Should You Buy Robinhood Markets While It's Below $110?

Key Points

Robinhood has a paid subscriber base of 3.2 million users.

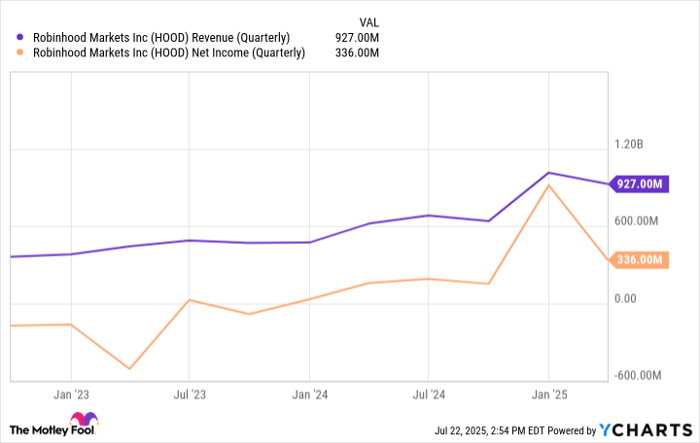

The online brokerage generated $927 million in net revenue in Q1 2025.

The company has $2.2 billion in net cash on its balance sheet.

In January, I highlighted Robinhood Markets (NASDAQ: HOOD) as a stock to buy for long-term investors, despite doubts about whether the company could do more than disrupt the brokerage industry. Back then, it was trading around $40 per share, and many still questioned its staying power.

Fast-forward six months -- not yet the long term -- and the stock has surged past $100, lifting its market capitalization to nearly $90 billion, resulting in a remarkable 173% increase year to date. With shares now near all-time highs, let's dive into what's driving this momentum, what lies ahead, what could go wrong, and whether the stock still makes sense for investors.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Here's how Robinhood is growing so quickly

Robinhood delivered standout Q1 2025 results, with revenue soaring 50% year over year to $927 million. The biggest driver was a 77% surge in transaction-based revenue, which climbed to $583 million.

Robinhood's second-largest revenue stream, net interest income, rose 14% to $290 million, fueled by a larger base of interest-earning assets and a continued ramp-up in securities lending.

Moreover, the brokerage gained $2 billion in net deposits in the quarter to a record $18 billion, and Robinhood Gold, the company's subscription offering that costs $5 per month or $50 annually, saw subscribers nearly double year over year from 1.7 million to 3.2 million.

Robinhood CEO Vlad Tenev summed up the growth on the Q1 earnings call: "Customers are not only trading more with us, but they're entrusting us with more of their assets."

As for how its growth is translating to the bottom line, Robinhood produced $336 million in net income, an impressive increase of 114% year over year.

HOOD Revenue (Quarterly) data by YCharts

Can Robinhood continue to grow?

As for where Robinhood goes from here, the company acquired TradePMR, a trading platform designed for independent registered investment advisors, for $300 million in cash and stock. The deal, which allows Robinhood entry into the wealth management sector, is another step in diversifying its business.

Additionally, Robinhood recently closed on its $200 million acquisition of Bitstamp, the world's longest-running cryptocurrency exchange, to broaden its addressable market outside of the U.S.

"Our 10-year arc, our long-term arc, is to build the No. 1 global financial ecosystem," Tenev added on Robinhood's most recent earnings call. "That means expanding our business from retail only, which it pretty much is now, to also serving businesses and institutions, and also expanding from primarily U.S. to being a full global platform serving customers everywhere."

Notably, Robinhood has nine different businesses that each generate at least $100 million in annualized revenue, nearly twice as many as a couple of years ago. Tenev also mentioned other opportunities for growth, including building out 24-hour trading, 401(k) administration for businesses, and employee stock plan administration for public companies.

Image source: Getty Images.

Here's what could go wrong for Robinhood

As of now, considering Robinhood's high growth, profitability, and clean balance sheet with $2.2 billion in net cash, you'd be hard pressed to find any problems with its business. However, the stock can be a different story.

For high-growth companies like Robinhood, their stocks typically have two issues: share dilution and valuation.

