Can Intel Out-perform the Market’s Doubts?

Key points:

- Intel reported $12.7 billion in Q1 revenue, with CCG down 8% and DCAI up 8% year over year.

- Intel Foundry Services revenue rose 7% year over year to $4.7 billion, positioning Intel as a CHIPS Act beneficiary.

- Non-GAAP operating margin was just 5.4%, with margins down 590 basis points due to underutilization and pricing strategy.

- Despite a forward P/E of 63.29, Intel trades at 0.84x price/book and 9.09x EV/EBITDA—well below peer averages.

- Intel cut 2025 CapEx guidance from $20B to $18B and reported -$3.68B free cash flow amid major transformation costs.

TradingKey - As Intel (INTC) undertakes one of the most pivotal turnaround plans in semiconductor history, the company sits at a precarious but promising inflection point.

Formerly the unchallenged leader of semiconductor manufacturing, Intel lost ground over the past decade to competitors like TSMC, AMD, and Nvidia. Yet today, Intel is executing a sweeping, multi-pronged transformation centered on future AI leadership, independence from external foundries, and national security initiatives.

With a cost structure reset, accelerated AI ambitions, and a laser-like focus on execution, Intel offers asymmetrical upside, albeit with significant execution and macroeconomic risks. Investors must weigh the slow-moving rebuild against the rising strategic importance of Intel’s products and foundry services within global AI and geopolitical trends.

Rebuilding the Core: Intel's Business Model and Competitive Advantage

Intel’s business is structured into two key segments: Intel Products and Intel Foundry. Intel Products includes the Client Computing Group (CCG), which reported $7.6 billion in quarterly revenue, down 8% year-over-year due to PC-market softness and share loss.

Source: Intel IR

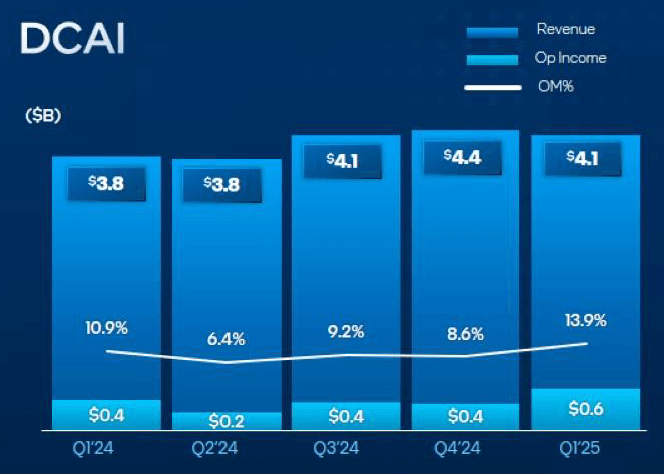

Meanwhile, the Data Center and AI (DCAI) division generated $4.1 billion in quarterly revenue, up 8% year-over-year as the Xeon 6 platform featuring Performance-cores (P-cores) gained traction.

Source: Intel IR

Worth noting is the fact that CCG and DCAI combined represent the lion's share of Intel’s $12.7 billion revenues in Q1.

