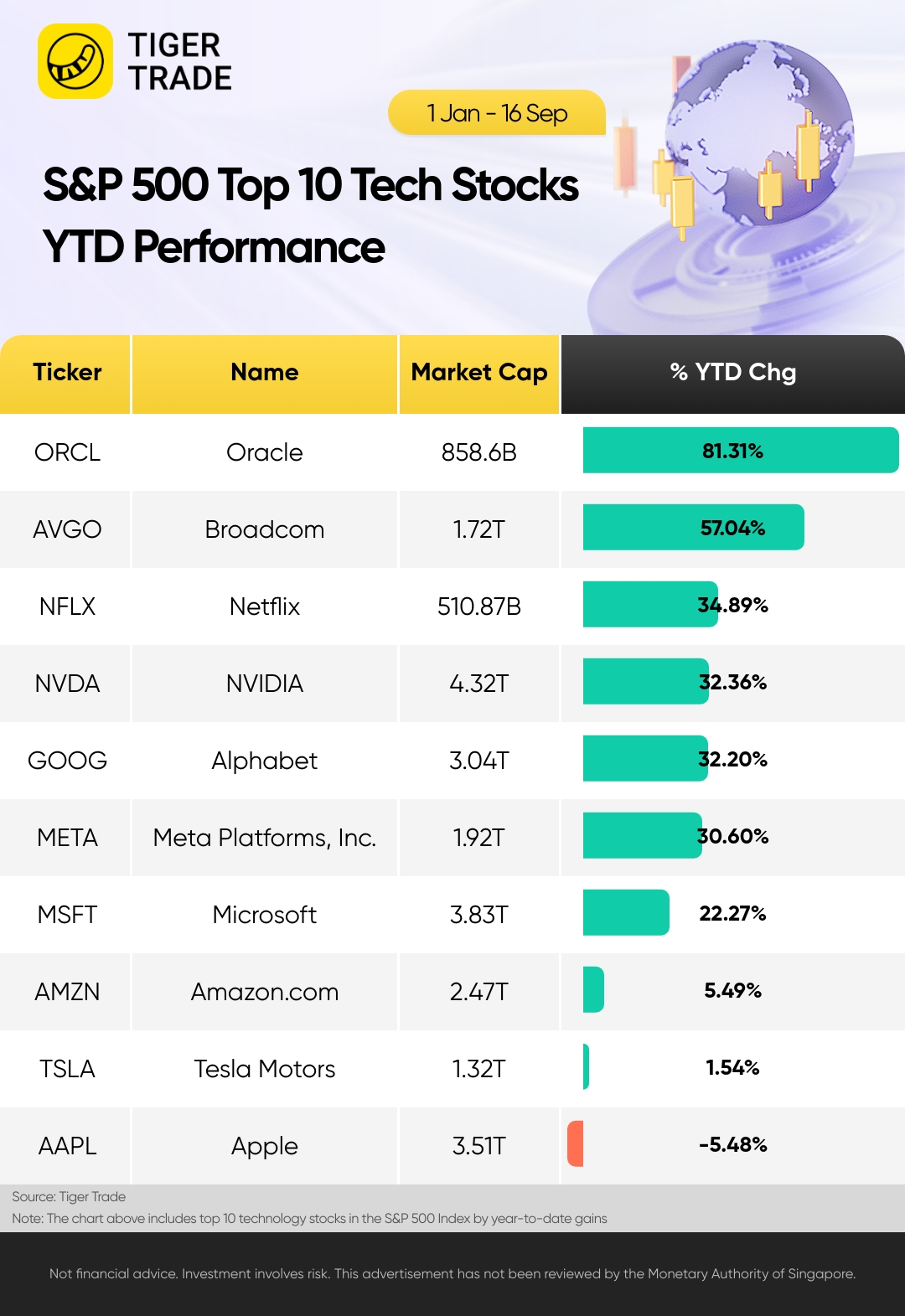

S&P 500 Top 10 Tech Stocks YTD Performance: Oracle Up 81%; Broadcom Up 57%; Netflix, Nvidia, Alphabet And Meta Up 30%

The S&P 500 closed above 6,600 for the first time on Monday. It has gained 12% this year. Among the S&P 500 constituent tech stocks, Oracle performed best, soaring 81% YTD; Broadcom up 57%; Netflix up 35%.

