Nvidia Stock Looks Cheap Right Now, but Here's 1 Reason It Could Actually Be Expensive

The artificial intelligence (AI) behemoth Nvidia (NASDAQ: NVDA) has gotten off to a rocky start this year, with shares down about 9% (as of March 24) so far in 2025. The emergence of the Chinese AI chatbot DeepSeek, concerns about economic growth, and President Donald Trump's proposed tariffs have led investors to reconsider the popular AI trade.

But as most long-term investors know, sell-offs are often opportunities to buy shares of great companies at more attractive valuations, especially if the company's fundamentals are still intact. Many would argue that this is the case for Nvidia, with Wall Street near a consensus buy on the stock.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

However, while Nvidia stock may in fact be cheaper right now, there's one reason it actually could be expensive.

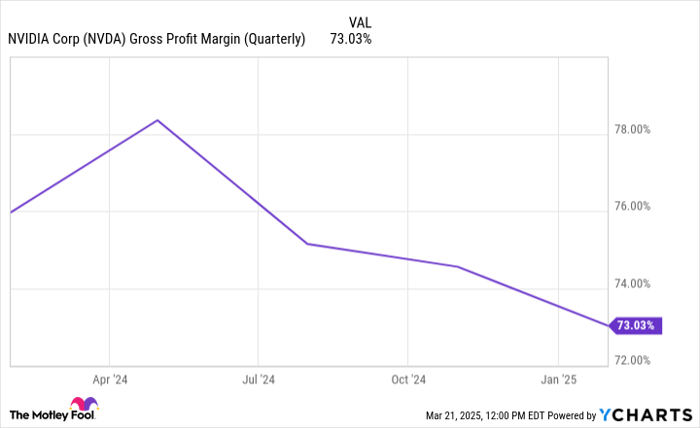

Contracting margins

A big part of the Nvidia story over the years and in the present is the company's incredible margins. Gross margin is calculated by taking revenue, subtracting the cost to make the goods sold, and then dividing this number by revenue. While gross margin doesn't account for all expenses at a company, it looks at the money retained after the costs to make a product. A high gross margin also indicates efficiency and pricing power because it suggests a company has the power to set a high cost relative to the cost of the good. That implies there is an inelastic demand.

Data by YCharts.

As you can see, Nvidia's gross margin has contracted in recent quarters. In the company's fiscal 2025 fourth quarter (ended Jan. 26, 2025), the gross margin fell to just over 73%. That's still an incredible gross margin and earnings still increased from the third quarter. But it also means that the increase in the cost to make Nvidia's chips and other AI infrastructure didn't translate into as much revenue growth. For instance, in the company's third quarter, the cost of revenue grew 20% from the prior quarter and revenue grew 17%. But in the fourth quarter, the cost of revenue rose 19%, while revenue only grew 12% quarter over quarter.

This might lead investors to believe that pricing power is eroding and there is more competition than initially believed, especially considering that Nvidia's margin is so high. On Nvidia's fourth-quarter earnings call, CFO Colette Kress said that its gross margin should remain in the low 70s as the company's next-generation Blackwell chips ramp up, but there will be an opportunity to see gross margin rebound back into the mid-70s later in fiscal year 2026 (now underway).

Wall Street analysts seem to be giving the company the benefit of the doubt. Analysts on average expect the gross margin to bottom in the current quarter at 71.1%, according to data provided by Visible Alpha. They then expect the gross margin to rebound to nearly 74.5% by the end of fiscal year 2026. Diluted earnings per share are also expected to grow by nearly 48% in fiscal 2026 on a year-over-year basis.

Is Nvidia over-earning right now?

Nvidia currently trades slightly under 26 times forward earnings, which is much more appealing than when the stock traded at about 50 times forward earnings or more not too long ago. However, if management turns out to be incorrect and Nvidia's margin continues to contract, then Nvidia could actually be over-earning right now and its price-to-earnings (P/E) ratio would significantly increase if its market capitalization holds.

As already mentioned, analysts currently project the gross margin will rebound this year and this very well could happen. It's something investors should consider not just with Nvidia, but with any stock they are covering. The forward P/E ratio (which relies on estimates) is a great indicator of where a stock is situated but it doesn't always tell the full story. The actual earnings of a company are critically important and can significantly impact the P/E ratio. It's certainly going to be a big driver for Nvidia's stock price this year.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $305,226!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $41,382!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $517,876!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of March 24, 2025

Bram Berkowitz has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.

Recommended Articles