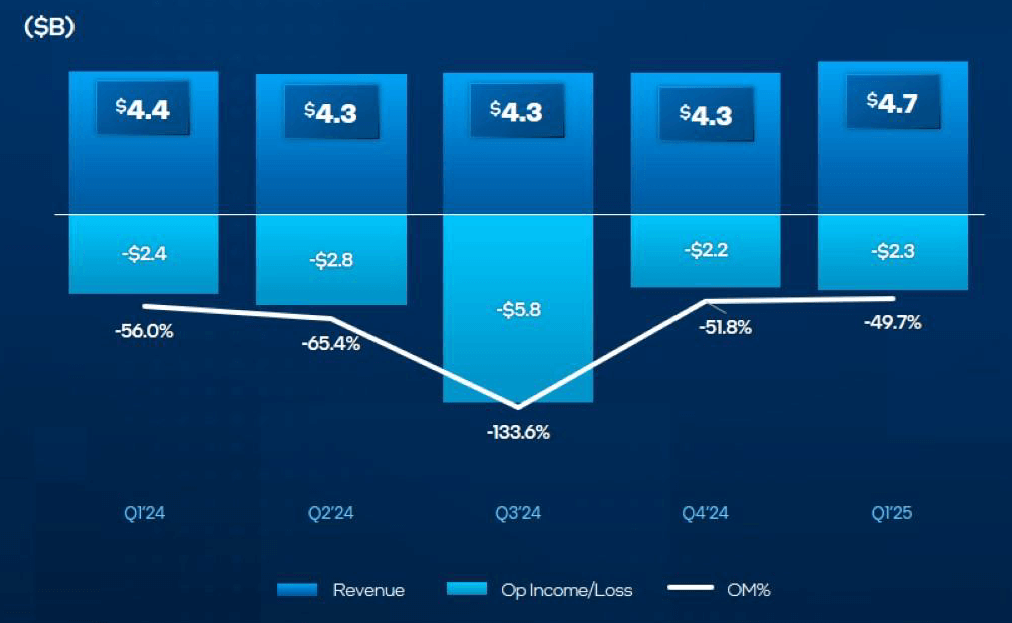

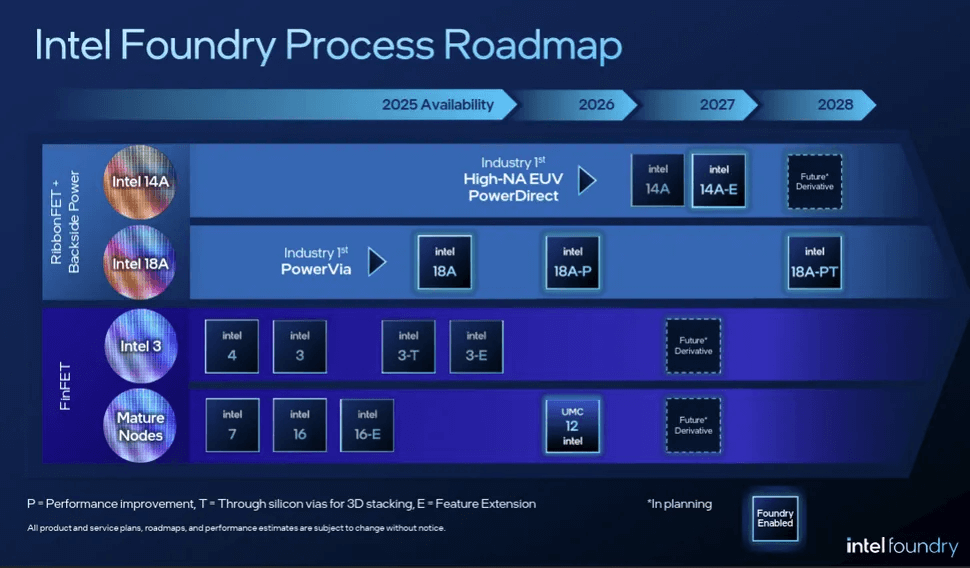

The real game-changer, however, is Intel Foundry Services (IFS), which reported $4.7 billion in revenue, up 7% year over year. Though still operating at a loss, IFS is gaining strategic weight through CHIPS Act alignment, AI hardware localization, and secure supply chain ambitions. Intel is ramping nodes like Intel 18A to become a leading foundry competitor to TSMC and Samsung by 2026.

Source: Intel IR

In AI, Intel’s differentiation is gaining early traction. The Xeon 6 P-core processors delivered a 1.9x improvement in AI inference throughput over the previous generations as measured by MLPerf benchmarks. This is a foundational, though not yet sufficient, step for competing against Nvidia and AMD in both training and inference workloads.

In contrast to short-term earnings volatility, Intel’s long-term model combines product and foundry offerings with deeper customer intimacy and more diverse revenue streams. The price of this transformation shows up as knife-edge operating margins (5.4% non-GAAP) and a tremendous reliance on execution on a very aggressive roadmap.