Competition among the “Magnificent Seven” names is heating up, Alphabet and Nvidia gained 32%, being the best-performing “Magnificent Seven” name on a year-to-date basis. Meta up 30%; Microsoft up 20%. But Amazon, Tesla and Apple underperformed the S&P 500 this year.

Oracle

Oracle’s was a reinvention of a quarter that, according to many on Wall Street, “changed the whole story.” The company’s fiscal first quarter of 2026 announces $14.9 billion in revenue, up 12% year-over-year, and non-GAAP EPS growth of 6% to $1.47. That alone would be solid, but it’s the underlying surge in future demand that has everyone talking.

“We signed four multi-billion-dollar contracts with three different customers in Q1,” said Oracle CEO, Safra Catz. “This resulted in the RPO contract backlog increasing 359% to $455 billion. It was an astonishing quarter and demand for Oracle Cloud Infrastructure continues to build. Over the next few months, we expect to sign-up several additional multi-billion-dollar customers and RPO is likely to exceed half-a-trillion dollars.

Oracle stunned the market by revealing that its remaining performance obligations (RPO), a measure of contracted work waiting to be delivered soared by 359% to a massive $455 billion at the end of August. This jump came on the back of four multi-billion-dollar AI contracts, a validation that Oracle’s pivot to cloud infrastructure and AI services is bearing fruit. Investors, sensing an inflection point, propelled the stock up by a staggering 36% in a single day.

Alongside larger cloud providers such as Microsoft, Oracle has been one of the big winners of the artificial intelligence boom, due to its cloud infrastructure business and its access to Nvidia’s graphics processing units, or GPUs, needed for large workloads.

Broadcom

Broadcom's most recent quarter underscored how central AI has become to results. In the third quarter of fiscal 2025 (the quarter ended Aug. 3), revenue rose 22% year over year to about $16 billion, adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) margin was 67%, and non-GAAP earnings per share was $1.69. Management also guided for fourth-quarter revenue of about $17.4 billion and said AI semiconductor revenue should climb to roughly $6.2 billion in the fourth quarter after growing 63% to $5.2 billion in the third. Free cash flow hit $7.0 billion, or 44% of revenue.

Summing the last four reported quarters puts Broadcom's trailing-twelve-month non-GAAP earnings per share at about $6.29. At the stock's price at the time of this writing, near $365, the stock trades around 58 times that trailing-12-months (TTM) figure -- rich even after factoring in Broadcom's breadth across AI accelerators, ethernet switching, and VMware-driven infrastructure software.

One key risk for Broadcom is that a large slice of near-term growth depends on just a handful of hyperscale customers, and cyclical pockets in legacy networking or storage can offset AI strength. Still, Broadcom's cash generation, dividend capacity, and guidance argue for durable fundamentals as AI builds out. The question is whether that durability is already priced in.

Netflix

Netflix has come to dominate the streaming landscape. However, the bears had a valid argument early on. Since creating and licensing content is so expensive, there were worries that the business would never generate positive free cash flow (FCF). Even though Netflix was growing its subscribers and revenue quickly, the thinking was that it would never be enough.

This is no longer a concern. Netflix raked in $6.9 billion in FCF in 2024, with management expecting $8 billion to $8.5 billion this year. This is up significantly from a loss of $3.3 billion in 2019. Netflix is using excess cash to repurchase shares.

The company is demonstrating the advantage it has achieved from its massive scale. Netflix can spread large content costs over a huge customer and revenue base, allowing it to generate robust profits.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.