Citi’s Quiet Reinvention: Resilience Over Hype

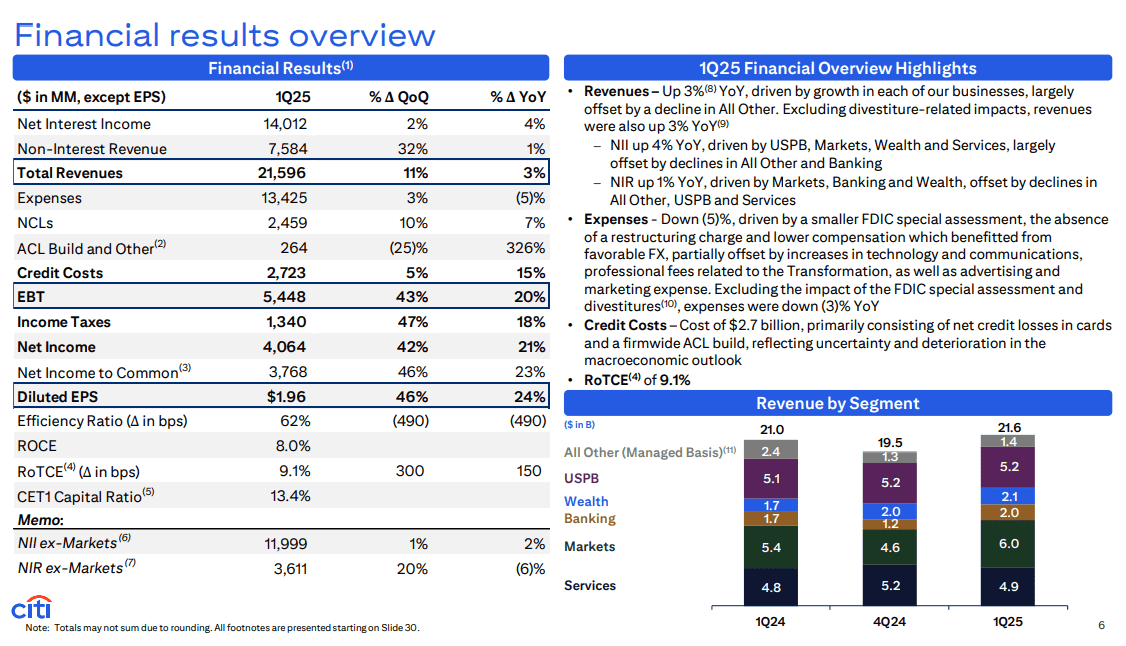

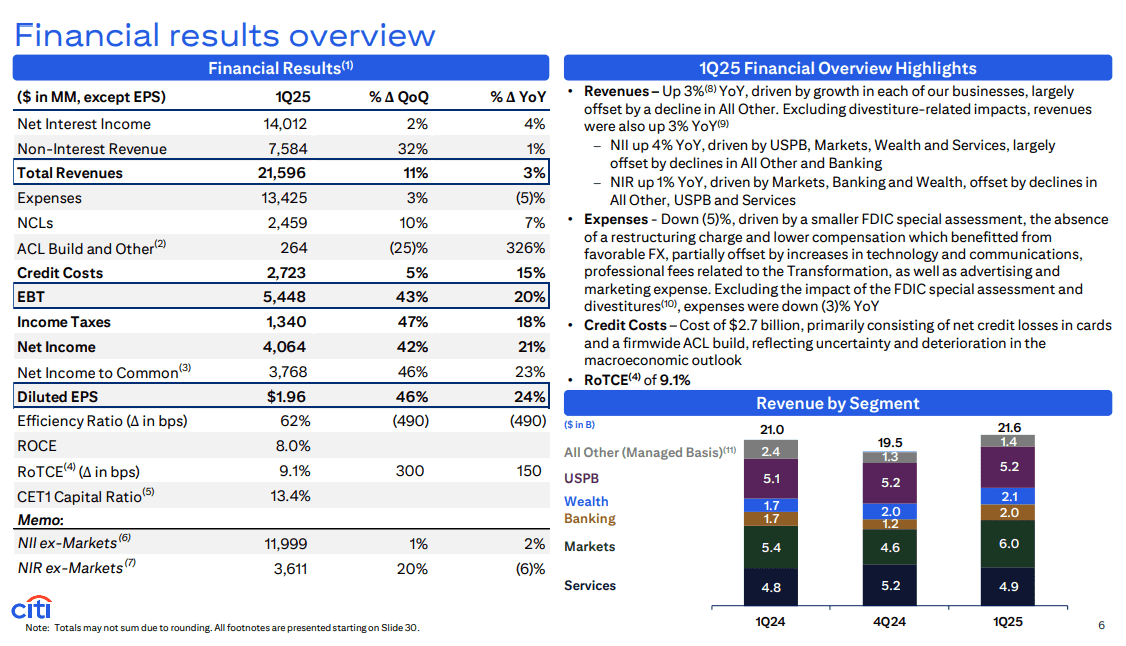

- Citigroup reported Q1 2025 net income of $4.1 billion, up 21% YoY, with RoTCE improving to 9.1%.

- Services generated $4.9 billion in revenue with a 26.2% RoTCE, while Wealth revenues surged 24% YoY.

- Citi trades at 0.6x tangible book value, indicating ~50% upside based on a fair value range of $91–$101.

- Total credit costs rose 15% to $2.7 billion, but CET1 ratio stayed strong at 13.4% with stable asset quality.

TradingKey - In the hypercompetitive landscape of the banks, Citigroup (C) is redefining itself, not with splashy transactions, but through measured reorganization, strategic separations, and a reenergized digital framework. Reporting total first-quarter 2025 income of $4.1 billion, up 21% from last year, and tangible gains within its five main businesses, Citi is forging itself from a bloated multinational into a lean, high-capacity banking organization.

Fundamental to Citi’s strategic value proposition is its distinctive global franchise, now one of the world’s few remaining international banking systems, coupled with targeted integration across institutional businesses, personal banking, and wealth management. But below the surface, something even more powerful is happening: a low-key artificial intelligence revolution, simplification of its technology stack, and infrastructure changes that can be scaled up, now beginning to provide operating leverage as well as greater return.

The transformation here is not so much about top-line bang as it is about earnings resilience, margin quality, and capital effectiveness. Citi’s RoTCE climbed 150 basis points year over year to 9.1% this quarter, while its efficiency ratio rose by virtually 500 basis points to 62%. In a world where return on equity tends to depend so much on macro currents, Citi’s internal self-improvement might be its long game.

