INTU: QuickBooks Continues to be a Major Driver

Share Price (USD) | 779.61 | 2024 Revenue (USD) | 16.29bn |

Market Cap (USD) | 217.47bn | 2024 EPS adj. (USD) | 16.97 |

Listings | NASDAQ | Dividend Yield | 0.51% |

52-wk high/low (USD) | 790.61-632.64 | Target Price (USD) | 893.02-923.98 |

Source: TradingView

Investment Thesis

TradingKey - Intuit (INTU) stock had a great rally recently, being up 40% since April. We believe the company is not very cheap anymore. However, there is still an upside of 15% left, due to the good momentum of dominating the accounting software market for SMEs and expanding towards mid-market/ high-end customers with both QuickBooks and TurboTax.

Company Background

Intuit is a software company that provides financial management solutions for both individuals and businesses. It has two main solutions: 1) QuickBooks – the most widely used accounting software for small businesses and 2) TurboTax – tax preparation software for individuals and small businesses. These two products comprise the majority of the revenue generated, but there are also smaller products such as Credit Karma (credit insights) and MailChimp (marketing automation tool).

Revenue Breakdown

Intuit reports revenue in four segments:

- Small Business & Self-Employed (59% of the total revenue) – Consist of QuickBooks primarily and aiming at SMEs who want to manage their finances more effectively

- Consumer (27% of the total revenue) – Consist of TurboTax primarily, targets individual who want help with tax fillings; the segment is highly seasonal, with most of the revenue earned during the tax season

- ProTax (4% of the total revenue) – Set of products made for tax and accounting professionals

- Credit Karma (10% of the total revenue) – Various personal finance solutions

Geography-wise, Inuit remains highly concentrated in the United States, with 92% of the revenue generated there.

Market Share and Competition

Without a doubt, QuickBooks is dominating the accounting software industry with over 80% market share among SMEs, far ahead of the 2nd and the 3rd players – Xero and Saga 50.

Good news for QuickBooks is that only half of the SMEs in America use any kind of accounting software. Of the rest, 30% rely on Excel spreadsheets and 20% of the small businesses still use old-school paperwork. This provides a decent runaway for the company to further penetrate the SMEs segment. Not only this, but Intuit is also actively engaged in acquiring larger mid-market customers, as they have more purchasing power.

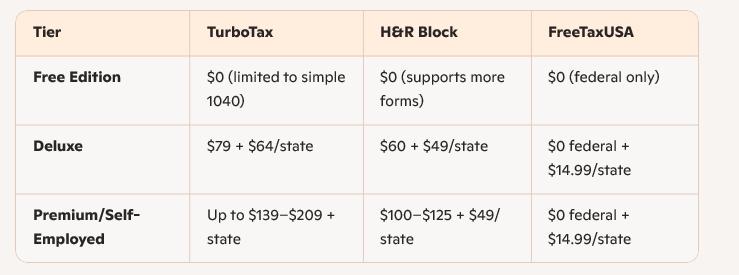

The situation for the other main product, TurboTax, is a bit different. There are quite a few other tax-filling software products on the market. Among them, TurboTax is among the priciest options, but they also provide smoother processing and friendlier interface.

Source: thecollegeinvestor.com

What’s common about these two services is that regardless of the economy, individuals and businesses still have to fill in accounting and tax forms, providing a certain level of downside cushion.

Growth Potential

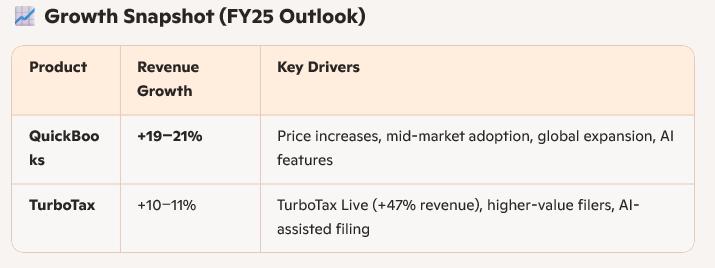

We believe growth will mostly come from the enterprise solutions and particularly QuickBooks. We expect the Small Business & Self-Employed segment (where QuickBooks is) will grow at a high teens in the coming years, driven by both user acquisition and price increases

QuickBooks already have the dominant market share and the most sophisticated product on the market, they just need to rely on the secular trend of more users switching from spreadsheets and paper to software, as well as the mid-market expansion.

The dominant market position will easily allow Intuit to increase prices mainly due to 1) clients not being able to easily switch to competitors (moving all the accounting books from QB to Xero will be quite a cumbersome process) and 2) the inclusion of more AI features within the product.

As for the TurboTax product we do expect less spectacular growth, despite the cheaper alternatives, Intuit is trying to focus on more high-end customers with its TurboTax Live – professional tax assistance which is more expensive than the basic TurboTax Online product which does not have this functionality.

Source: Intuit Investor Relations

Valuation

The stock is currently traded at 63x PE. Applying the discounted cash flow model, we came up with a target price of USD900 for INTU, a moderate 15% upside.

As mentioned above, we expect the growth will come primarily from QuickBooks, but this will come at the expense of margin limitation. QuickBooks is a relatively complex software product that requires maintenance and customer support, unlike TurboTax which is more standardized. As of 2024, the operating margin stands at 39% and we expect the coming years to reach not more than 41-42%.

All these implies an EPS growth of low to mid-teens, justifying the 15% upside.

Risks

Competition risks remain, but we believe they will not come from incumbent players but from potential entrance of the market from large fintech and payment companies – Visa, PayPal or Stripe, as they do have a rich amount of user data and technical capabilities to create such products.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.