Lam Research Corp Stock (LRCX) Moved Up by 3.51% on Jun 10: A Full Analysis

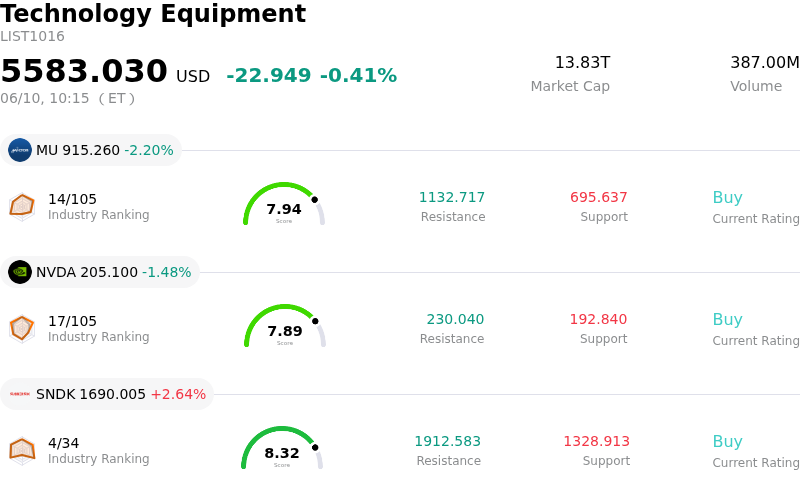

Lam Research Corp (LRCX) moved up by 3.51%. The Technology Equipment sector is down by 0.41%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 1.95%; NVIDIA Corp (NVDA) down 1.48%; SanDisk Corporation (SNDK) up 2.64%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

Lam Research (LRCX) is experiencing intraday volatility today, driven by a confluence of strong financial performance, positive analyst sentiment, and robust industry tailwinds, particularly from the artificial intelligence (AI) sector. The company recently reported strong financial results for its fiscal third quarter of 2026, exceeding both revenue and earnings per share expectations. Additionally, Lam Research has raised its outlook for 2026 wafer fabrication equipment (WFE) spending, signaling increased investment in semiconductor manufacturing.

Analyst ratings reflect this positive momentum, with several firms maintaining or upgrading their recommendations to "Buy" or "Overweight" and significantly increasing price targets for LRCX shares in late May and early June 2026. For example, Wells Fargo and UBS both recently boosted their price targets, indicating a bullish outlook on the company's future. The stock itself has recently reached a new one-year high, suggesting strong investor confidence.

The broader semiconductor industry is experiencing significant growth, with a notable surge in revenue during the first quarter of 2026, largely attributed to strong demand from AI and data centers, especially within the memory market. Lam Research is well-positioned to benefit from these trends, expecting its advanced packaging revenue growth to exceed 50% in calendar year 2026. The company's strategic focus on the increasing demand for AI-driven technologies in semiconductor manufacturing is a key factor supporting its performance.

Despite the predominantly positive news, the observed intraday volatility could be due to several factors. Some investors might be engaging in profit-taking after the stock's substantial recent rally. There are also ongoing discussions about the company's valuation, with some commentary suggesting the stock may appear overvalued even with the strong AI-related growth prospects. Furthermore, certain institutional investors have made adjustments to their positions, with some reducing their holdings, which can contribute to short-term market fluctuations. The overall market sentiment for the semiconductor sector can also influence LRCX, as seen in past instances where industry-wide sell-offs affected the stock.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of [15.23], indicating a neutral signal. The RSI at 59.36 suggests neutral condition and the Williams %R at -30.64 suggests oversold condition. Please monitor closely.

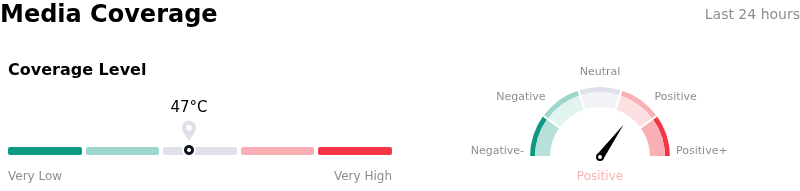

Media Coverage of Lam Research Corp (LRCX)

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 47, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $317.98, a high of $385.00, and a low of $213.00.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Increased geopolitical risk due to recent U.S. restrictions on chip equipment shipments to China, directly impacting market access and future revenue streams for Lam Research, which has significant exposure to the Chinese market.

- Heightened valuation risk as the stock is considered significantly overvalued by analysts (e.g., Morningstar estimated 46% overvalued, and current forward P/E is elevated compared to historical averages), making it susceptible to sharp corrections during broader market downturns or negative news.

- Potential for declining gross and operating margins, as indicated by an analyst downgrade citing management's forecast for a slight gross margin decline in the current quarter.

- Recent insider selling activity, including a Form 144 filing on June 1, 2026, may signal a lack of confidence among company insiders regarding near-term prospects.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.