Ferguson Enterprises Inc Stock (FERG) Moved Up by 3.33% on Jun 18: What Signal Does It Send?

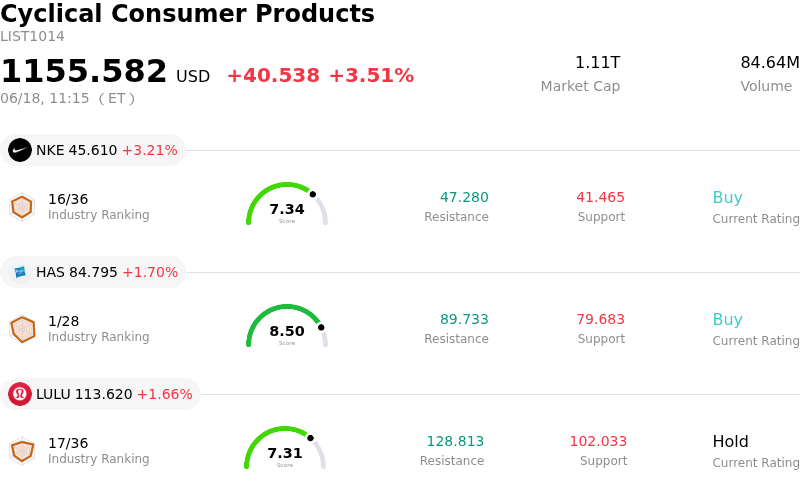

Ferguson Enterprises Inc (FERG) moved up by 3.33%. The Cyclical Consumer Products sector is up by 3.51%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Nike Inc (NKE) up 3.16%; Hasbro Inc (HAS) up 1.70%; Lululemon Athletica Inc (LULU) up 1.56%.

What is driving Ferguson Enterprises Inc (FERG)’s stock price up today?

Ferguson Enterprises is experiencing upward price momentum and notable intraday volatility following a series of significant strategic and structural updates that have bolstered investor confidence. Chief among these developments is the company's recent announcement that it will simplify its listing structure by canceling its secondary listing on the London Stock Exchange, effective in July. By consolidating its trading solely on the New York Stock Exchange, where trading liquidity is significantly higher, the company is eliminating the administrative complexities and overhead costs associated with a dual listing. This decisive shift aligns the company's equity market presence directly with its core North American operations and customer base, a move that institutional investors have welcomed.

Furthermore, the stock is benefiting from the ongoing positive execution of its capital allocation strategy. The board previously authorized a substantial new share repurchase program of up to two billion dollars, signaling strong confidence that the company's shares are undervalued. This buyback program, paired with a solid dividend payment scheduled for July, continues to provide a robust floor for the stock price. Institutional backing remains strong, with major hedge funds and asset managers maintaining or increasing their stakes in the business, further underscoring market confidence in the firm’s long-term value proposition.

Underpinning this structural transition is the company's steady operational performance in the North American construction and infrastructure distribution sectors. Although the broader residential construction market faces mixed conditions, Ferguson's recent quarterly financial results demonstrated solid resilience. The company delivered a comfortable earnings-per-share beat and modest top-line expansion, driven by its strategic focus on high-margin HVAC expansions, private label offerings, and disciplined cost management. Positive analyst revisions and elevated price targets following these results continue to support the stock's upward trajectory, as market participants digest the combined impact of listing consolidation, structural cost reductions, and aggressive share buybacks.

Technical Analysis of Ferguson Enterprises Inc (FERG)

Technically, Ferguson Enterprises Inc (FERG) shows a MACD (12,26,9) value of 2.860, indicating a neutral signal. The RSI at 47.411 suggests neutral condition and the Williams %R at 50.380 suggests neutral condition. Please monitor closely.

Fundamental Analysis of Ferguson Enterprises Inc (FERG)

Ferguson Enterprises Inc (FERG) is in the Cyclical Consumer Products industry. Its latest annual revenue is $12.83B, ranking 6 in the industry. The net profit is $786.00M, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $282.75, a high of $315.00, and a low of $204.56.

More details about Ferguson Enterprises Inc (FERG)

Company Specific Risks:

- London Stock Exchange Delisting Friction: Ferguson’s formal June 16, 2026, announcement to cancel its secondary listing on the LSE effective July 20, 2026, forces U.K. Depositary Interest (DI) holders to actively convert to NYSE-traded shares. This creates administrative complexity and risks triggering near-term selling pressure from European investors who are unable or unwilling to custody U.S. equities.

- Executive Insider Trading Signal Concerns: The early June 2026 adoption and execution of Rule 10b5-1 trading plans by senior executives, including the CEO and CHRO, has sparked negative market sentiment and analyst concerns over insider liquidations, especially as the stock navigates a period of mixed top-line performance.

- Cyclical Housing and Residential Headwinds: The business remains highly vulnerable to prolonged high-interest-rate environments and affordability constraints, which continue to depress new residential construction and repair/remodel demand, threatening organic revenue growth in its core water and air solutions segments.

- Tight Liquidity Metrics: With a quick ratio of 0.96, the company faces relatively tight near-term liquidity, which could constrain operational flexibility as it attempts to execute its newly authorized $2.0 billion share repurchase program alongside capital-intensive HVAC acquisitions.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.