Climbing the Moat: Intel vs. Competition in the AI Age

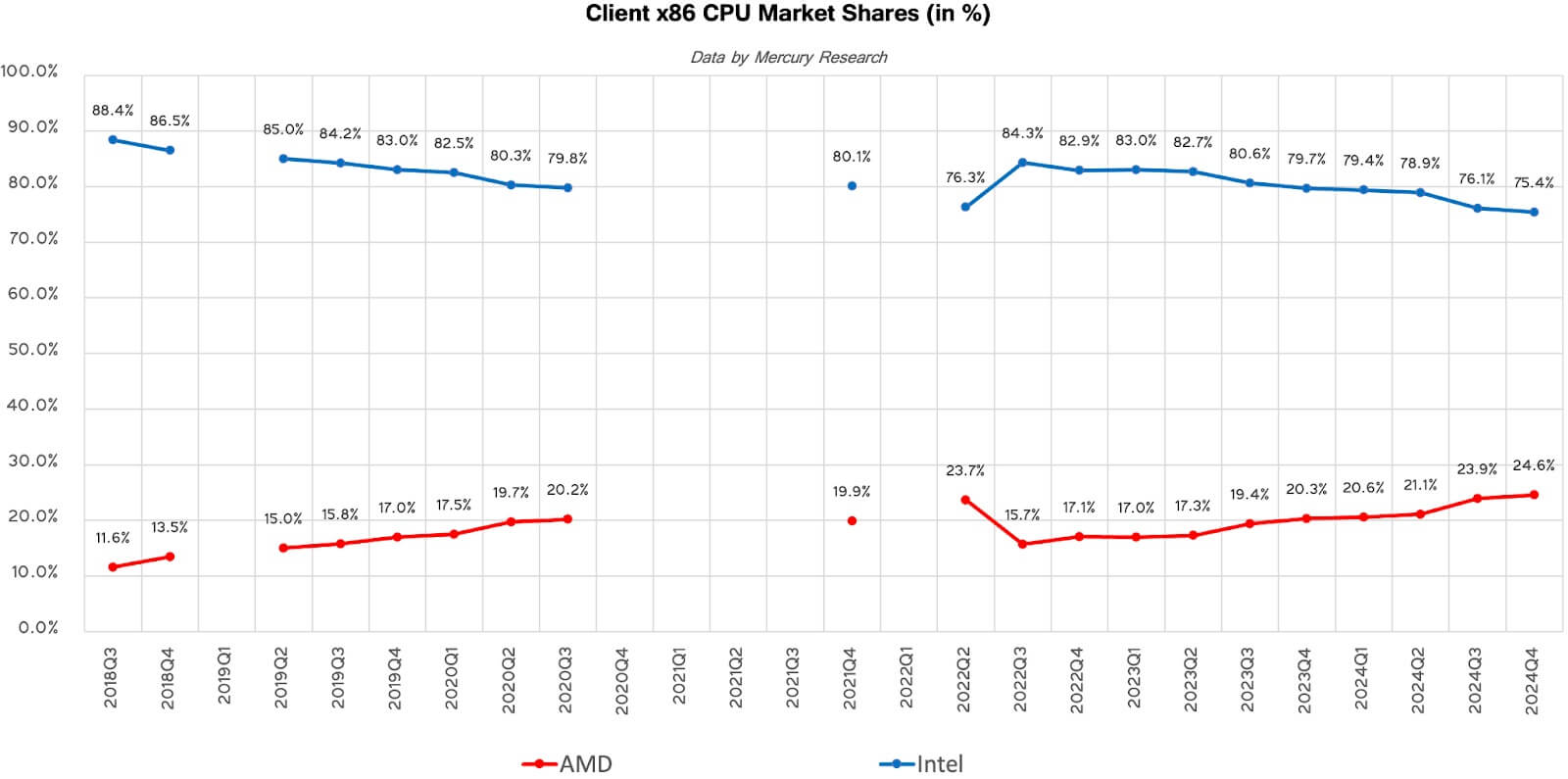

Intel competes fiercely on multiple fronts. In the PC segment, AMD dominates with its Ryzen CPUs, while Apple's silicon leadership puts x86 into question. In the data center, Nvidia leads AI compute leadership with its H100 GPUs and AMD is closing the gap with its EPYC chips that are optimized for cloud and AI workloads. TSMC remains the undisputed leader in advanced node manufacturing.

