HK Close | HSI Edges Higher On Solid Turnover; Tech And Consumer Electronics Lead Gains

I. Market Overview

Hong Kong equities ended modestly higher, led by strength in technology and consumer electronics. The Hang Seng Index (HSI) closed at 26,585.06, up 0.37%; the Hang Seng China Enterprises Index (HSCEI) finished at 9,122.95, up 0.31%; and the Hang Seng Tech Index (HSTECH) outperformed at 5,746.30, up 1.11%. Turnover remained active, with total market turnover at HK$250.45 billion, signaling constructive participation despite mixed global cues.

Gains were concentrated in semiconductors, hardware and selected platform names, while a few large-cap internet stocks lagged. Sentiment was also buoyed by company-specific catalysts, most notably a sharp rally in Skyworth on restructuring plans.

II. Sector Performance

Large-cap Tech Stocks

Large-cap tech outperformed: the HSTECH rose 1.11% as semis led—Hua Hong Semi +5.17% to HK$105.80, SMIC +3.69% to HK$77.25—while platforms were mixed: Alibaba +2.19% to HK$163.20, Tencent +0.25% to HK$602.50, Meituan -0.05% to HK$97.30, and NetEase -3.70% to HK$208.00.

Top Performing Sectors

• Home Improvement Retail +18.52%

• Consumer Electronics +17.97%

• Distributors +7.68%

Bottom Performing Sectors

• Forest Products -5.19%

• Other Diversified Financial Services -3.97%

• Office Services & Supplies -3.70%

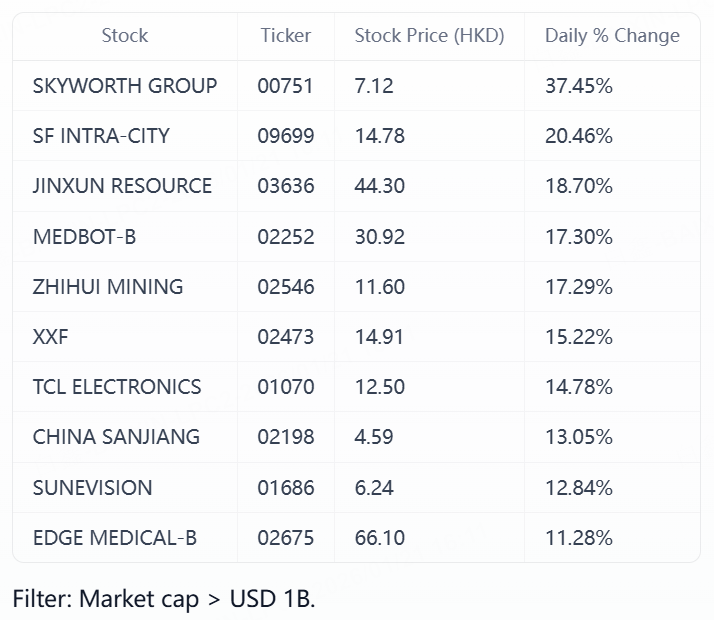

III. Top 10 Gainers in Hong Kong Market Today

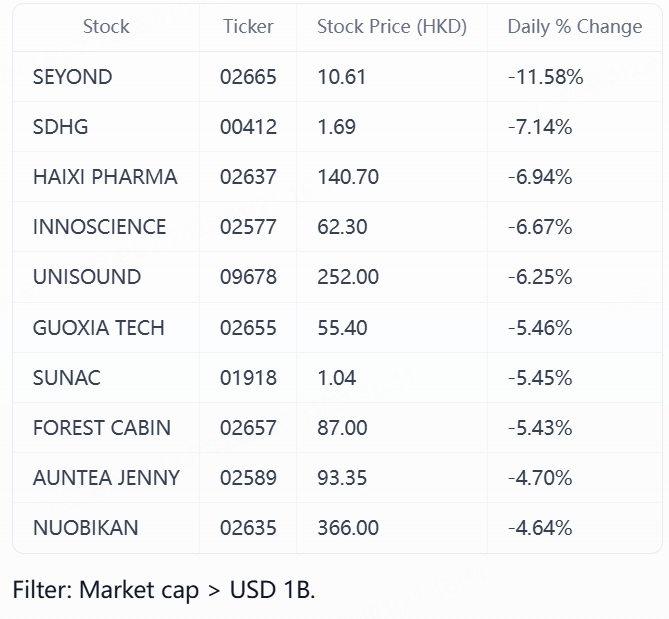

IV. Top 10 Losers in Hong Kong Market Today

V. Closing Summary

The Hong Kong market advanced for the session with broad—but measured—gains across major benchmarks. The HSI (+0.37%) and HSCEI (+0.31%) posted modest rises, while the HSTECH (+1.11%) outpaced as investors rotated into semiconductors and select platforms. Turnover at HK$250.45 billion suggests ongoing engagement despite external volatility. Market breadth favored cyclical tech-linked areas and consumer hardware, with defensive pockets of weakness in some financial and services segments.

Large-cap tech was mixed but net positive. Semiconductors led: Hua Hong Semi (+5.17%) and SMIC (+3.69%) benefited from improving sentiment toward chip manufacturing and supply-chain visibility. Platform and internet names were uneven: Alibaba (+2.19%) and Kuaishou (+3.62%) rose, while Tencent (+0.25%) ticked higher and NetEase (-3.70%) slipped. Hardware-linked names like BYD Electronic (+2.45%) and Sunny Optical (+2.16%) added support.

Outside tech, company-specific catalysts drove notable moves. Skyworth Group (+37.45%) surged after announcing plans to spin off its photovoltaic business and pursue a go-private transaction—an MT Newswires report highlighted the restructuring as a pathway to unlock value and fund growth in solar. Robotics-related names saw interest intraday (Tiger Newspress flagged strength in Medbot and peers), consistent with gains in Health Care Equipment and related tech segments. Nonferrous metals and gold-linked counters also attracted bids amid a supportive commodity tape noted by local media.

