Should You Buy the Dip in CoreWeave Stock?

Key Points

CoreWeave offers AI developers access to GPUs through cloud-based infrastructure.

It is not yet consistently profitable, and much of its backlog stems from a small cohort of customers.

The company's valuation has normalized over the last few months, but the stock remains somewhat pricey.

One of the most anticipated artificial intelligence (AI) initial public offerings of the last year was CoreWeave (NASDAQ: CRWV). While investors initially cheered on the data center services provider following its March 2025 debut, shares have been under immense selling pressure over the last several months.

A combination of AI bubble fears, the high amount of debt on the company's balance sheet, and potentially a misunderstanding of CoreWeave's value proposition drove the shares downward by as much as 52% since the beginning of November. While the stock has rebounded somewhat from its recent low, shares are still trending downward since late January. Let's dig into some of CoreWeave's advantages and assess if now is a good opportunity for smart investors to buy the dip.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

The neocloud advantage: How CoreWeave is disrupting hyperscalers

Over the last three years, hyperscalers such as Amazon Web Services, Microsoft Azure, and Google Cloud Platform have shelled out hundreds of billions of dollars in capital expenditures to procure high-powered AI chips and servers, and to construct massive data centers to house this hardware. One of the biggest catalysts behind big tech's rising infrastructure spending is its need to provide AI processing power to its customers.

While the AI trend has undoubtedly ushered in a new growth arc for cloud service providers, accelerated capex levels and lengthy data center buildouts have been making Wall Street uneasy as of late. In some ways, these dynamics can benefit CoreWeave.

CoreWeave is a neocloud company: Essentially, its business model is to procure GPUs from Nvidia and rent access to this hardware via a cloud-based platform. The value proposition of this approach is that it provides a fast, cost-efficient way for developers to access best-in-class AI ecosystems without the expenses of designing, building, and operating their own data centers.

Image source: Getty Images.

How Nvidia and OpenAI de-risk CoreWeave

Nvidia is more than just a chip supplier to CoreWeave. The GPU designer is actually a major investor in the neocloud company, and recently doubled its stake in it, buying an additional $2 billion worth of its shares.

As of the end of the third quarter, CoreWeave boasted a backlog of $55.6 billion -- up 271% year over year. According to management, commitments from OpenAI represent up to 40% of that total. Meanwhile, Meta Platforms inked a multiyear, $14 billion deal of its own with CoreWeave a few months ago.

In my view, CoreWeave's ability to attract top-tier hyperscalers as customers while maintaining a strategic relationship with the king of AI chips, Nvidia, makes the company's investment profile significantly less risky compared to smaller peers like Nebius Group or Iren.

Is CoreWeave stock undervalued?

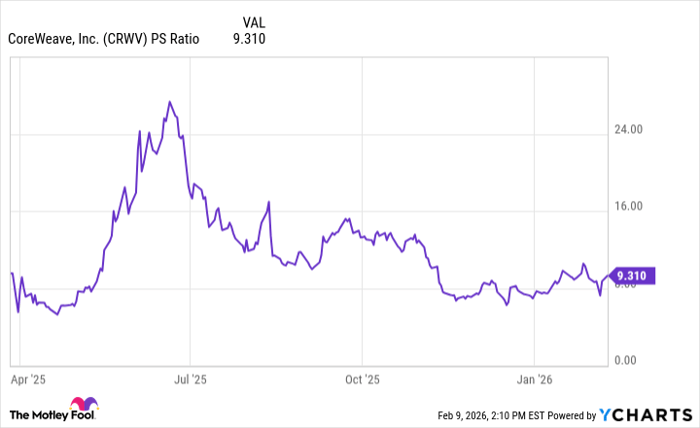

The perceived drawback for CoreWeave as an investment is its valuation relative to its financial profile. It is not yet consistently profitable, and it carries nearly $19 billion worth of debt and operating leases on its balance sheet.

CRWV PS Ratio data by YCharts.

Against this backdrop, a price-to-sales (P/S) ratio of 9 is far from a cheap valuation for an unprofitable, capital-intensive business with a high customer concentration.

Nevertheless, I think CoreWeave could still be a savvy buy right now for the right investors. Shares have normalized considerably over the last several months. Moreover, the AI infrastructure supercycle is only just beginning. CoreWeave looks well positioned to ride some strong secular tailwinds over the next several years.

Investors looking to complement their existing AI positions with emerging opportunities may want to consider CoreWeave stock at its current levels and prepare to hold on for the long run.

Should you buy stock in CoreWeave right now?

Before you buy stock in CoreWeave, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and CoreWeave wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $443,353!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,155,789!*

Now, it’s worth noting Stock Advisor’s total average return is 920% — a market-crushing outperformance compared to 196% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of February 12, 2026.

Adam Spatacco has positions in Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has a disclosure policy.

Related Articles

This $1 Trillion AI Stock Is Getting Ready for 2026: Is Meta a Good Buy?

When ads and commerce are factored in, Meta is building a long-term platform—in Augmented Reality and smart glasses — to get us closer to the future of AI. This device hardware business is less profitable than ads right now, but it could grow the company’s ecosystem and open up new ways for it to ma

Is SaaS Dead? The Truth Behind the Software Meltdown, the Missing Floor, and the Peak That’s Not Coming Back

TradingKey - A trillion dollars just vanished from software stocks—this piece breaks down who AI is really killing, who quietly benefits, and why cheap SaaS may be the biggest value trap of this cycle.

Best AI Tools for Stock Analysis in 2026 to Boost Your Investment Portfolio

As Artificial Intelligence (AI) continues to enhance everyday decision-making, these tools will allow us to leverage artificial intelligence to analyse stocks and optimise our investment portfolio.

Silver Faces Sixth Consecutive Year of Supply Deficit, How Much Upside Is Left in 2026?

TradingKey - According to the 2026 Silver Market Outlook recently released by the Silver Institute, the current robust performance of the silver market remains supported by solid fundamentals. The report indicates that the global silver market is expected to face a structural supply-demand imbalance