The One Thing Every Investor Should Know About the Stock Market Right Now

Key Points

The S&P 500’s average price-to-earnings ratio has raced to uncomfortably high levels.

There’s a significant footnote, however, to add to the data.

Most investors have yet to notice that while some large-cap stocks are now richly priced, another group of attractive stocks has become measurably cheaper as a result.

You don't need to know every little detail about the stock market to be a successful investor. You just need to know enough of the right ones.

However, there's one important detail every investor should know about the market right now: Its overall, aggregate valuation. A quick check will show that the market is in eye-popping territory here.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Yes, stocks as a whole are expensive right now

Does a stock's price (relative to its per-share earnings) matter? Most growth investors would say it doesn't -- at least not nearly as much as revenue growth does, or even a company's apparent potential. Profits are often seen as something to worry about once a company is producing sales growth by penetrating a particular market.

To be fair, this mindset has paid off handsomely for over a couple of decades now. Amazon and Facebook's parent Meta Platforms are two great examples of where it has worked.

The thing is, earnings-based valuations don't matter right up until the point in time that they do. And once they do, the market tends to make any necessary corrective adjustments in a hurry. If the correction is steep enough, it falls into bear market territory.

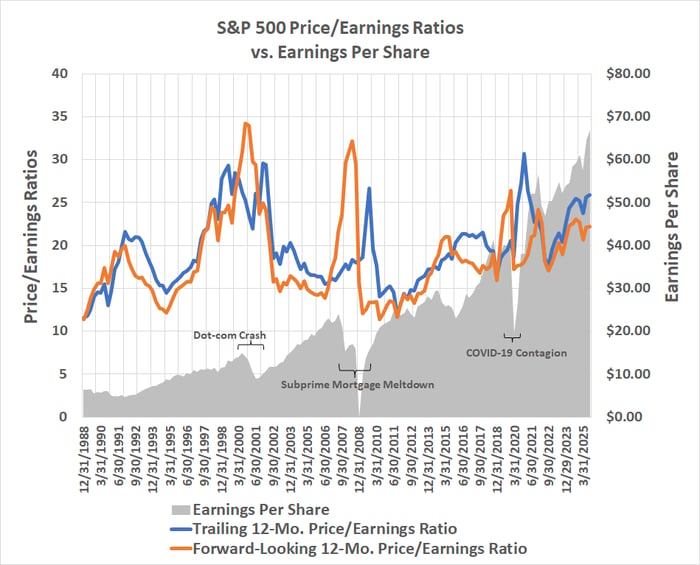

There's the rub for sidelined investors right now. The market is still (mostly) moving higher in step with earnings, shrugging off any attempts at even a modest correction. In the absence of any real, prolonged correction since mid-2022, though, this rally has outpaced earnings growth. The result? The S&P 500's (SNPINDEX: ^GSPC) trailing price/earnings ratio now stands at nearly 26, while its forward-looking P/E ratio is more than 22. Both are well above their long-term norms.

Data source: Standard & Poor's. Chart by author.

What gives? Why are investors willing to pay premium prices now that they've not been willing to pay (in a normal economic environment, anyway) since the dot-com craze of the late 1990s that led to a major crash in the early 2000s?

In many ways, it's the same kind of thinking at work now. There's a small handful of technology companies producing -- or at least promising -- incredible growth. Only now, rather than the advent of the internet, it's the advent of artificial intelligence that's driving the bullishness. (In the interest of fairness, unlike far too many dot-com companies then, most of today's AI-related outfits at least have a shot at eventually becoming profitable.)

Still, it's not just a feeling. The overall market's valuation is uncomfortably steep here. Something's got to give sooner or later.

The rest of the valuation story

However, most stocks may not be quite as overvalued as they seem to be, based on the broad numbers.

Blame the so-called "Magnificent Seven" stocks like Nvidia, Microsoft, Apple, and the aforementioned Meta and Amazon for the current situation. Although these seven names only make up 1.4% of the tickers found in the S&P 500, they collectively account for nearly one-third of the index's total value and market cap. If they're richly priced, it skews the S&P 500's trailing and forward-looking price/earnings ratio higher.

And they are most definitely richly priced at this time. Market-leading Nvidia's trailing P/E is nearly 50, while Apple's and Microsoft's trailing price/earnings ratios are closer to 40 than to 30. Numbers crunched by Yardeni suggest the Magnificent Seven's forward-looking P/E currently stands at nearly 29 versus the S&P 500's comparison of only 22, which implies that the average forward-looking P/E for every other S&P 500 constituent closer to the longer-term norm is near 20.

Image source: Getty Images.

