[IN-DEPTH ANALYSIS] Eaton (ETN): The Grid King with AI Sword and MAGA Shield

Source: TradingView

Key Points

- By leveraging MAGA(Make-America-Great-Again) manufacturing reshoring and Biden's infrastructure bill, Eaton has built a cost moat through "local procurement + policy subsidies".

- With a 30% share in the North American data center UPS market, Eaton deeply integrates its power grid equipment with AI computing infrastructure, capturing the explosive demand of data centers.

- Despite short-term tariff pains, the long-term "new oil of power" logic remains intact, as continued order growth and a 25% upside potential at a 26x PE ratio underscore its resilience.

The "US National Project" in Eaton’s Balance Sheet

TradingKey - By the rusty shores of Lake Erie, Eaton (NYSE: ETN) pulled off a move slick in 2012. It stashed its tax papers in Dublin's lucky drawers but kept its beating heart in Cleveland's steel ribs, which is a city once synonymous with steel and smokestacks now pulsing with the algorithms of smart grids.

Here, in the silent hum of transformers and the flicker of data center LEDs, Eaton has a business portfolio that is like a precise power Lego set: building the invisible highways of electricity that power everything from TikTok servers to F-35 fighter jets, all while balancing the tempo of EV innovation with the glacial patience of grid modernization. Behind this equilibrium lie three distinct yet interlocking business gears:

Source:Eaton

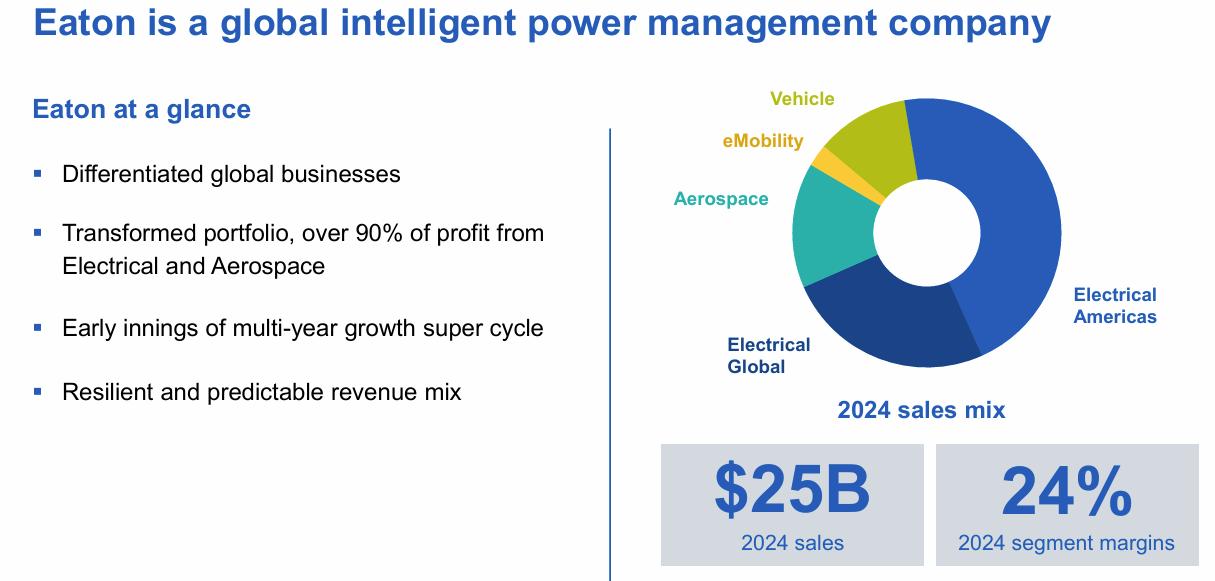

1) Electrical Business: In the field of smart grids, the company holds a 30% share in the North American data center UPS market. In 2024 it accounted for 70% of the revenue. The American market has benefited from the upgrade of data centers and power grids, with an organic growth of 17%. Amazon, Microsoft, Meta, Alphabet and TikTok, these companies have become key customers of Eaton's power management solutions due to their large-scale expansion of AI data centers.

