A Slice of Victory: Why Domino’s Has Won Investors’ Hearts and Appetites?

Key Takeaways

- Resilient Growth: Domino’s thrives on affordable fast food demand, making it a strong performer in economic downturns.

- Tech-Driven Moat: Its advanced digital operations boost efficiency, cut costs, and outpace competitors.

- Investor Appeal: High ROA, steady cash flow, and global expansion offer strong long-term investment potential.

Youth in a Pizza: A Warm Memory

TradingKey - Ten years ago, I was studying abroad with barely any money in my pocket. Domino’s promotional flyers were like manna from heaven: a large pizza for only $5, buy one get one free - a savior for broke students. I wasn’t interested in complicated pizza toppings, but Domino’s Cheese & Garlic Pizza left a deep impression after just one bite - a crispy crust, cheese and garlic like the smile of an old friend, simple yet satisfying. No other brand had that pure flavor; Domino’s became a warm memory in my youth. Later, I started researching the company and found it wasn’t just selling pizza but was a business that, with unwavering persistence over a decade, perfected simplicity.

Today, inflation runs wild like a runaway horse, while wages growth like turtles crawl, pushing consumers toward affordable fast food. This “lipstick effect” makes brands like Domino’s, McDonald’s, and Coca-Cola shine during economic winters. In the past, people might spend $50 at a high-end restaurant for a chef’s pizza; now, Domino’s deliciousness and affordability are the smarter choice. Next, I will take you through Domino’s success story and analyze why it’s a pizza worth biting into as an investment.

The Secret to Success: Perfecting Simplicity

Domino’s success can be summed up in one sentence: do simple things the best, day in and day out. From a small store on the brink of closure to the global pizza chain king, it relied not on flashy marketing but on honestly facing problems, technology-driven efficiency, and flexible market adaptation.

1. Sincere Rebirth: From “Cardboard Pizza” to Winning Customers’ Hearts

More than a decade ago, Domino’s hit a low point. Customers complained the pizza tasted like chewing cardboard, service was terrible, and brand trust nearly collapsed. In 2009, management did something bold: launched a pizza transformation campaign, putting customer complaints front and center, as if telling the world, “We messed up, but we will change.” They reformulated the crust, sauce, and cheese, introduced new flavors like cheese-stuffed crust, and shifted focus from a fanatical 30-minute delivery promise to balancing taste and efficiency. The result? Consumers were moved by this sincerity, and U.S. same-store sales grew at an average annual rate of 6% from 2010, with the brand rising like a phoenix.

This courage to face problems head-on is like a friend who admits mistakes and strives to improve, making you want to give it another chance. For investors, this shows Domino’s execution power and resilience: a company that can climb out of the valley can withstand future challenges.

2. Tech Magic: Making Pizza Fly to Your Door

Domino’s is not just a pizza store but a tech company in fast food disguise. It uses technology to turn ordering pizza into a silky smooth experience, with every step choreographed.

Open the Domino’s app, and the Pizza Tracker tells you the pizza is in the oven; ten minutes later, it’s on the delivery rider’s scooter. You don’t even need to bother ordering - the Zero Click app orders automatically in 10 seconds. Want to order via Alexa, smartwatch, or car system? No problem. Even sending a pizza emoji on X (Twitter) works! Domino’s app has over 15 million monthly active users, far surpassing Pizza Hut and Papa John’s, with user stickiness as strong as cheese pull.

Behind this is smarter operation. AI analyzes your ordering habits, predicts demand, optimizes inventory; average order completion time is just 22 minutes, with 90% of deliveries arriving within 30 minutes. Domino’s is testing drones and autonomous delivery, aiming for future low-cost delivery. Dynamic pricing, like discounts on rainy days, and the Domino’s Rewards membership system act like caring friends, giving you exclusive offers that keep you coming back.

For investors, technology is Domino’s moat. Its digital capabilities and efficiency not only make customers happy but also reduce costs and increase profits. Competitors can only envy this advantage.

3. Agility and Global Vision: Steady Progress

Domino’s culture is like a Silicon Valley startup: dare to try, dare to make mistakes, and dare to change. Employees can boldly suggest ideas, such as “emoji ordering” from internal innovation contests. Failed attempts, like AI voice ordering, are cut quickly, with resources swiftly redirected. Flat management lets store feedback reach headquarters directly, with decisions as fast as a delivery rider sprinting.

