Up 20% in Five Days, Over 50% This Year: Why Was Marvell Technology Tapped by Nvidia?

AI Podcast

Marvell Technology's stock has surged, driven by record FY2026 results and a pivot to AI ASICs and optical interconnects. The company is a key partner for Amazon AWS and benefits from AI computing demand. Strategic acquisitions and a $2 billion Nvidia investment strengthen its position. While facing competition from Broadcom and customer concentration risks, Marvell's growth trajectory is supported by institutional upgrades and optimistic revenue guidance. Future performance hinges on executing its optical interconnect strategy and expanding AI chip penetration.

TradingKey - Since April 2026, Marvell Technology ( MRVL) has shown sustained strength in its stock price performance. On April 10, it closed at $128.49, rising 7.14% on the day, with a cumulative gain of nearly 20% over the past five trading days. The overall gain for April reached 29.72%, the year-to-date increase exceeded 51%, and the 52-week surge was as high as 143.03%. Behind this share price strength are solid financial results and a clear industrial logic.

1. What Does Marvell Technology Do?

Founded in 1995 and headquartered in Santa Clara, California, Marvell Technology was co-founded by Dr. Sehat Sutardja, his wife Weili Dai, and his brother Pantas Sutardja. As a leading global fabless semiconductor company, it has nearly 6,000 employees and R&D centers located across the United States, Europe, Israel, Singapore, and Shanghai, China.

The company was initially known for its storage controller chips before gradually expanding into mobile communications, data centers, and the Internet of Things (IoT). In recent years, it has pivoted entirely to the core sector of custom chips for AI infrastructure. Leveraging its deep expertise in high-speed interconnects and mixed-signal technology, Marvell has emerged as the second-largest player in the global AI ASIC market, behind only Broadcom.

II. Latest Financial Results: A Record-Breaking FY2026

On March 5, 2026, Marvell Technology reported its fourth quarter fiscal 2026 financial results for the period ended January 31, 2026. Revenue reached a record high of $2.22 billion, up more than 20% year-over-year. Net income was approximately $396 million, representing a substantial year-over-year increase of about 97.9% on a GAAP basis. Adjusted earnings per share (EPS) were $0.80, slightly exceeding the market expectation of $0.79.

Full-year performance was even more robust: total revenue for fiscal 2026 was $8.195 billion, up 42% year-over-year, while non-GAAP EPS was $2.84, up 81% year-over-year, with both setting new records. The company also provided optimistic guidance, projecting first quarter fiscal 2027 revenue of approximately $2.4 billion, significantly above the analyst consensus of $2.28 billion. Management has raised its full-year revenue guidance for fiscal 2027 and fiscal 2028 to $11 billion and $15 billion, respectively.

III. How Marvell Technology Generates Revenue?

Marvell Technology's current investment thesis has evolved from a single-chip supplier to a dual-engine synergy of "AI ASIC custom chips" and "optical interconnect technology."

1. AI ASIC Custom Chips

As Google ( GOOGL ), Amazon ( AMZN ), Microsoft ( MSFT) and other cloud giants initiate an "AI computing cost revolution" to seek alternatives beyond Nvidia ( NVDA) GPUs, demand for customized AI ASICs has entered an explosive phase. Broadcom ( AVGO) and Marvell, leveraging their advantages in high-speed interconnects and chip IP, are collaborating with cloud giants to build customized AI computing clusters on demand. Marvell is one of the largest partners for Amazon's AWS Trainium series AI ASICs and is a primary beneficiary of the large-scale deployment of custom chips.

2. Optical Interconnect and Silicon Photonics Technology

When the connection distance in large-scale AI data centers exceeds approximately 10 meters, copper interconnects can no longer meet bandwidth and distance requirements, necessitating a transition to optical interconnect systems. Marvell has deep technical expertise in optical DSP and optical interconnect products. To this end, the company recently accelerated its strategic positioning through two key acquisitions: the purchase of AI startup Celestial AI for approximately $3.25 billion in December 2025, aiming for $1 billion in annualized optical interconnect revenue by fiscal year 2029; and the acquisition of interconnect technology firm XConn for $540 million in January 2026.

