Tariffs Becoming an Inflationary Anchor? Powell Hints: Without Trump’s Tariff Policies, Rate Cuts Might Have Already Started

TradingKey – On the evening of July 1 (U.S. Eastern Time), all eyes were on the policy tug-of-war between Federal Reserve Chair Jerome Powell and President Donald Trump.

Speaking at the Sintra conference in Portugal, Powell reiterated that the Fed’s rate-cutting path remains strictly data-dependent, and pointed out that without the inflationary pressure from Trump’s tariff policies, the central bank might have already begun its easing cycle in 2025.

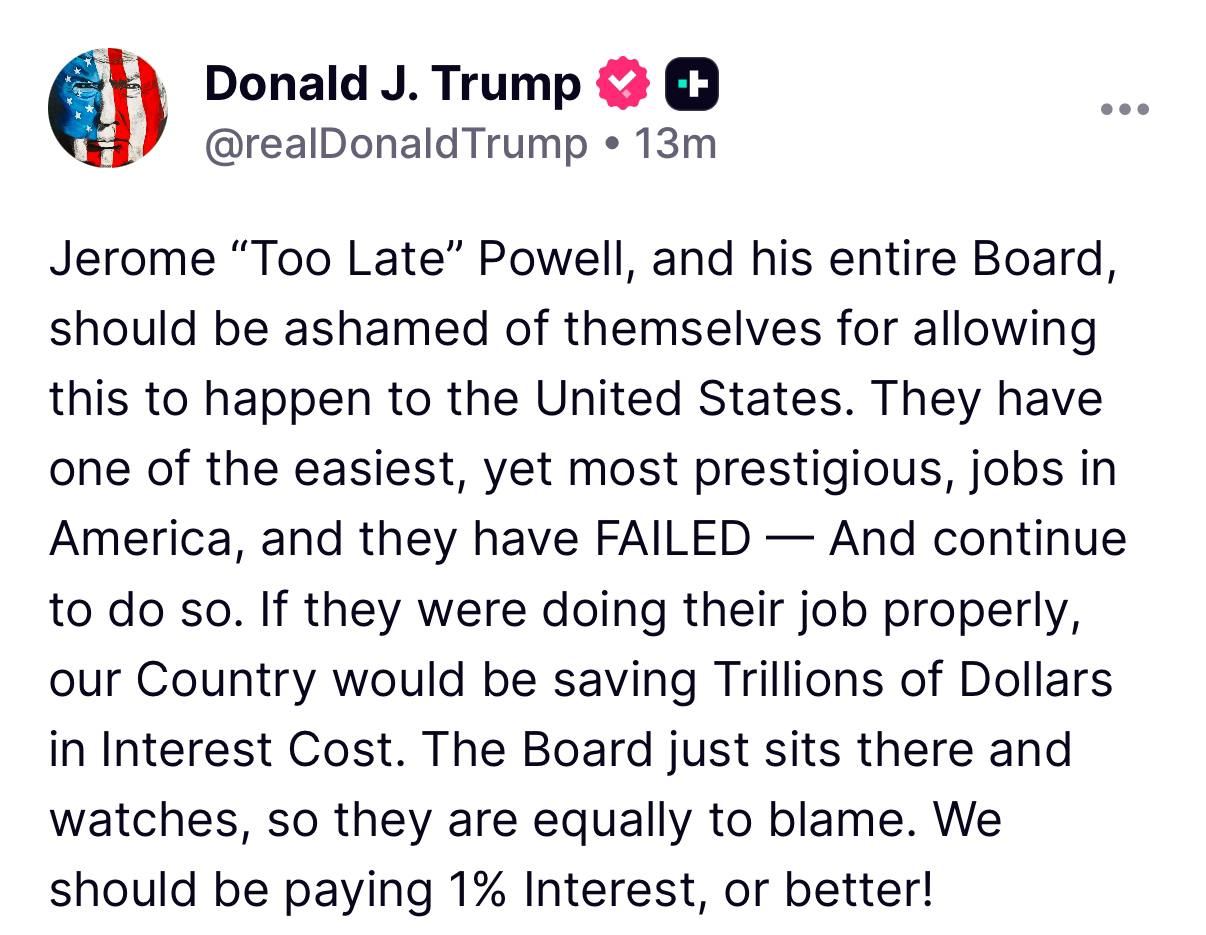

His remarks were seen as a direct response to ongoing political pressure from Trump, who once again criticized Powell on June 30:

"I think we should be paying 1% right now, and we're paying more because we have a guy who suffers from, I think, Trump Derangement Syndrome,"

Faced with increasing White House pressure, Powell remained composed: “I'm very focused on just doing my job.”

When asked about his potential reappointment, he gave no clear answer, only stating that he hopes to hand over a stable economic environment to his successor.

Market expectations for a July rate cut have picked up slightly, with federal funds futures pricing in around a 25% chance of a cut this month. Goldman Sachs also updated its forecast, now expecting the Fed to begin cutting rates in September — three months earlier than previously anticipated, with possible reductions of 25 basis points in September, October, and December.

Meanwhile, at its most recent meeting in June, the Federal Reserve reaffirmed its decision to keep interest rates steady at 4.25%–4.5%, marking the seventh consecutive meeting since December 2024 where no rate changes were made.

The ongoing clash between Trump and Powell over interest rates has become one of the key variables shaping global financial markets in the second half of 2025, with every comment and move closely watched by investors worldwide.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.