Oracle Earnings Preview: Market Focuses on OCI Growth and Order Fulfillment, Shares May Rise to $400 by 2026

AI Podcast

Oracle's fiscal Q4 earnings will focus on OCI's sustained growth and order backlog conversion. The stock has seen significant gains, and robust OCI performance and backlog realization could drive further upside. Conversely, decelerated OCI growth, missed backlog targets, or increased CapEx could pressure the stock. Oracle's cloud infrastructure revenue surged 84% in Q3, with OCI as its primary growth engine. The company's Remaining Performance Obligations (RPO) reached $553 billion, driven by AI cloud contracts. Investors will monitor RPO conversion rates, cloud revenue guidance, and management's FY2027 revenue outlook.

TradingKey - Oracle ( ORCL) will report its fiscal 2026 fourth-quarter earnings on June 10, ET. The market's primary focus for this report is whether the OCI cloud infrastructure business can sustain high growth and if the massive order backlog can be effectively converted into revenue and cash flow.

Since March, Oracle has recorded its fourth consecutive monthly gain, with a cumulative increase of 68%. If Oracle delivers robust OCI growth, a further expanding order backlog, and a clear path for revenue realization in this report, it will provide further support for the stock's upside. Conversely, if OCI growth decelerates, backlog conversion misses expectations, or capital expenditure pressure rises significantly, the stock price will face correction pressure.

Key Earnings Highlight: Can OCI Growth Be Sustained?

In the past, Oracle was primarily viewed by the market as a legacy enterprise software and database giant, but the explosion in AI computing demand is shifting its valuation logic. Rapidly growing demand from Big Tech, AI startups, and enterprise customers for training, inference, cloud-based databases, and high-performance computing has made OCI Oracle's most dynamic growth segment.

Last quarter, Oracle's fiscal 2026 third-quarter results showed that total revenue grew 22% year-over-year to $17.2 billion, while cloud revenue rose 44% to $8.9 billion, with cloud infrastructure (OCI) revenue surging 84% to $4.9 billion. Compared to the 13% growth in its cloud applications business, OCI has emerged as Oracle's strongest growth engine.

Consequently, the market will focus on whether OCI revenue growth can remain elevated in this earnings report. If OCI growth continues to significantly outpace overall cloud revenue growth, it would indicate that AI demand is still being rapidly released, validating Oracle's cloud transformation thesis. Especially as demand for AI training and inference expands, OCI's ability to secure more major contracts will directly influence market projections for revenue growth over the next two to three years.

However, OCI's rapid growth depends not only on demand but also on supply capacity. AI cloud infrastructure requires vast quantities of GPUs, networking equipment, data centers, power, and cooling resources. If Oracle cannot expand capacity in a timely manner, revenue recognition could lag despite a strong order book. Management's guidance on data center delivery timelines, GPU supply, capital expenditures, and customer onboarding progress will be the focal point of the earnings call.

Can more than $500 billion in Remaining Performance Obligations (RPO) be realized?

Oracle's most striking data point last quarter was its Remaining Performance Obligations (RPO), which reached $553 billion, a staggering 325% year-over-year increase and up $29 billion from the previous quarter. The company stated that this growth was primarily driven by large-scale AI cloud contracts.

RPO represents future contracted revenue that has not yet been recognized and is a crucial metric for measuring long-term demand in the cloud business. For investors, however, high RPO growth is only the first step; the key lies in whether these orders can be converted into revenue on schedule. If RPO continues to rise while OCI revenue simultaneously accelerates, it suggests that Oracle's AI cloud orders are being effectively realized. Conversely, if RPO continues to accumulate but revenue recognition misses expectations, the market may grow concerned about prolonged contract cycles, delivery capacity constraints, or uncertainties in customer demand.

Consequently, the core question for this earnings report is whether Oracle can convert its backlogged orders into actual revenue. Investors will focus on RPO growth rates, the proportion of short-term RPO, cloud revenue guidance, and management's commentary regarding fiscal 2027 revenue targets. Oracle previously raised its FY2027 revenue outlook to $90 billion and stated it was confident in meeting or even exceeding this target, which implies that the market already has high expectations for the conversion of these orders.