Source: Tom’s Hardware

But Intel's competitive story is changing. By vertically integrating IDM 2.0 and leaning heavily on foundry independence, Intel is differentiating on security dimensions of supply chain resilience and domestic production that competitors cannot easily match. That becomes an increasingly vital differentiator amid geopolitical tensions and government subsidies for chip independence.

However, margins remain under pressure. Non-GAAP profit margins declined 590 basis points year over year due to underutilization and aggressive pricing. Intel’s choice to underprice 18A for initial foundry customers is strategic, aiming to win volume and build trust that could pay off if scale and yield targets are met by 2026.

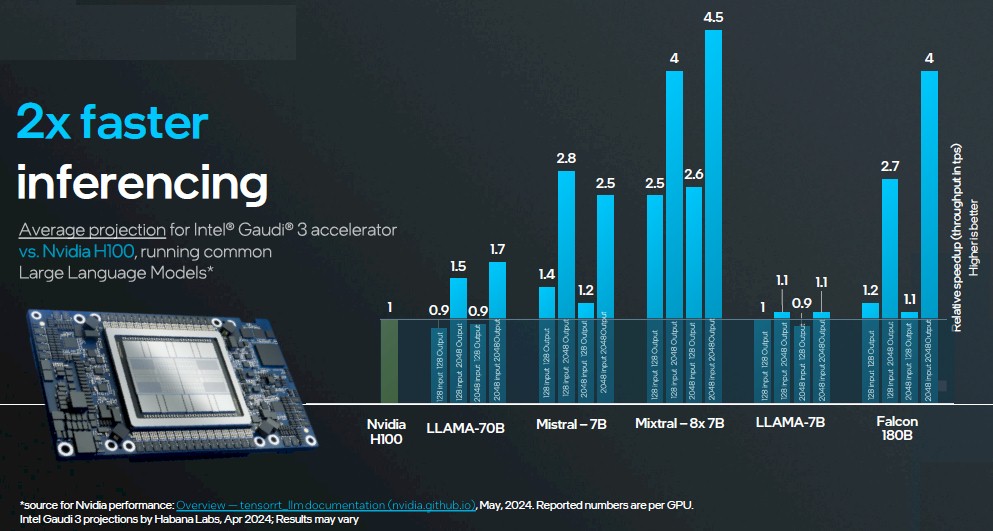

AI integration is both a battleground and a potential. Intel’s Gaudi accelerators target low-cost, power-efficient AI training markets as a differentiated alternative for companies that will not pay Nvidia premiums. Initial benchmarking indicates competitive price/performance ratios, though actual take-up is embryonic. Meanwhile, Intel’s mainstream Xeon base is positioned for AI inference upgrades as demand expands beyond high-end training.

Source: Next Platform

IFS customer acquisition is gaining momentum quietly. Intel reported cooperation with top U.S. hyperscalers as a significant step towards derisking its foundry scale-up. If Intel succeeds in getting stuck-term agreements from AI infrastructure players, it will close the competition differential over time against TSMC, not by being node-for-node equal overnight, but by winning on geopolitical and regulative dimensions.

Strategic Drivers & Financial Deep Dive: Cost-Cutting to Capital Discipline

Intel’s future hinges on three secular growth drivers: AI democratization, foundry diversification, and global chip manufacturing rebalancing. Management is reshaping the company to exploit all three.

Xeon, Gaudi, and IFS each serve distinct roles in this broader strategy. AI workload transitions create new cross-sell opportunities, with Xeon 6’s performance boost enabling more AI-capable servers. Gaudi may lag Nvidia in performance, but offers a compelling value proposition for businesses scaling AI affordably. Intel’s 18A node is vital to its foundry ambitions and is expected to be production-ready in late 2025.

