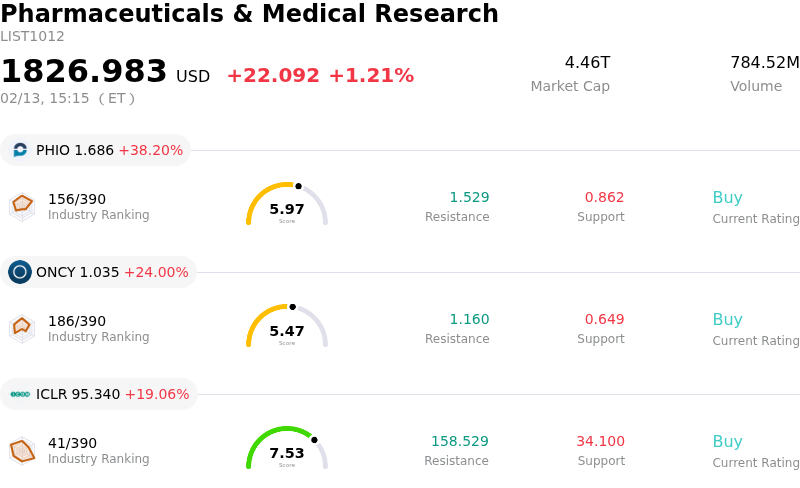

Vertex Pharmaceuticals Inc Stock Moved Up by 6.51% on Feb 13: What Signal Does It Send?

Vertex Pharmaceuticals Inc (VRTX) moved up by 6.51%. The Pharmaceuticals & Medical Research industry is up by 1.21%. The company outperformed the industry. Top 3 gainers of the industry: Phio Pharmaceuticals Corp (PHIO) up 38.20%; Oncolytics Biotech Inc (ONCY) up 24.00%; ICON PLC (ICLR) up 19.06%.

Vertex Pharmaceuticals (VRTX) experienced a significant upward movement on February 13, 2026, driven primarily by positive analyst sentiment and encouraging financial results, despite a slight miss on quarterly earnings per share. Several analyst firms issued positive reports, with Oppenheimer upgrading the stock to "Outperform" with a $540 price target, citing optimism around the company's renal pipeline candidates povetacicept and inaxaplin. Cantor Fitzgerald also raised its price target to $590 while maintaining an "Overweight" rating, highlighting confidence in Vertex's renal franchise to potentially rival its cystic fibrosis (CF) business. Scotiabank maintained its "Sector Perform" rating but increased its price target to $558. These analyst adjustments reflect an average target price of $540.73, indicating a potential upside from current levels.

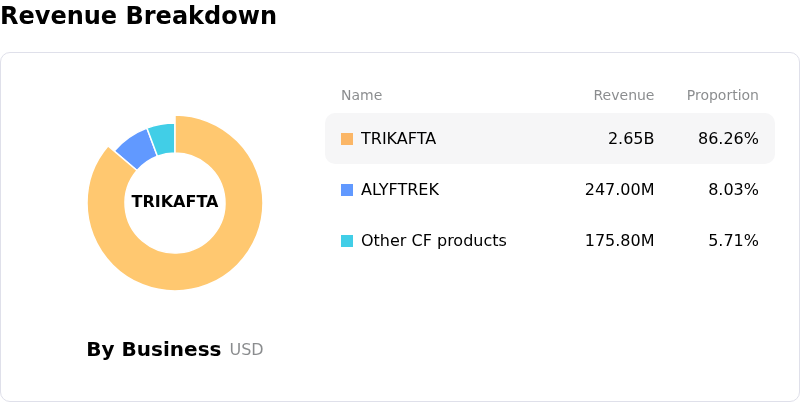

The company reported its fourth-quarter 2025 earnings, revealing revenue of $3.19 billion, which surpassed analyst expectations of $3.17 billion or $3.18 billion and represented a 9.5% to 10% year-over-year increase. This revenue growth was largely fueled by strong sales of its cystic fibrosis drugs, particularly Trikafta/Kaftrio, and contributions from newer drugs like Alyftrek, Journavx, and Casgevy. While adjusted earnings per share (EPS) of $5.03 slightly missed consensus estimates of $5.05 to $5.08, the revenue beat and positive outlook appear to have overshadowed the minor EPS shortfall.

