Oracle’s AI Pivot Hits Overdrive

- Oracle’s IaaS revenue grew 52% YoY in Q4 FY25, with cloud consumption revenue surging 62% during the same period.

- Remaining performance obligations reached $138 billion, up 41% YoY, driven by strong demand and Cloud@Customer deployments growing 104%.

- CapEx hit $21.2 billion in FY25 and is projected to exceed $25 billion in FY26, focused on AI infrastructure.

- Oracle trades at 29x P/B (TTM), 740% above sector median, with forward EV/Sales at 10.4x, signaling extreme valuation premium.

Oracle’s (ORCL) FY2025 earnings and FY26 guidance present an interesting picture of a company in high-end transformation, from legacy software colossus to capital-intensive, vertically integrated AI infrastructure and cloud leader. Powered by 52% YoY growth in IaaS revenue and 62% cloud infrastructure consumption growth, Oracle is no longer transitioning; it is scaling its infrastructure moat and getting embedded at the bedrock level of enterprise AI. With cloud revenue during Q4 having peaked at $6.7 billion and remaining performance obligations (RPO) having increased by 41% to $138 billion, the company has reached the tipping point in enterprise demand.

But even with such headline wins, Oracle's stock, currently at $207.04, trades at levels that raise serious valuation doubts. Oracle now trades at an eye-watering 293% premium compared with the sector median basis for forward Price/Book and over 271% basis for EV/Sales (FWD), with its PEG GAAP ratio of 2.81. The overvaluation suggests an inevitable disconnect between optimism at the market level and pricing discipline. The question is no longer how Oracle would grow, but whether such a valuation model efficiently captures future cash flow generation amidst its reinvention phase with heavy capex and relative margin squeeze.

Source: Seeking Alpha, Stock Price Summary

The analysis that follows examines Oracle’s transformation, competition, and monetization playbook at the level of strategy, with forensic examination brought to valuation premium, cost structure, and sustainability. Here, what reveals itself is a nuanced picture: one of superb top-line growth powered by AI-infused infrastructure growth, but slowed by a valuation multiple stack increasingly disconnected from sector fundamentals. For investors, Oracle is a contradiction in motion, either at the doorstep of sustainable platform-scale repricing or overdue for an inevitable multiple reset with intensifying growth capital intensity.

From DATABASE TITAN to AI Infrastructure Behemoth

%20Market%20Size%202024%20to%202034.jpg)