IV. Strategic Catalyst: Nvidia $2 Billion Endorsement

At the end of March 2026, Nvidia announced a strategic partnership with Marvell Technology, including a $2 billion investment. Under the agreement, Marvell will provide XPUs and networking solutions compatible with Nvidia's NVLink Fusion rack platform, and the two companies will also collaborate on silicon photonics technology.

Nvidia CEO Jensen Huang stated, 'For customers seeking custom chips, they can now access our products and ecosystem through the partnership between Nvidia and Marvell.' This investment is more than just financial support; it is a powerful 'endorsement' from an AI industry leader.

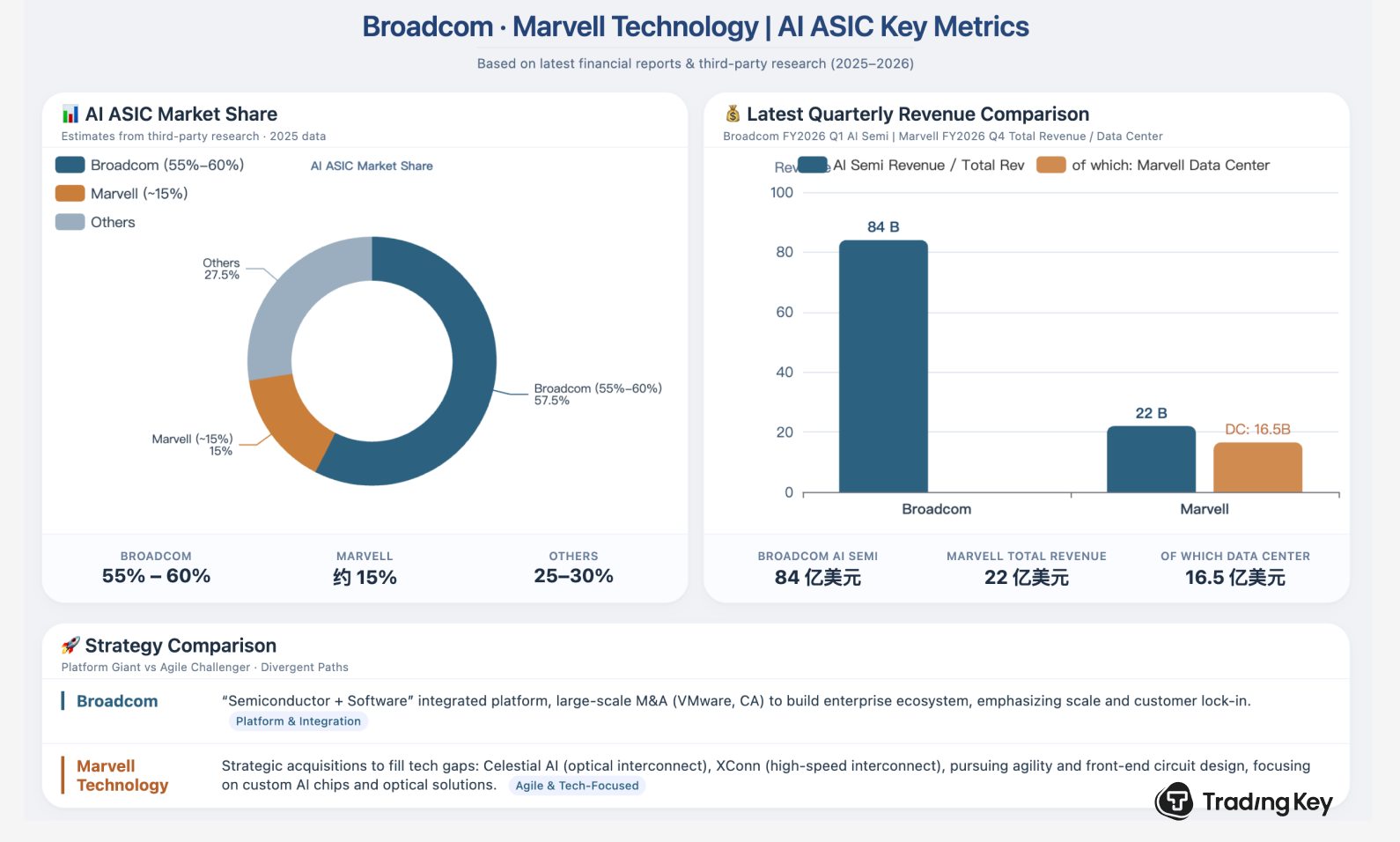

V. Comparison with Broadcom

Marvell and Broadcom are the top two players in the AI ASIC space, but there are significant differences in their market positions, customer structures, and strategies.

Dimension | Broadcom | Marvell Technology |

|---|---|---|

ASIC Market Share | Approximately 55%-60% (Estimated by third-party research reports; data based on 2025 projections) | Approximately 15% |

Latest Quarterly AI-Related Revenue | Quarterly AI semiconductor revenue of $8.4 billion (FY2026 Q1) | Total quarterly revenue of approximately $2.2 billion, with $1.65 billion from the data center business |

Customer Concentration | Diversified portfolio including Google, Meta, and ByteDance | Highly concentrated on Amazon AWS |

Development Strategy | "Semiconductor + Software" integrated platform, with large-scale M&A integration | Strategic acquisitions (Celestial AI, XConn), pursuing flexibility and front-end circuit design capabilities |

Broadcom's quarterly AI semiconductor revenue has reached $8.4 billion, nearly matching Marvell's total revenue for the entire fiscal year 2026 ($8.195 billion), representing a massive scale gap. However, Marvell is growing faster (42% annual growth), and its current valuation is more elastic than Broadcom's.

VI. Institutional Perspectives: Intensive Target Price Upgrades