This is seemingly good news for investors' positions outside of the Magnificent Seven names. There's still measurable price-based risk, though. The Magnificent Seven stocks (and their close cousins) may set the tone and the pace for the broad market, but if they undergo a price correction, most other stocks will follow that lead. Sure, there's always a chance that the market could separate itself into two different groups, one of which is AI-driven large caps that suffer a much-needed correction, while the other is everything else. That's not likely, though. Fair or not, stocks tend to move as a herd.

Investors need an action plan

This backdrop leaves all investors in something of a lurch -- stocks are expensive, but they're still rising on low-double-digit earnings growth that's expected to last at least through the end of next year.

It's conceivable that stocks could still inch their way forward while waiting for earnings to catch up, dialing back at least some of this frothy valuation. This would be a bit of a rarity, though. Right or wrong, the market tends to soar or tumble these days; there's rarely a middle ground with its performance.

The solution (for the time being anyway) may be doing nothing, remembering that stocks ebb and flow, but also remembering that you can't accurately predict when these ebbs and flows start. It may not feel right to simply ignore these steep valuations. But your priority as an investor is mostly just making sure you're in the market when earnings are on the rise, as they still are. Given enough time, everything else tends to work itself out, even if that means riding out a bit of a setback. It'll pass soon enough.

That being said...

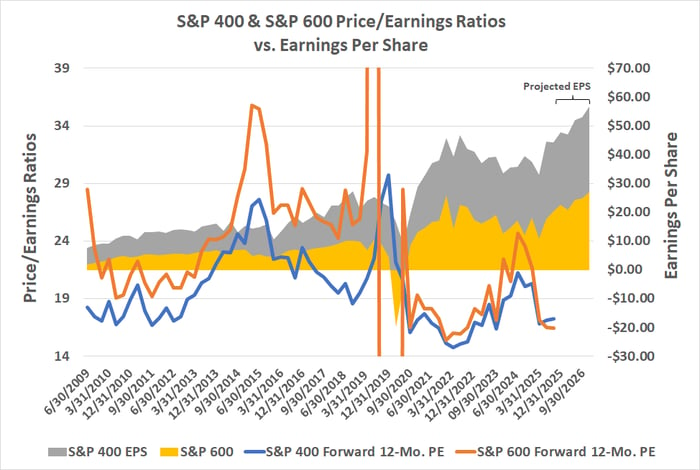

The interesting detail no one seems to be talking about here is the fact that it's only large-cap stocks -- as reflected by the S&P 500 -- sporting pumped-up valuations. The small-cap stocks that make up the S&P 600, along with the mid-caps that make up the S&P 400, have actually gotten cheaper as large-caps have become more expensive. Yardeni reports that the S&P 400's forward-looking price/earnings ratio currently stands at only 16.4, in fact, while the S&P 600's is slightly lower at 15.7.

Data source: Standard & Poor's. Chart by author.

So, if you're looking for a way to shield yourself from the unknown fallout from large-cap stocks' frothy valuations, it's absolutely possible that these names that have been mostly disconnected from their large-cap counterparts will remain disconnected in the event of a market correction that right-prices the S&P 500, pushing them higher while large caps move lower.

Nevertheless, be smart. Any bearish headwind aimed at large-cap stocks still means you'll want to carefully select individual small and mid-sized names. Marketwide corrections can be pretty indiscriminate.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, Stock Advisor’s total average return is 1,066%* — a market-crushing outperformance compared to 186% for the S&P 500.

They just revealed what they believe are the 10 best stocks for investors to buy right now, available when you join Stock Advisor.

*Stock Advisor returns as of September 8, 2025

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Apple, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Related Articles

Amazon Stock Predictions for 2026 to 2030: Will They Exceed Expectations and Achieve Major Long-Term Goals?

TradingKey - As we head into 2026, many investors are questioning where Amazon (AMZN) fits into the technology world.

A Crash After a Surge: Why Silver Lost 40% in a Week?

TradingKey - Spot silver (XAGUSD) prices continue to decline. Silver plunged 20% on Thursday, breaking below $71 per ounce, with the sell-off intensifying on Friday as prices fell further below $64. Compared to the all-time high set on January 29, silver prices have retraced more than 40%, wiping out nearly all gains accumulated over the previous month.

Is Bitcoin’s Four-Year Cycle Dead in 2026?

Is the Bitcoin 4-year cycle dead? After 2025 broke historical records with a red post-halving year, institutional analysts explore if the Bitcoin price has decoupled from the halving countdown. Analyze the impact of spot ETFs, global liquidity, and the roadmap to the 2028 halving in this 2026 market

Why Ripple ETFs are Winning the Capital War Against Bitcoin

While Bitcoin and Ethereum ETFs face massive outflows, XRP ETFs have defied market trends with a historic 30-day inflow streak reaching $1.37 billion. Explore why institutional "smart money" is rotating into Ripple, the structural impact of the "Liquidity Lock," and why analysts set a 2026 price tar