2) Aerospace accounts for 15% of its revenue. The operating profit margin reached a record of 24% in 2024, benefiting from the recovery of commercial aviation and the growth of defense orders(+14% YoY). Eaton's aviation business stems from its strategic mergers and acquisitions and industrial diversification layout. The capital market is more concerned about its potential growth in the fields of electric aircraft (eVTOL) and military drones.

3) Vehicle and eMobility: The traditional vehicle business accounts for 11% of revenue, down 2% YoY due to cost pressure. The eMobility accounts for 3%, up 30% YoY, and the profit margin is higher. Although the aviation and eMobility businesses seem independent, there are deep synergies between the two in terms of the application of intelligent technologies and supply chain management.

The Linchpin of MAGA's Industrial Revival

Eaton, with its transformers and smart grid technologies, holds a core supplier position in "Infrastructure Investment and Jobs Act" (BIL). In the "manufacturing reshoring" policy continuously strengthened by the Trump administration, Eaton has optimized costs through policy provisions such as the reduction of corporate income tax, clean energy subsidies, and accelerated capital depreciation. For example, the federal subsidy obtained by the new plant in South Carolina has reduced the cost of each 500-kV transformer by 15%, which forms a double leverage with the tax incentives for domestic procurement in the IRA Act.

When the Biden administration enforces that charging piles must meet the power standard of 150 kW or more, the market share of Eaton's eMobility business has soared from 12% to 28%, building a "power tariff wall" with the NEVI certification. The essence of the MAGA movement is the spatial reset of the supply chain and geo-economics. This violent cutting of the supply chain rewrites the global industrial network into a "North American power local area network", and Eaton is the DNS server of this local area network.

Eaton’s AI Sword Unsheathed

In Q1 of 2025, the backlog of orders for Eaton's power transmission equipment reached $11.7 billion, which is 1.5 times the annual revenue of this sector in 2024. This "receiving payment before delivery" business model reflects the urgency of the upgrade of the US power grid: the delivery cycle of transformers has been extended from 3 months to 2 years, and the price of power distribution equipment has skyrocketed by 68% in two years. The revenue growth rate of Eaton's American electrical business is as high as 14%.