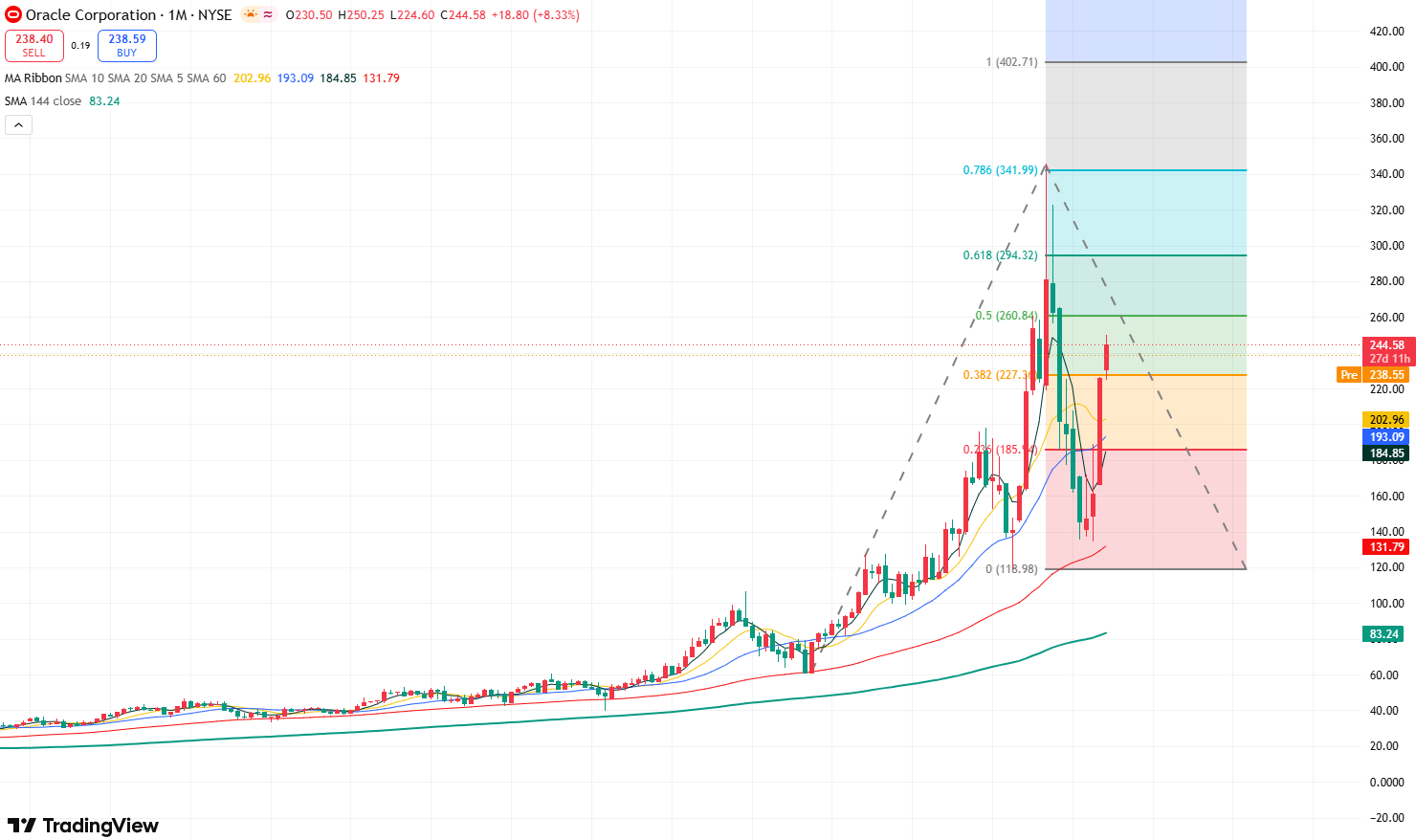

Oracle Technical Analysis: Share Price Projected to Reach $400 by H2 2026

Oracle monthly stock chart, Source: TradingView

Looking at Oracle's monthly chart, the stock experienced a significant retracement after hitting an all-time high of $341.99 last year, with the drawdown reaching approximately 60% by February of this year. However, following four consecutive months of gains, bullish sentiment has returned, and the stock is poised to challenge its previous all-time high of $341.99.

Currently, if Oracle's upcoming earnings report beats expectations, it will support the share price in testing the previous high resistance at $341.99. A breakout above this level would open up upside potential toward the Fibonacci 1.0 extension at $402. Conversely, the stock may pull back to test the $227 support level, with further support at $185.

Oracle weekly stock chart, Source: TradingView

Based on Oracle's weekly chart, if the stock can effectively settle above $250, it may continue to test the $280-$300 resistance range, with stronger resistance in the $320-$340 previous high range. If the rally fails to hold the $238-$250 level, the downside target is initially $220-$225, with further support at $190-$200 and $160-$165.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.