Source: Precedence Research

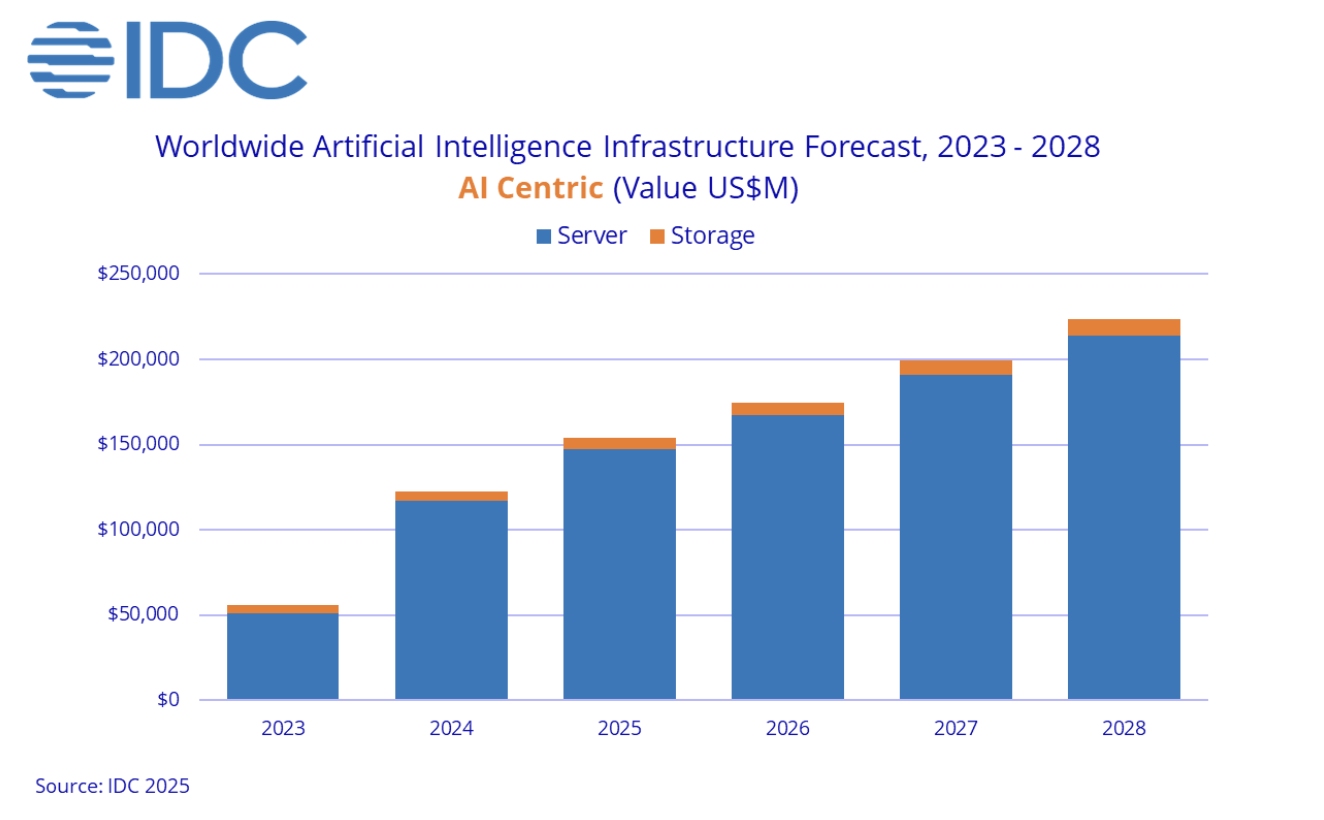

Oracle’s business model has experienced a seismic shift over the last five years. What was a historic software licensing and database company is now becoming an ever-more-converged infrastructure and AI platform company. Its dual-cloud approach, SaaS for enterprise applications and IaaS for compute and storage, now represents 42% of quarterly revenue and is growing at a combined 27% YoY. The truly remarkable aspect is infrastructure: OCI (Oracle Cloud Infrastructure) revenue grew 52% during Q4 2025, with cloud consumption revenue increasing 62%, led by the pick-up of demand from enterprise AI deployments.

Source: IDC

Oracle’s platform isn’t merely competing by cost or latency; it’s differentiated first by AI-native capabilities. The new Oracle 23 AI vector database makes enterprise data instantly compatible with LLMs with security retained, something most companies struggle to do at scale. That makes Oracle the default AI data layer by design among regulated and mission-critical industries such as healthcare, defense, and finance.

Oracle Cloud SaaS business is established within Fusion Cloud ERP and NetSuite, both having generated $1 billion in revenue during Q4 and increasing 18–22% YoY. They have incorporated AI agents and rising renewal rates but are vulnerable to saturation due to deeper vertical-specialized integrations by their rivals, for example, Workday, SAP, and Microsoft.

Concurrently, Oracle’s remaining performance obligations at $138 billion reflect not just strong future bookings but the strategic stickiness of the cloud footprint. That’s facilitated by Cloud@Customer deployments, private cloud deployments behind client firewalls, growing 104% YoY, that offer an exit ramp for hybrid clients moving their sensitive workloads increasingly into Oracle’s cloud model.

Challenging the Cloud Giants: Differentiation, Not Dominance

Oracle’s competitive landscape is defined by giants: Amazon’s AWS, Microsoft’s Azure, and Google Cloud control the hyperscaler space. But Oracle is creating a defensible niche with hybrid flexibility, privacy, and performance. Its differentiated approach, collimating together hyperscale-level scale with on-premises-level control, is stoking multi-cloud deployments that are up 115% QoQ. Oracle’s co-location model with AWS, Azure, and Google has spawned 23 multi-cloud regions, with 47 more planned. That suggests Oracle’s neither trying to displace hyperscalers nor just add one more cloud, but get embedded with them and become an integral part of customers with sovereignty data requirements and complex compliance requirements.

What differentiates Oracle from AWS and Azure isn’t breadth, but specialization. Oracle 23 AI’s vector database architecture is developed from the ground up as a native LLM backend with direct plug-and-play compatibility with no bulky ETL layers. That reduces latency, makes governance that much easier, and makes Oracle the high-integrity data provider for generative AI workloads.

But competition lurks on the horizon. Microsoft has embedded LLMs throughout Office 365 and Dynamics with the Azure OpenAI Service, creating a deeper productivity platform. Google Cloud is quickly ramping up verticalized solution stacks with its Vertex AI platform. Even lesser players such as Snowflake and Databricks are encroaching on Oracle’s data infrastructure space with cloud-native data stacks for AI optimization.

Short answer: Oracle’s differentiation is real, but so is competition risk. While the hyperscalers are going horizontal, Oracle’s bet is vertical, AI-based, and infrastructure-fueled. That helps it have clout in focused markets, but potentially less universal across all enterprise segments.