Source: Q1 Deck

Disassembling the Engine: Strengths of Core Business Operations and Competitive Advantage

Citi’s expansive architecture has frequently been a double-edged sword, though, during Q1 2025, all of its five main businesses reported resilient performances that demonstrate a matured simplification strategy. Services, its most productive and return-intensive segment, generated $4.9 billion of revenue, up 3% YoY, on a spectacular 26.2% RoTCE. Treasury and Trade Solutions (TTS), integrated within Services, recorded further market share gains, with 8% growth in USD clearing volume and 5% in cross-border value of transactions. Services had a 5% increase in year-on-year net interest income, driven by better deposit spreads and volume growth.

Markets, traditionally a volatile business, were a positive factor for the quarter, with revenues climbing 12% to $6 billion. Fixed Income gained 8% on client activity within rates and spread products, while Equity markets rose 23% on derivatives and Prime momentum. Prime balances gained 16%, reflecting greater client entrenchment. With a RoTCE of 14.3%, Markets is now a stabilizing factor, not a cyclical swing component.

Wealth, a tier that Citi is looking to scale, produced a 24% YoY revenue increase and cemented momentum across all three client segments. U.S. Personal Banking (USPB) recorded modest 2% growth, while Branded Cards led the charge, fueled by higher net interest margins as well as new customer features such as Flex Pay through Apple Pay. Bank-wide, the company is rolling out Gen AI aggressively across the board, from risk monitoring through automated code reviews, representing a shift toward scalable productivity improvements.

