Applied Materials Inc Stock (AMAT) Moved Up by 5.17% on Jun 29: Drivers Behind the Movement

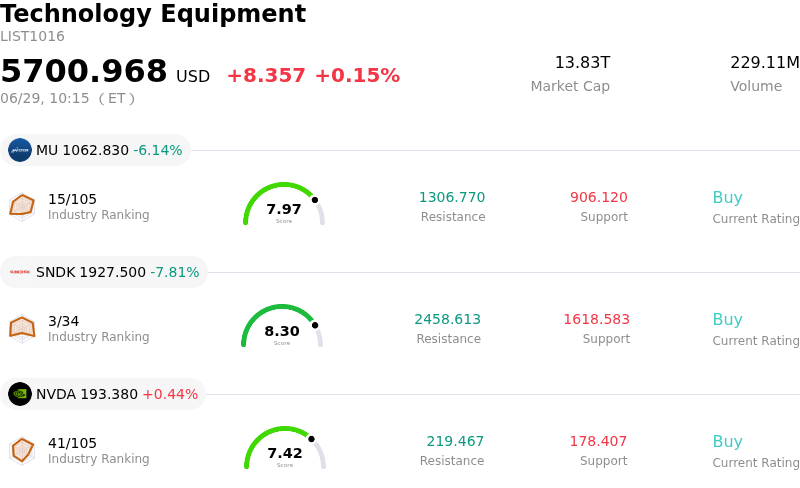

Applied Materials Inc (AMAT) moved up by 5.17%. The Technology Equipment sector is up by 0.15%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 6.14%; SanDisk Corporation (SNDK) down 7.81%; NVIDIA Corp (NVDA) up 0.40%.

What is driving Applied Materials Inc (AMAT)’s stock price up today?

The significant positive price movement in Applied Materials is primarily driven by strong fundamental momentum following a high-conviction product showcase and a wave of aggressive target price upgrades by major Wall Street firms. At its Master Class event, the company unveiled a suite of six new chipmaking systems specifically designed to accelerate DRAM production and advanced packaging. These new systems directly address the industry-wide memory wall, which limits artificial intelligence compute performance by restricting the speed at which data moves between memory and processors.

In response to this product launch and the company's clear leadership in the semiconductor capital equipment sector, several prominent financial institutions upgraded their forecasts on Monday. KeyBanc Capital Markets raised its target price on the stock to reflect an attractive relative valuation and sustained growth, pricing the shares based on higher forward earnings estimates. Similarly, Cantor Fitzgerald significantly increased its price target, highlighting the company's strong growth prospects. Other major institutions, including Jefferies, B. Riley, Wells Fargo, and Bank of America, also hiked their price targets while maintaining optimistic ratings. This broad analyst upgrade cycle has heavily boosted investor confidence and acted as a major catalyst for the current session's gains.

The bullish sentiment is further reinforced by positive developments across the broader semiconductor industry. Micron Technology's recent blockbuster earnings results served as a direct validation of Applied Materials' strategic focus on memory and packaging tools, signaling that AI-driven memory demand remains exceptionally strong. Additionally, the stock's upward movement represents a robust recovery from a sharp sell-off in the previous trading session, which was driven by late-quarter institutional profit-taking and temporary sector-wide rotation. With management maintaining strong visibility over future orders and projecting rapid earnings growth for the upcoming quarter, investors have quickly reassessed the long-term outlook, driving the stock higher as the market recognizes the durability of the current artificial intelligence infrastructure build-out.

Technical Analysis of Applied Materials Inc (AMAT)

Technically, Applied Materials Inc (AMAT) shows a MACD (12,26,9) value of 12.695, indicating a buy signal. The RSI at 63.925 suggests neutral condition and the Williams %R at 20.907 suggests buy condition. Please monitor closely.

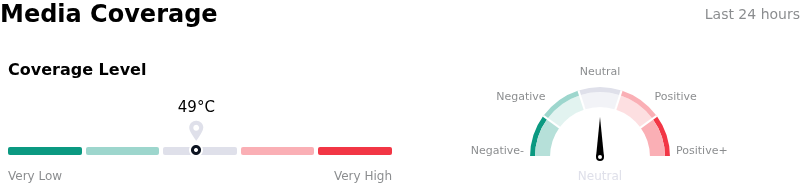

Media Coverage of Applied Materials Inc (AMAT)

In terms of media coverage, Applied Materials Inc (AMAT) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Applied Materials Inc (AMAT)

Applied Materials Inc (AMAT) is in the Technology Equipment industry. Its latest annual revenue is $28.37B, ranking 10 in the industry. The net profit is $7.00B, ranking 6 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $554.63, a high of $790.00, and a low of $308.00.

More details about Applied Materials Inc (AMAT)

Company Specific Risks:

- Downstream Capital Expenditure Slowdown: Reports that major memory producer SK Hynix is moderating its High-Bandwidth Memory (HBM) expansion present an immediate threat to Applied Materials. Because the company is heavily exposed to DRAM and NAND flash deposition, etching, and process control tools, a capital spending deceleration by key Asian chipmakers risks creating a tool oversupply and weakening AMAT's mid-term order pipeline.

- Aggressive and Concentrated Insider Liquidations: Recent SEC Form 4 and Form 144 filings reveal intense executive de-risking, with over $114 million in insider stock sales over the last three months and zero purchasing activity. Headline liquidations by CEO Gary Dickerson ($42.5 million), SVP/CTO Omkaram Nalamasu ($14.4 million), and Semiconductor Products Group President G. Raja Prabu ($25.3 million) put downward pressure on the stock and signal that leadership may view current prices as a near-term valuation ceiling.

- Severe Free Cash Flow and Liquidity Contraction: Despite strong headline revenues, the company's quarterly free cash flow severely contracted year-over-year to $210 million, significantly missing the institutional consensus expectation of $1.6 billion. This cash drain is driven by mounting working capital requirements to build advanced materials inventory and self-fund highly capital-intensive projects, such as the $500 million Singapore manufacturing facility expansion, which restricts immediate financial flexibility.

- Stretched Valuation and Multiple Compression Risk: Following intense AI-driven speculation, AMAT's trailing P/E ratio has expanded past 55x–61x, representing a significant premium over its 5-year median P/E of 20.4x. Trading well above historical averages leaves the stock highly vulnerable to sharp multiple compression in the event of macroeconomic shocks, rising Treasury yields, or a reassessment of near-term AI spending.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.