Cathie Wood’s 2030 forecast. Is BTC the new Digital Gold?

This $1 Trillion AI Stock Is Getting Ready for 2026: Is Meta a Good Buy?

When ads and commerce are factored in, Meta is building a long-term platform—in Augmented Reality and smart glasses — to get us closer to the future of AI. This device hardware business is less profitable than ads right now, but it could grow the company’s ecosystem and open up new ways for it to ma

Is SaaS Dead? The Truth Behind the Software Meltdown, the Missing Floor, and the Peak That’s Not Coming Back

TradingKey - A trillion dollars just vanished from software stocks—this piece breaks down who AI is really killing, who quietly benefits, and why cheap SaaS may be the biggest value trap of this cycle.