In the past month, several institutions have issued positive evaluations of Marvell Technology. On April 9, Barclays upgraded its rating from "Hold" to "Overweight" due to growth prospects in optical interconnect and silicon photonics products, significantly raising its price target from $105 to $150; analyst Tom O'Malley stated that Marvell's optical networking revenue is poised for growth of up to 90% this year and next. Bank of America maintained its "Buy" rating on April 2, raising its target from $110 to $125. CITIC Securities maintained its "Buy" rating on March 10 with a $120 target, and JPMorgan reiterated its "Overweight" rating on March 3 with a $130 target. Based on consolidated institutional data, the average analyst price target for Marvell Technology is approximately $120.59, with a high of $164.

VII. Risks and Concerns

Despite its promising prospects, investors should remain mindful of the following risks:

- Customer concentration risk: Marvell is heavily reliant on Amazon AWS; any adjustment in AWS's capital expenditure cadence could significantly impact the company's revenue.

- Elevated valuation: The current trailing P/E ratio stands at approximately 41x, higher than the semiconductor industry average, suggesting the market has already priced in a portion of the optimistic outlook.

- Intensifying competition: Broadcom has set a long-term goal for AI chip-related revenue to exceed $100 billion, requiring Marvell to continuously expand its market share.

- Acquisition and integration risk: The integration of Celestial AI and XConn still requires time to be validated, and whether synergies can be realized remains a key variable.

VIII. Conclusion

Marvell Technology sits at the intersection of two high-growth tracks: AI ASICs and optical interconnects. Strategic investment from Nvidia, a flurry of rating upgrades from institutions like Barclays, and record-breaking financial performance have collectively driven a market re-rating of the company from a "chip supplier" to a "key player in AI infrastructure."

However, after a year-to-date rally of over 50%, future stock performance will depend heavily on execution—specifically whether the optical interconnect business can achieve explosive growth of over 90% and if custom AI chips can continue to expand their penetration among hyperscalers. While Broadcom has established a robust "dancing elephant" logic through its scale and diversified client base, Marvell plays the role of a "high-growth challenger." Earnings reports over the next few quarters will be the critical window to test the mettle of this dark horse.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.