In global expansion, Domino’s is a smart traveler, carrying a standardized backpack and a localized map. Global stores use the unified PULSE system to ensure consistent quality; in India, they offer vegetarian pizzas catering to religious habits; in China, they serve crayfish and spicy flavors to capture local tastes. International markets, Asia and Europe become new growth engines. Despite trade wars and geopolitical pressures, localization strategies root Domino’s firmly worldwide. With Europe’s economy possibly recovering in 2025 due to interest rate cuts, international revenue is expected to accelerate.

For investors, this agile culture and globalization are dual engines: a stable core model plus flexible growth space.

“Hungry for More”: A Multi-Channel Growth Engine

Domino’s “Hungry for More” strategy is a precise offensive, advancing on multiple fronts. It partners with Uber Eats to attract new customers; DoorDash, expected to launch in late 2025, will bring more traffic. Meanwhile, Domino’s app, with real-time route tracking and a smooth experience, crushes competitors in monthly active users. In China, Domino’s is the only pizza brand promising 30-minute delivery across all channels; if late by a minute, customers get a free 9-inch pizza coupon. 90% of orders arrive on time, like a friend who never breaks promises.

This multi-channel approach is like opening several windows during an economic winter: third-party platforms bring new customers, the app retains old ones, working together like cheese and crust. For investors, this means lower customer acquisition cost and stronger brand loyalty. Especially when consumers seek value, Domino’s rides the wave.

Financial Code: Investment Brilliance in Steady Numbers

Market Position: The King’s Confidence

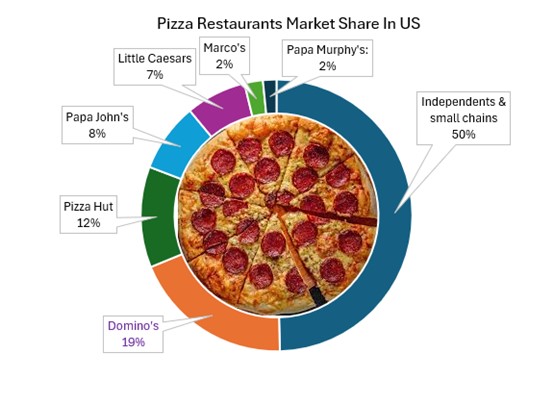

Domino’s is the clear global leader in pizza, holding about 20% of the U.S. pizza market, well ahead of Pizza Hut (12%) and Papa John’s (8%).

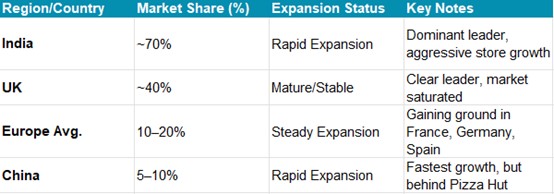

International markets provide diversification and shield the company from single-market risks. The brand dominates India with a 70% market share in organized pizza, leads the UK with 40% in delivery pizza, and is steadily expanding across continental Europe with 10–20% share.

In China, Domino’s is rapidly gaining ground, holding 5–10% of the pizza delivery market and accounting for about 13% of global revenue in 2024-making it the company’s fastest-growing major market.

Source: HubSpot, TradingKey

Source: Jubilant FoodWorks, Domino’s, Euromonitor, Statista, Yum China

Profit Margin: The Fruit of Efficiency

Domino’s operating margin reached 19%, higher than Pizza Hut’s 15% and Papa John’s 12%, thanks to an efficient supply chain and digital operations. For investors, a high margin means greater return potential.

Source: Company Financials, TradingKey

ROA and Valuation: Buffett’s Half-Court?

Domino’s trailing twelve months (TTM) ROA stands at an impressive 33%, reflecting its ability to generate strong profits from a relatively small asset base typical of asset-light, franchised fast-food companies. While high ROA is common in this business model, Domino’s ROA notably exceeds competitors like Yum! Brands (around 24%) and McDonald’s (around 16%), highlighting its superior operational efficiency. Warren Buffett favors firms with high ROA because it signals efficient asset use and steady cash flow, both of which Domino’s demonstrates consistently in the fast-food sector.

However, Domino’s TTM P/E is about 28, well above Buffett’s traditional preference for below 15. The high P/E reflects market optimism about growth but may make Buffett hesitant. Yet Buffett has shown flexibility recently with high-growth, wide-moat companies like Apple. If he sees Domino’s tech moat and globalization potential, he might bite, despite the premium valuation.