Source: Intel Foundry

Financially, the turnaround was reflected in operating discipline. Non-GAAP operating expenses decreased 15% year over year, supported by cost-cutting through workforce reduction and flattening of management layers. Operating expenses, however, still account for 39.2% of revenue due to heavy R&D and manufacturing ramp costs.

Adjusted free cash flow remains negative at -$3.68 billion in Q1. Still, Intel reduced its 2025 CapEx guidance from $20 billion to $18 billion, targeting net CapEx of $8–11 billion. This move indicates a pivot toward asset-light execution and increased reliance on government incentives.

Customer retention holds steady in the CCG and DCAI businesses, though AI-related pressures are mounting. The move by Intel to divest a 51% stake in Altera to Silver Lake while holding on to 49% indicates a realistic strategy of keeping the key businesses while continuing to gain returns from programmable logic businesses going forward.

Strategically, Intel's restructuring to consolidate the Network and Edge Group within CCG and the DCAI is intended to improve accountability and align R&D priorities more sharply around AI and client-server convergence. Whether this accelerates the pace of innovation remains a watchpoint for 2025-2026.

Valuation: Uncovering the Intrinsic Signal Beneath the Macro Noise

Intel’s valuation presents a paradox. Although it sits at a steep premium on some forward earnings multiples, other multiples indicate deep undervaluation against its past norms and industry peers. Its forward P/E of 63.29 is 215% above the sector median and more than double its five-year average of 29.16. On the surface, this suggests overvaluation.

Such a distortion, though, stems not from irrational exuberance but from depressed near-term earnings as Intel invests significantly in its foundry growth as well as 18A node ramp. Intel’s heavy investment in 18A and foundry expansion distorts earnings while masking the long-term value of its strategic shifts.

When using enterprise-based metrics, the story changes. Intel’s EV/EBITDA forward multiple of 9.09 is 30% below the sector median, showing investors aren’t assigning value to future cash flows. Its price/book of 0.84 and price/cash flow of 8.73 not only fall meaningfully behind peers, but are also heavily discounted against Intel’s 5-year average, indicating already price-embedded pessimism.

This disconnect reveals potential upside. If Intel executes successfully on its cost controls and gains traction in AI and foundry, the prevailing price provides significant room to meaningfully expand multiples.

Essentially, Intel’s being priced as a legacy laggard, but if its transformation pays off, then perhaps Intel can be re-priced as a sovereign-grade chip manufacturing and AI infrastructure platform, supporting 30–50% upside over 18–24 months.

Risk Factor Audit: No Easy Roads to Recovery

The central risks surrounding Intel are daunting. The first of these is execution risk. Intel must achieve competitiveness with its 18A node by the end of 2025 or risk undermining its credibility as a viable alternative foundry. Even minor delays could extend the economics of scaling up its foundry operations by years.

Macroeconomic conditions also pose a heightened risk. Intel’s Q2 revenue guidance points to sequential declines, reflecting ongoing digestion of AI inventory and a slowdown in hyperscaler capital expenditure cycles. Prolonged weakness in end-market demand may extend periods of negative cash flow and delay the realization of operating leverage.

Source: Intel IR

Competition continues to intensify. AMD and Nvidia are not resting on their laurels; Nvidia’s Blackwell architecture, due later this year, may make AI performance gaps even bigger.

Capital efficiency is also a persisting threat. Intel’s foundry expansion and CapEx plans depend heavily on customer demand materializing as forecasted. Any shortfalls in uptake could severely impact returns on invested capital and weaken debt metrics.

Conclusion: Rebuilding at a High-Conviction for the Patient Investor

Intel’s turnaround is complex and far from guaranteed, but the upside is material. If it executes on 18A, scales foundry operations, and secures a meaningful slice of AI infrastructure, it may be revalued not as a legacy tech player, but as a national and strategic leader in semiconductor innovation.

For long-term investors with a tolerance for volatility and a focus on structural value, Intel offers high-conviction upside in a market that is still pricing it as yesterday’s news.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.