Furthermore, Vertex provided an optimistic outlook for 2026, forecasting total revenue between $12.95 billion and $13.10 billion, representing 8% to 9% growth. A key component of this guidance is an anticipated non-CF product revenue exceeding $500 million, signaling momentum in newer therapeutic areas like Casgevy and Journavx. The company is actively diversifying its portfolio beyond CF, with strategic plans for five product launches in five distinct disease areas within a five-year timeframe, including advancements in its renal franchise with povetacicept. Vertex is also progressing with its mid- and late-stage clinical pipeline, which is expected to deliver transformative medicines and enhance long-term value. These strategic developments and positive revenue projections contributed to the favorable investor response.Vertex Pharmaceuticals (VRTX) experienced a significant upward movement on February 13, 2026, largely influenced by positive analyst ratings and robust revenue performance. Several analyst firms issued encouraging reports, with Oppenheimer upgrading the stock to "Outperform" and setting a price target of $540, citing optimism regarding the company's renal pipeline candidates such as povetacicept and inaxaplin. Cantor Fitzgerald also raised its price target to $590, maintaining an "Overweight" rating and highlighting confidence in Vertex's renal franchise to potentially match its successful cystic fibrosis business. Scotiabank similarly increased its price target to $558 while maintaining its "Sector Perform" rating. These analyst adjustments collectively point to an average target price of $540.73, suggesting potential for further appreciation.

The company recently reported its fourth-quarter 2025 earnings, which showed total revenue reaching $3.19 billion, exceeding analyst consensus estimates and marking a 9.5% to 10% year-over-year increase. This strong revenue growth was primarily driven by continued robust sales of its cystic fibrosis (CF) drugs, including Trikafta/Kaftrio, and growing contributions from newly launched therapies such as Alyftrek, Journavx, and Casgevy. Although the adjusted earnings per share of $5.03 marginally missed analyst forecasts, the positive revenue surprise and forward-looking guidance appeared to mitigate the impact of this slight earnings shortfall.

Furthermore, Vertex provided an optimistic outlook for 2026, projecting total revenue to be in the range of $12.95 billion to $13.10 billion, signifying an 8% to 9% growth. A significant part of this forecast includes an expected revenue contribution of over $500 million from its non-CF products, indicating successful diversification efforts beyond its core CF franchise. The company reiterated its strategic goal of achieving five product launches across five different disease areas within a five-year timeframe, emphasizing advancements in its renal franchise with povetacicept and progress in its broader mid- and late-stage clinical pipeline. These strategic initiatives and promising growth prospects appear to have positively influenced investor sentiment, contributing to the stock's upward movement.

Technically, Vertex Pharmaceuticals Inc (VRTX) shows a MACD (12,26,9) value of [3.89], indicating a neutral signal. The RSI at 50.77 suggests neutral condition and the Williams %R at -65.29 suggests oversold condition. Please monitor closely.

Vertex Pharmaceuticals Inc (VRTX) is in the Pharmaceuticals & Medical Research industry. Its latest annual revenue is 12.00B, ranking 20 in the industry. The net profit is 3.95B, ranking 15 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as BUY, with an average price target of 525.59, a high of 625.00, and a low of 330.00.

Company Specific Risks:

- Vertex Pharmaceuticals missed Q4 2025 earnings per share estimates, reporting $5.03 per share against an expectation of $5.07 per share, indicating potential operational underperformance.

- New product launches, including Journavx and Casgevy, show "underwhelming growth" and "remain niche," casting doubt on their ability to drive future growth already factored into the company's valuation, making its ~26x 2025 EPS vulnerable.

- The expansion into new disease areas through collaborations, such as the WuXi Biologics alliance for autoimmune diseases, introduces high clinical setback and delay risks for preclinical programs, potentially increasing R&D spending and adding execution complexity that could weigh on future margins.

- Concerns exist regarding potential safety signals in other pipeline candidates like suzetrigine, povetacicept, and inaxaplin, which could challenge the company's competitive standing.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.