The Truth About Negative Shareholder’s Equity

Domino’s shareholder’s equity is negative (around -$4 billion) due to aggressive stock buybacks and dividends, not operating losses. Annual $250 million buybacks are expected to boost 2025 EPS by 6%. Debt supports buybacks and dividends, with a leverage ratio of about 5x. This high leverage is common in U.S. stocks but requires caution amid rising interest rates.

Don’t be scared by negative shareholder’s equity. Domino’s free cash flow (FCF) flows steadily, easily covering buybacks and dividends. This shows the business is as solid as its 30-minute delivery promise. For long-term investors, this generous shareholder return model plus strong cash flow makes Domino’s a buy-and-hold for a decade.

.png)

Source: Company Financials, TradingKey

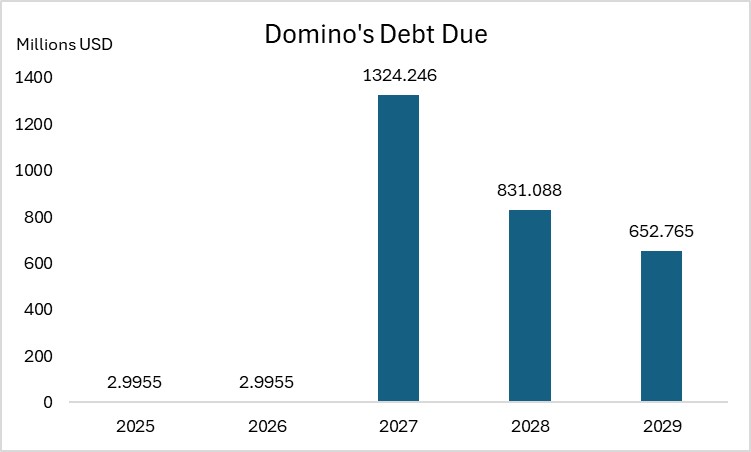

Domino’s faces relatively low debt repayments in 2025 and 2026, with only about $3 million due each year, making these periods manageable and not very stressful in terms of debt obligations. However, 2027 marks a significant peak, with approximately $1.324 billion in long-term debt maturing, representing a substantial repayment challenge. This large upcoming maturity will require careful financial planning to ensure sufficient liquidity and refinancing options are in place to meet the obligation without disrupting operations.

Source: Company Financials, TradingKey

Owned Stores and Supply Chain: The Behind-the-Scenes Pillars

Domino’s U.S. owned stores dropped from 577 in 2003 to about 294 now, accounting for only 8% of revenue, but they’re far from decorative. They serve as labs for testing new tech and marketing strategies; schools for training managers and franchisees; and bridges helping HQ understand franchisee challenges. These roles smooth franchise operations and stabilize expansion.

Source: Company Financials, TradingKey

Supply chain operations (U.S. and Canada) contribute two-thirds of revenue and one-third of profit but could be outsourced. This shows Domino’s core is not stores or supply chain but a brand and tech-driven system. Domino’s China is run by an independent franchisee with strategic alignment but local autonomy on flavors and promotions, enabling smooth global market navigation.

Source: Company Financials, TradingKey

Investment Logic: Why Take a Bite of Domino’s?

Domino’s success stems from focus on delivery, experience optimization, and continuous innovation. Its brand core is simplicity, efficiency, and technology - like a freshly baked pizza, aromatic and worthy of savoring. Reasons to invest are clear:

- Lipstick Effect: Affordable fast food demand rises in economic downturns; Domino’s is a winner.

- High ROA: Efficient asset use and stable cash flow, a value investor’s favorite.

- Global Growth Potential: Asia and Europe markets still have room to grow.

- Tech Moat: Digitalization and AI leave competitors behind.

Risks to watch:

- High P/E: A 28x P/E may deter conservative value investors.

- High Leverage: Rising interest rates could increase debt pressure.

- Competitive Pressure: Third-party platforms may siphon profits.

- International Risks: Trade tensions, currency fluctuations, and local policies add uncertainty.

Epilogue: A Pizza’s Lesson

Ten years ago, that $5 Cheese & Garlic Pizza was not only my lifeline but a symbol of Domino’s commitment to simplicity. From a small store to a global pizza empire, it proves that perfecting simplicity makes you king. For investors, Domino’s steady cash flow, high ROA, and global potential are like a hot pizza - tempting and reliable. Even if its P/E makes Buffett frown, for those willing to accept a premium, this pizza is worth a bite, to slowly savor its future.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.