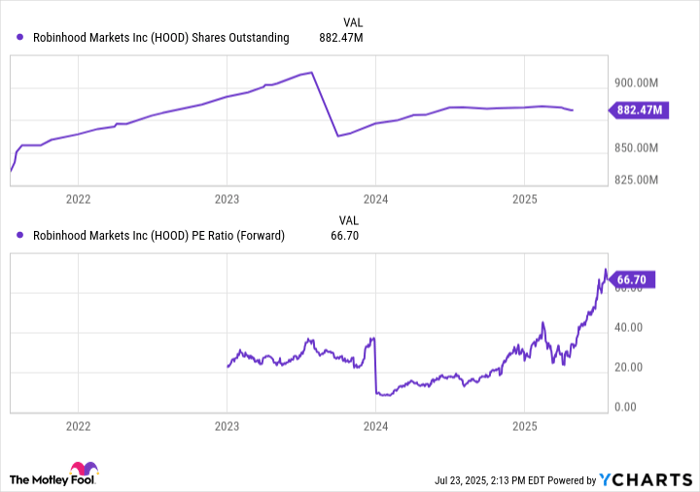

Since its IPO, Robinhood's share count has risen by 5.6%, which dilutes investors' ownership stake. The good news is that management is addressing the concern, lowering share-based compensation from $871 million in 2023 to $304 million in 2024. Additionally, management recently increased its share repurchase authorization from $1 billion to $1.5 billion, or nearly all of its $1.6 billion in trailing 12 months of net income. According to management, the buybacks will decrease its share count by approximately 1% in 2025.

As for the stock's valuation, Robinhood now trades at roughly 67 times forward earnings estimates, near an all-time high.

That's a steep price tag for a company still pouring resources into growth and customer acquisition. While Robinhood's roadmap includes promising new products that could eventually justify the valuation, many remain early stage ideas with no guarantee they will turn into meaningful profits.

HOOD Shares Outstanding data by YCharts

Is Robinhood stock a buy?

Robinhood continues to prove its doubters wrong. With 75% of its 25 million funded accounts coming from members of the millennial and Gen Z generations, the platform is well-positioned for long-term growth as those users get older and build wealth.

Still, with shares near all-time highs and valuation stretched, now may not be the best entry point. Long-term investors who believe in the vision might consider holding or dollar-cost averaging, i.e., investing a set amount at predetermined times. But chasing the stock after its massive run comes with real risk for future returns.

Should you invest $1,000 in Robinhood Markets right now?

Before you buy stock in Robinhood Markets, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Robinhood Markets wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $636,774!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,064,942!*

Now, it’s worth noting Stock Advisor’s total average return is 1,040% — a market-crushing outperformance compared to 182% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of July 21, 2025

Collin Brantmeyer has positions in Robinhood Markets. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Related Articles

National Debt Bomb Ignited? Musk Warns U.S. Will Be 1000% Bankrupt Without AI

TradingKey - Tesla (TSLA) CEO Elon Musk recently issued another warning regarding the rapidly ballooning U.S. national debt. He stated clearly that without artificial intelligence and robotics, the United States will inevitably head toward fiscal bankruptcy.

Tesla Stock Outlook: Competing With Rivian, Robotaxi Potential, and 2026 Prospects

There is much conversation about the prospect of investing in Tesla (TSLA) as we move closer to 2026. The volatility of its share price in 2025 is leading many investors to consider if they should purchase shares of Tesla given the alternatives available in terms of electric vehicles (Rivian, etc.).

Why Sanae Takaichi Winning Japan’s Diet Election Led to a Surge in Japanese Stock Indices?

TradingKey - Reports indicate that the ruling coalition led by Japanese Prime Minister Sanae Takaichi has secured a single-party majority in the parliamentary elections held on Sunday (February 8). Following the news, the yen weakened slightly, while the Nikkei Index surpassed 57,000 for the first t

A Crash After a Surge: Why Silver Lost 40% in a Week?

TradingKey - Spot silver (XAGUSD) prices continue to decline. Silver plunged 20% on Thursday, breaking below $71 per ounce, with the sell-off intensifying on Friday as prices fell further below $64. Compared to the all-time high set on January 29, silver prices have retraced more than 40%, wiping out nearly all gains accumulated over the previous month.