Growth with Weight: Operating Leverage and Capital Intensity Management

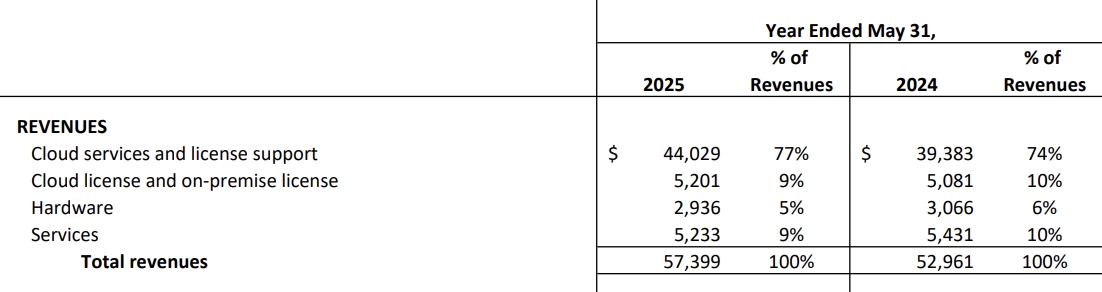

Oracle’s robust FY24 and FY25 quarters present an unlikely duo: net revenue growth and rising cash flow, alongside a rapidly expanding capital base. For the year, total revenues stood at $57.4 billion (8% YoY), with cloud services and license support at $44 billion (12%).

Source: Oracle Corporation, Q4 Financial Tables

Notably, annualized IaaS revenue now peaks at over $12 billion with participation from Autonomous Database at $2.6 billion annualized and AI consumption. Cash flow from operations came in at $20.8 billion during FY25, up 12%, a clear sign that the move by Oracle is not just about top-line growth but about monetization maturity. However, this robustness is offset by CapEx intensity. Oracle spent $21.2 billion on CapEx during FY25 and now projects the same for FY26 at $25+ billion, with the management themselves agreeing that such a figure could be too low. Most such spending is toward AI-optimized infrastructure along with rapid data center deployment, which is aligned with backlog-driven OCI growth.

.jpg)

Source: Oracle Corporation, Q4 Financial Tables

Profitability is solid but challenged. GAAP FY25 operating income was $17.7 billion (30.8% margin), and non-GAAP was $25.0 billion. GAAP EPS was $4.34, and non-GAAP EPS was $6.03. However, compared with the 72% YoY increase in forward P/E relative to sector median (according to the valuation snapshot), earnings growth lags behind price growth.

.jpg)

Source: Oracle Corporation, Q4 Financial Tables

Oracle's forward EV/EBITDA of 20x represents 35% above sector averages and forward EV/Sales at 10x, which is a 251% premium. This represents valuation drift that isn't entirely warranted by changes in cost structure or margin scalability. Oracle's multi-billion-dollar ramp-up of CapEx, even with backlog justification and cloud consumption, represents a risk of overextension should demand slow or hyperscaler competition escalate.

Scaling at the Edge of Risk: What Could Possibly Go Wrong?

While Oracle's cloud growth narrative is attractive, risks remain significant. Execution is most important: delivering 47 new multi-cloud regions and 30 Cloud@Customer deployments over 12 months entails high geopolitical and operating complexity. Management itself has conceded that supply lags demand, a harbinger of possible hardware procurement or site activation bottlenecks.

Second, CapEx intensity is comparable now with hyperscalers, but Oracle lacks their scale advantages. With $25+ billion of CapEx in the following year, ROI depends on continued demand by a small enterprise AI clique. Softness anywhere in demand could significantly compress ROI.

Third, valuation reset risk lurks over the stock. With Oracle trading at 200–700% premiums across different metrics, even modest earnings misses or macro shifts could trigger de-rating events. The distance between non-GAAP earnings and cash conversion deserves scrutiny, too, given increasing revenue conversion into usage-based OCI consumption.

Finally, the competitive landscape is unforgiving. Amazon and Microsoft are allowed to price-undercut or bundle their services, and new entrants like Snowflake offer cloud-native, more agile stacks for AI. Oracle’s differentiation is real; it must continually be proven by performance and product growth, however, to justify its model of valuation.

Conclusion

Oracle is no longer a legacy software giant; it’s becoming an AI-enhanced, high-performance cloud infrastructure platform. The makeover is working: demand is exploding, cloud revenue is accreting, and RPOs show sustained enterprise adoption. The market, though, may be pricing in a perfect execution bell curve that disregards margin variability, CapEx drag, and rising execution difficulty. For long-term holders, Oracle offers exposure to one of the most ambitious public-market AI-infrastructure overhauls, but one that now requires nuanced risk, return, and valuation assumption recalibration.

.png)

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.