Source:Eaton

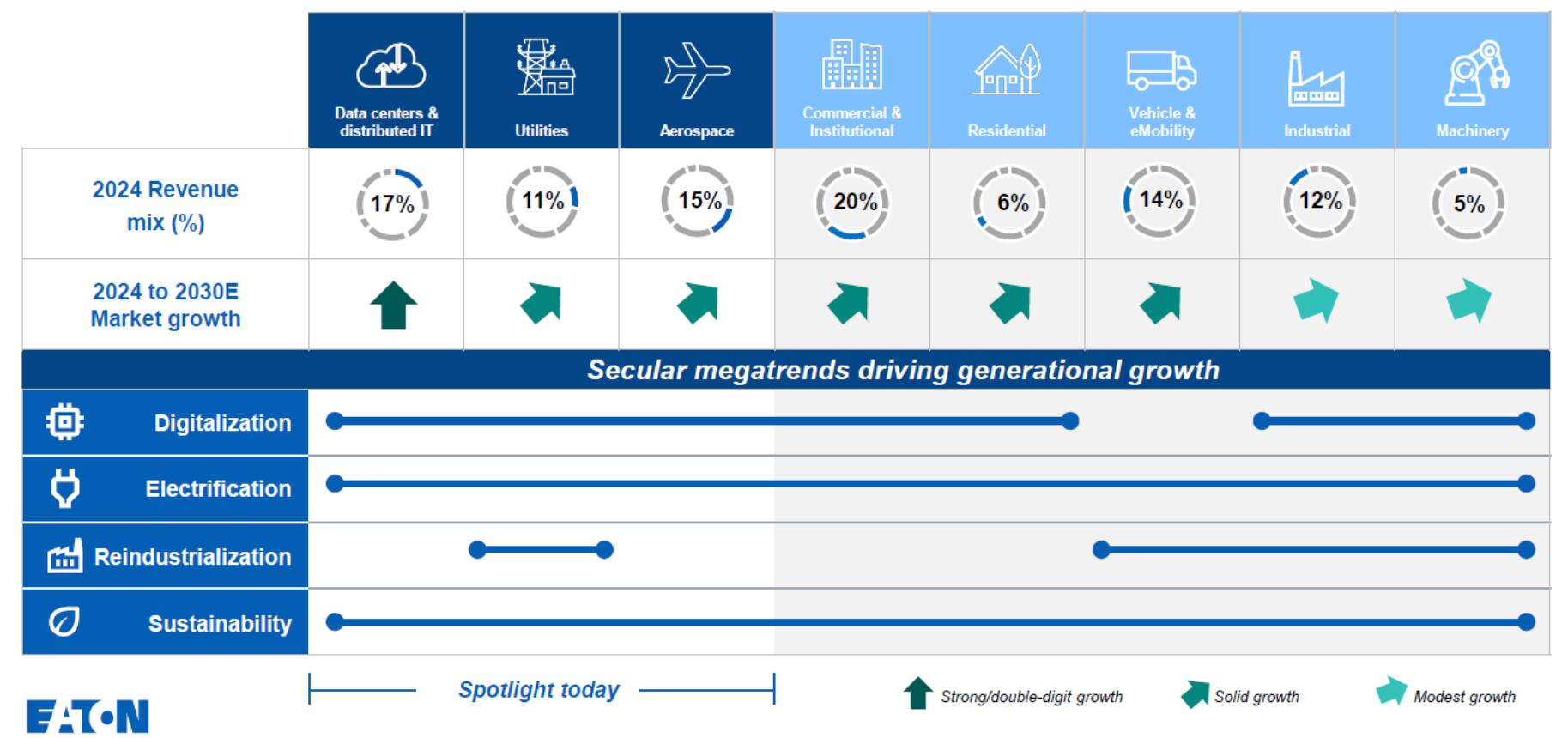

With a set of growth data like a strategic compass, Eaton has outlined a core revenue growth blueprint of 6% - 9% annually before 2030. The main engines driving profit growth include digitization, electrification, and re-industrialization. Among them, the CAGR of data centers and distributed IT businesses grows by more than 16%, and the CAGR of power and industrial equipment also increases at around 7%.

Eaton's case reveals a deep logic: in the double revolution of digitization and carbon neutrality, power infrastructure may become the "new oil" of national competitiveness. The new industrial narrative written by Eaton in its financial statements goes beyond the individual enterprise and empty political slogans. In this era, the American Dream is no longer the muscle memory on the assembly line, but perhaps the binary data beating in the intelligent power distribution cabinet.

The Battle of the Old and New Continents

In the market competition of power transmission equipment, Hitachi-ABB, Siemens, GE, and Schneider Electric have long occupied the top four positions. Eaton, with a global market share of fifth (about 9%), has built an unshakable moat on the North American continent with its unique strategic resilience.

When European giants are advancing rapidly in the field of ultra- high-voltage direct - current transmission, Eaton has chosen a more pragmatic path-compressing the response speed of intelligent power distribution cabinets to 4 milliseconds and using the IRA Act subsidies to push the profit margin of energy storage systems to 42%, enabling it to form a technical monopoly in scenarios such as North American data centers and new energy power stations.