Sector-wise, leadership skewed toward consumer hardware and distribution, with top performers including Home Improvement Retail (+18.52%), Consumer Electronics (+17.97%), and Distributors (+7.68%). Laggards were concentrated in Forest Products (-5.19%), Other Diversified Financial Services (-3.97%), and Office Services & Supplies (-3.70%). Property headlines were mixed: Reuters reported creditor support for Vanke’s bond repayment plan, easing near-term default fears; however, the broader real estate complex remained subdued in sector data, indicating investors are still cautious pending more comprehensive balance-sheet progress.

Sources: Public market data, summarized media reports

Disclaimer: This content is for reference only and does not constitute investment advice.

Related Articles

Can Oracle Make a Strong Comeback in 2026 After Previous Struggles?

TradingKey - The focus of retail investors should be on companies with long-term revenue prospects and strong cost management. Oracle (ORCL) appears to be a good example.

The Hotter AI Gets, the More Attractive “Bricks” Become? Wall Street's HALO Craze Turns Heavy Assets Red-Hot

TradingKey - As AI technology continues to lower the barriers to replication for virtual products, global asset pricing logic is undergoing a subtle shift—tangible assets rooted in the physical world that are difficult to replace digitally are regaining significant favor from capital. This trend has

Ethereum Fails to Hit $2,200. Will ETH Hit New Lows Again in 2026?

Ethereum retreats after testing $2,200: Will it continue to drop and hit new lows?

Nvidia Q4 Earnings Beat Expectations but Stock Plunges 5.5%, $260 Billion in Market Value Erased Overnight, Why Are Investors Voting With Their Feet?

TradingKey - On February 25, 2026, global AI chip leader Nvidia (NVDA) released its fiscal 2026 fourth-quarter earnings report. Revenue, net profit, and data center business all significantly exceeded Wall Street consensus expectations, delivering a "stellar" set of results.

Deconstructing Citrini’s “2028 Global Intelligence Crisis”: S&P 8000 Bait and the Game Logic of Technological Deflation

A deep deconstruction of the 2026 AI-driven wealth migration logic, analyzing the paradox between the unemployment wave warnings and the S&P 8,000 projection in the Citrini report. Through core case studies such as Microsoft’s valuation mean reversion and Amazon AWS’s computing power dividends, this article reveals high-conviction investment opportunities in "physical layer" assets against a backdrop of technological deflation.