Source: Q1 Deck

Going Against the Tide: Citi's Advantage in a Competitive Market

Citi’s competitive positioning is located where scale, digitization, and institutional depth converge. In Services, it remains the leader of cross-border transaction flows, retaining the #1 spot in direct custody and adding 65bps of TTS market share year over year. This moat, based on regulation familiarity, cross-border capabilities, and client infrastructure embedded within, is still challenging for fintechs, even for regional banks, to emulate.

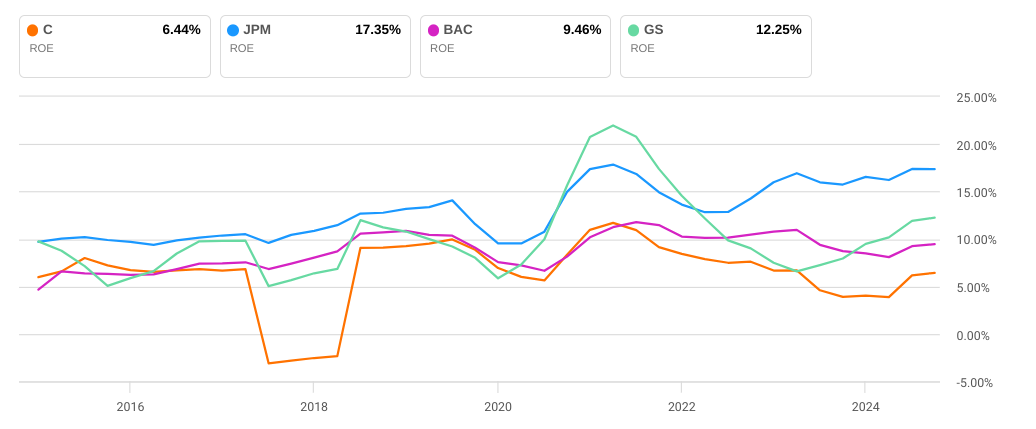

Compared with peers JPMorgan Chase and Bank of America, Citi trails peers on profitability metrics including ROCE and multiples of the earnings per share, though it is quickly closing the gap through cost normalizing and business exits. In contrast with JPMorgan, set aggressively for consumer scale, or Goldman Sachs, set skewed toward advisory and trading, Citi is constructing a hybrid platform: retail enough to be sticky, institutional enough to scale.

Significantly, integration of AI is starting to gain real momentum. Citi’s internal transformation has phased out more than 130 legacy applications in Q1 alone, substantially enhancing cost and risk control. Its strategic partnership with Palantir for modernization of onboarding and real-time analytics in Wealth indicates a shift toward intelligent, not merely larger, operations. In Markets and Services, Gen AI-driven developer tools and automated trade surveillance are reducing operational friction and making processes flow more seamlessly, Citi is not only catching up, it’s innovating stealthily.

Source: SeekingAlpha

Growth Drivers and Financial Foundations: The Turnaround Taking Place

The actual narrative for shareholders is Citi’s shift towards positive operating leverage. Three consecutive quarters of leverage, plus Q1 2025 revenues up 3% YoY, are disrupting Citi’s past pattern of cost-heavy structures coupled with unimpressive margin execution. Operating expenses declined 5% year over year, thanks to the absence of FDIC assessments as well as a decline in severance, as technology investments and marketing rose as a part of strategic growth.

The company’s $21.6 billion of revenues during the quarter comprised a 4% increase in net interest income as well as a 1% increase in non-interest revenues. The latter is set to reaccelerate within Banking and Wealth as M&A advisory picks up, as well as fee-based AUM compounds. Investment Banking fees rose 14%, while advisory rose 84%, reflecting a strong pipeline for strategic mandates.

The credit quality is one of concern. Total credit cost increased by 15% to $2.7 billion, primarily due to card-driven net credit losses as well as ACL builds, underpinned by macro uncertainty. Nevertheless, Citi’s ACL coverage is healthy at 2.7%, while its CET1 is 13.4% and still maintains a substantial buffer above minimums. Tangible book value per share increased 6% YoY to $91.52, lifted by buybacks ($1.75B in Q1) and gains from AOCI. For long-term owners, such asset growth combined with better RoTCE indicates better capital efficiency on the horizon.

