Think Snowflake Stock Is Expensive? This Chart Might Change Your Mind.

Snowflake (NYSE: SNOW) has experienced significant activity since its September 2020 initial pubic offering (IPO). Between the company's rally in the bull market of 2021 and its lows amid a surprise leadership change earlier this year, investors generally have considered it an expensive stock.

However, one key metric took a hit during its sell-off earlier in the year. Now, investors feel a restored level of confidence and have rallied around the new CEO and the artificial intelligence (AI)-oriented direction of the company. Consequently, its comparatively low valuation by one measure could help boost the stock.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

Why Snowflake isn't so expensive

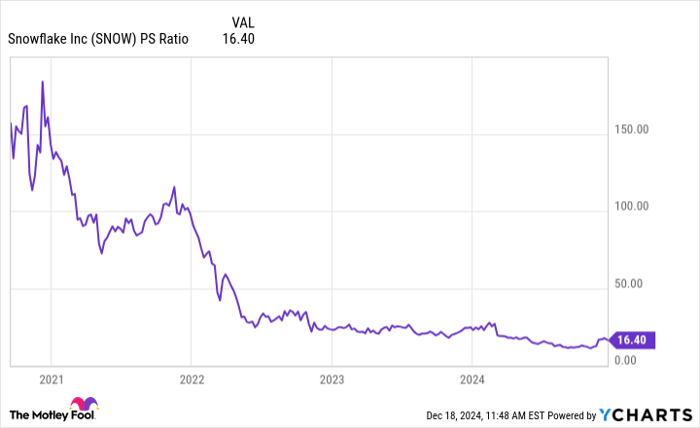

Investors should question the narrative that Snowflake is expensive due to its price-to-sales ratio (P/S) of 16.

SNOW P/S Ratio data by YCharts.

Admittedly, persuading investors to see 16 times sales as "cheap" is a hard sell, even when talking about the highest-quality stocks. It doesn't help that ongoing losses leave the company without a P/E ratio or that the stock trades at 19 times its book value.

However, the 16 P/S ratio isn't far above the record low valuation for Snowflake. Moreover, the stock began its history as a much pricier stock since investors bid its sales multiple to stratospheric levels. In December 2020, the P/S ratio reached a high of 183, meaning the current sales multiple of 16 is more than a 90% discount from the metric's all-time high.

Additionally, as mentioned before, CEO Sridhar Ramaswamy seems to be winning over investors. After he credited AI with the company's growth in the fiscal third quarter of 2025 (ended Oct. 31), the stock shot 25% higher following the announcement and has held on to most of those gains.

Furthermore, investors should remember that Snowflake stock sold at close to a 25 P/S ratio before the CEO change in late February. Given the AI-driven growth, investors may want to consider buying the software-as-a-service (SaaS) stock before rising confidence levels take the sales multiple back to levels experienced under the previous management team.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $349,279!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $48,196!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $490,243!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of December 16, 2024

Will Healy has positions in Snowflake. The Motley Fool has positions in and recommends Snowflake. The Motley Fool has a disclosure policy.

Related Articles

Amazon Stock Predictions for 2026 to 2030: Will They Exceed Expectations and Achieve Major Long-Term Goals?

TradingKey - As we head into 2026, many investors are questioning where Amazon (AMZN) fits into the technology world.

A Crash After a Surge: Why Silver Lost 40% in a Week?

TradingKey - Spot silver (XAGUSD) prices continue to decline. Silver plunged 20% on Thursday, breaking below $71 per ounce, with the sell-off intensifying on Friday as prices fell further below $64. Compared to the all-time high set on January 29, silver prices have retraced more than 40%, wiping out nearly all gains accumulated over the previous month.

Is Bitcoin’s Four-Year Cycle Dead in 2026?

Is the Bitcoin 4-year cycle dead? After 2025 broke historical records with a red post-halving year, institutional analysts explore if the Bitcoin price has decoupled from the halving countdown. Analyze the impact of spot ETFs, global liquidity, and the roadmap to the 2028 halving in this 2026 market

USD Dollar Trend Forecast: Dollar Index Falls Below 97.0 to 4-Year Low, Will the Dollar Continue To Fall or Bottom Out in 2026?

TradingKey - In January 2026, the US Dollar Index continued its downward trend from 2025, officially breaking below the key 97.0 level and reaching a low of 95.5, marking a nearly four-year low since February 2022.