Source:Market Research Intellect

Facing the low-price offensive of China's TBEA and XD Group, Eaton is driven by the "North American localization + high-value-added" dual wheels: doubling the transformer production capacity of the Texas factory, switching the copper procurement to the Montana mine to enjoy a subsidy of $150 per ton, and the 15% premium of the intelligent power distribution cabinet is exactly the commercial value exchanged by the technical barrier. Moreover, in the Red Sea New City project in Saudi Arabia, its packaged solution of smart grid + energy storage crushes its Chinese opponents with the advantage of the full-life-cycle cost.

Financials and Valuation

For the financial parts, Eaton's revenue and gross profit margin are growing rapidly, and the EPS growth rate is over 18% YoY, which is significantly benefited from the upgrade of the North American power grid and the double - wheel drive of the data center power solution (AI - driven growth of 75%) and the new energy transformation. The management expects that the proportion of high gross margin orders will increase in 2025, and the share of the American business will be consolidated under the influence of the tariff policy, which is expected to maintain a high growth rate over 15%. asset-liability ratio is 52.69%, which is within a controllable range. The company's free cash flow is as high as $3.5 billion, which supports the acquisition of Fibrebond and begins to increase Eaton’s profits in Q3. Eaton continuous increase in stock repurchases (exceeding $2 billion) over the next two years, which shows its emphasis on shareholder returns.

Trump's "reciprocal tariff" has a "short-term negative and long-term positive" impact on Eaton. In the short term, the cost pressure suppresses profits, but in the medium and long term, the expansion of domestic demand and policy dividends will dominate the growth. If the United States finally imposes a 25% tariff on Chilean copper, resulting in an 8% - 10% increase in the raw material cost, Eaton can partially offset the tariff cost by enjoying the IRA subsidy ($150 per ton) and tax credits through local procurement. The impact of the tariff only turns the 2 pct or more YoY growth of Eaton's profit margin into a stable stage. Coupled with the support of the US reshoring policy and the demand for AI data centers, the return of manufacturing is still expected to bring an additional 5 pct order growth rate (reaching 25%).

Eaton's current dynamic PE valuation is 26x, slightly higher than that of Schneider (25x) and ABB (20.5x). It is expected that the data center + energy storage business will maintain a CAGR growth rate of 25% in the next five years, and if the IRA policy continues, Eaton's valuation would likely be raised to 30x PE. Coupled with the high profit growth, Eaton still has a potential appreciation space of about 25% in this year, compared with the current price of $290.

Ticker | ETN | ABBNY | SBGSY | EMR | WEGZY |

Company Name | Eaton Corporation | ABB Ltd | Schneider Electric S.E. | Emerson Electric Co. | WEG S.A. |

Gross Profit Margin | 38.20% | 38.16% | 42.64% | 52.44% | 33.73% |

EBIT Margin | 18.78% | 17.48% | 17.10% | 18.07% | 20.22% |

Net Income Margin | 15.25% | 12.55% | 11.19% | 13.74% | 15.91% |

ROE | 20.20% | 30.16% | 15.19% | 7.70% | 30.84% |

Dividend Yield (TTM) | 1.34% | 1.89% | 1.52% | 2.00% | - |

Revenue Growth (YoY) | 7.25% | 2.07% | 6.27% | 10.31% | 16.87% |

EBITDA 3 Year (CAGR) | 17.72% | 11.67% | 11.43% | 7.86% | 25.70% |

EBIT 3 Year (CAGR) | 23.07% | 14.24% | 12.86% | 2.18% | 26.54% |

Net Income 3 Year (CAGR) | 20.96% | -3.85% | 10.04% | -4.34% | 19.00% |

EPS Growth Diluted (YoY) | 18.45% | 14.88% | 6.51% | -4.10% | 5.43% |

P/E GAAP (FWD) | 26.19 | 20.57 | 25.32 | 23.67 | 25.98 |

EV/EBITDA (FWD) | 18.79 | 14.48 | 14.62 | 14.16 | 20.32 |

Price to Book (TTM) | 6.14 | 7.08 | 4.4 | 2.9 | 10.25 |

Source: TradingKey, Refinitiv, as of the latest financial reports and trading date

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.