Source: Q1 Deck

How much is Citi worth? Valuation Outlook

Citigroup is one of the cheapest names among systemically significant banks, even while its operating transformation gains traction. At Q1 2025, Citi is trading at only 0.6x tangible book value versus peers such as JPMorgan at ~2.0x and Bank of America at ~1.3x. Forward P/E is below 8x, following a 21% year-over-year jump in net income and 9.1% improvement in RoTCE.

This extreme discount suggests that the market doubts that Citi’s simplification plan and tech-driven enhancements will come to full fruition. Nevertheless, tangible book value per share increased 6% YoY to $91.52, driven by solid capital returns, including $1.75 billion of Q1 buybacks. At 13.4%, the CET1 ratio is sturdy, and its balance sheet possesses the flexibility to navigate both normalization of credit and reinvestment requirements.

Looking to the future, if Citi continues to trend toward greater operating leverage and earnings efficiency, a re-rating on valuation is possible. Applying a conservative 1.0x–1.1x tangible book multiple as RoTCE approaches 10–12% would support a fair value of between $91–$101 per share, implying ~50% appreciation from today. The sum-of-the-parts DCF backs up this assessment, approximating Citi’s equity value at ~$90 billion, or ~$95 on a per-share basis under very conservative growth assumptions. Risks exist—primarily consumer credit degradation and execution errors on AI scaling—but the margin of safety built into the valuation of Citi provides an asymmetric payoff for a patient investor who is not anticipating cyclical change, but structural change.

Risks of It Getting Derailed

Though Citi’s rehabilitation is persuasive, execution is still risky. The speed of change, especially closing down old systems and integrating full-fledged AI, is audacious with lots of regulator focus. Gen AI launches pose cybersecurity risks as well as operational risks if not carefully managed.

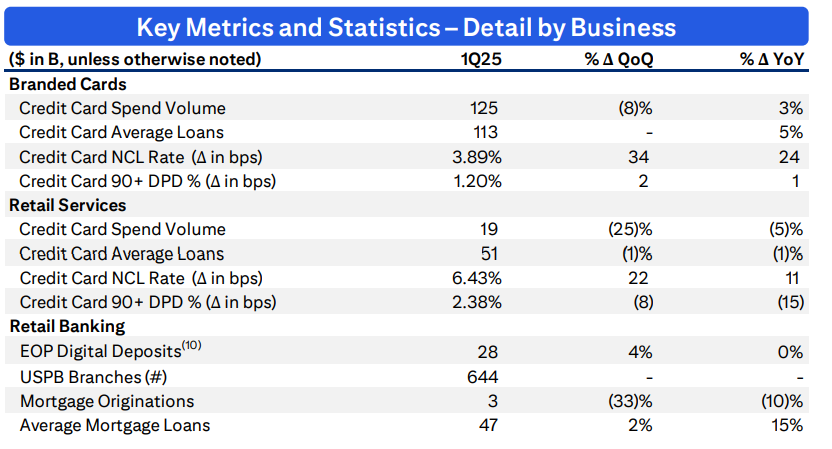

Consumer credit worsening, particularly in USPB cards (4.7% NCL ratio), is another cause for concern, as accelerating delinquencies could drive provisions up further. Citi's international exposure also exposes it to geopolitics, currency risk, as well as delayed exit from non-core geos.

Ultimately, competition for institutional clients is becoming increasingly fierce, with digital-first players, fintech APIs, and low-priced strategies by geographically based banks putting pressure on established players such as Citi not only to modernize, but to out-innovate.

Conclusion

The Q1 2025 numbers from Citi capture a company moving in the right direction, less through hype, though, and more through structural improvement. With a lean cost structure, efficiency through artificial intelligence, and improving yields, Citi is perhaps finally building the foundations for a long-overdue valuation re-rating.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.