TSMC Q2 Results Beat Estimates, Raises Full-Year Outlook, Adds $100 Billion Investment in US to Meet AI Boom

TSMC’s Q2 2026 results exceeded expectations, with revenue rising 36% year-over-year to NT$1,270.381 billion and earnings per share reaching $4.31. Driven by robust demand for advanced 3nm and 5nm nodes and AI-related high-performance computing, the company raised its full-year revenue growth outlook to over 40%. Capital expenditure was increased to $60–$64 billion to bolster advanced packaging and global capacity. Despite these strong fundamentals, market concerns persist regarding the long-term ROI of AI infrastructure and high tech-sector valuations. TSMC remains a critical beneficiary of AI growth, with management projecting sustained supply constraints for advanced nodes.

TradingKey - Global foundry leader TSMC ( TSM) has once again delivered results that far exceeded market expectations. The newly released second-quarter financial results for 2026 not only broke multiple historical records, but the company also simultaneously raised its full-year revenue growth target and capital expenditure plans, further signaling that demand for AI chips remains robust and the construction of global computing power infrastructure continues to accelerate.

According to the financial report, TSMC's Q2 revenue reached NT$1,270.381 billion (approximately $40.2 billion), a year-on-year increase of 36%; net profit soared 77.4% year-on-year to NT$706.562 billion (approximately $22 billion), marking double-digit growth for nine consecutive quarters and significantly outpacing prior market expectations. In US ADR terms, single-quarter earnings per share reached $4.31, beating analyst expectations by 14.32%.

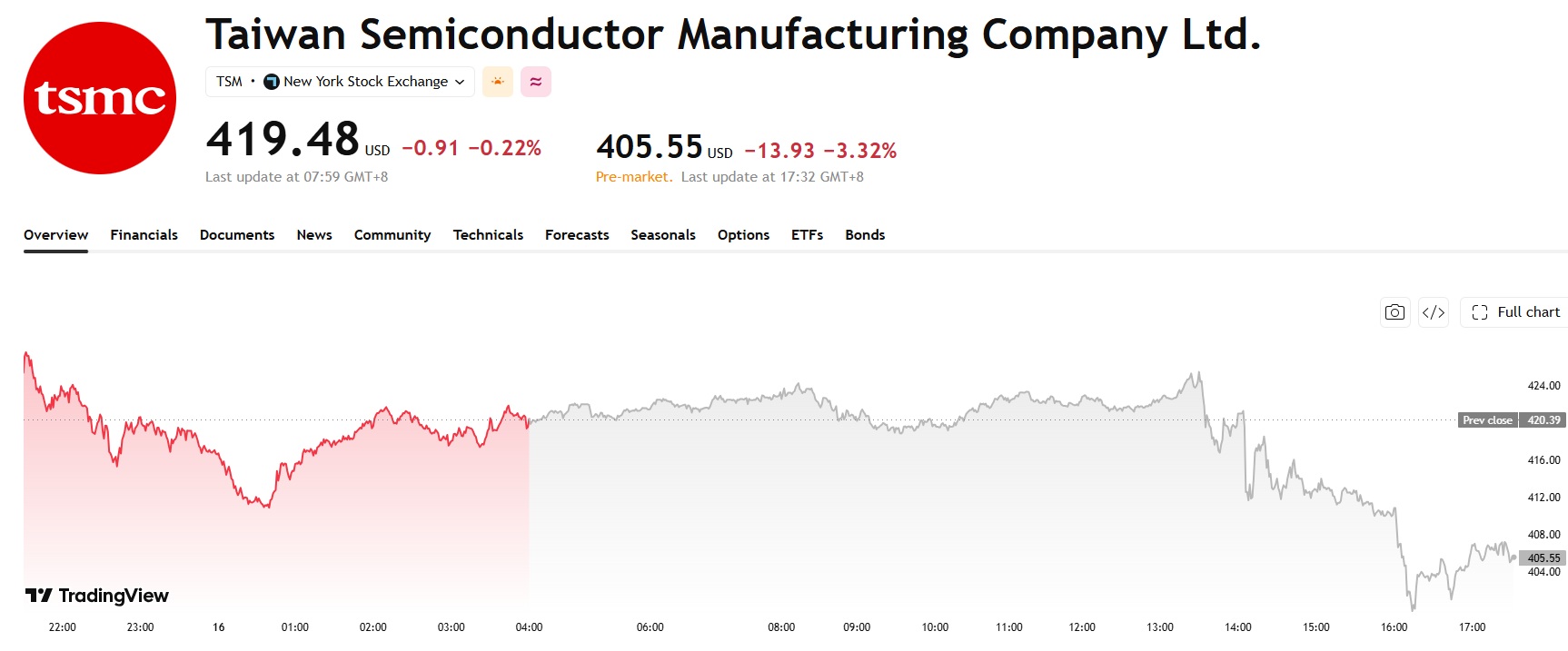

However, the stellar performance failed to lift the stock price; instead, TSMC's ADR fell over 3% in pre-market trading.

Source: TradingView

Advanced Nodes Drive Profitability, AI Computing Power Becomes Core Growth Engine

Financial data shows that TSMC's profitability continues to strengthen, with its Q2 gross margin reaching 67.7%, up 9.1 percentage points year-on-year, continuing to climb quarter-on-quarter and breaking through the upper limit of its own prior guidance. Its operating margin stood at 60.3%, also significantly beating the market expectation of 58.6%. This strong profitability was mainly driven by the high-margin contribution of advanced node chips.

Data on the breakdown of process nodes shows that 7nm and more advanced nodes jointly accounted for 77% of wafer revenue, with the share of advanced nodes continuing to rise.

Specifically, the 3nm node accounted for 30%, while the 5nm node accounted for 33%. As the current mainstream nodes, the two jointly contributed over 60% of revenue. The 7nm node accounted for 11%. This quarter, the 2nm node officially made its commercial debut and began contributing revenue, accounting for 3%, and is currently in a steady ramp-up phase. This high-margin capacity mainly fulfills orders from leading clients such as Nvidia's AI chips and Apple's flagship processors, serving as the core foundation for high earnings growth.

By business segment, the AI computing business became the absolute driver of growth. In the second quarter, high-performance computing (HPC) revenue surged 20% quarter-on-quarter. Benefiting from the iteration of global AI large language models and the large-scale construction of computing infrastructure, orders for AI chips remained fully booked, firmly supporting the company's overall performance.

In contrast, the traditional consumer electronics market remained relatively flat. Smartphone-related business experienced a slight pullback due to seasonal factors, and the recovery rate of demand in the PC market was also relatively limited.

However, the rapid growth in demand for AI chips has been sufficient to offset the impact of the sluggish consumer electronics market, continuing to drive strong overall revenue growth.

Bloomberg Intelligence analyst Charles Shum noted that demand for AI servers and high-performance processors currently remains highly robust. This not only compensates for the weakness in the smartphone and PC markets but also further enhances TSMC's ability to raise product prices in the future, providing sustained support for the company's profit margins.

TSMC Raises Capital Expenditure, US Expansion Accelerates Further

During this earnings call, TSMC further raised its full-year business outlook. The company expects its USD-denominated revenue growth rate to exceed 40% in 2026, a further increase from its previous target of "growth of over 30%," demonstrating management's high level of confidence in future order demand.

Meanwhile, the company also significantly raised its full-year capital expenditure budget from the previous $52 billion to $56 billion to $60 billion to $64 billion, representing an increase of approximately 14% and hitting a record high.

The company's CFO, Wendell Huang, stated during the earnings conference call that capital expenditures over the next three years will increase further and be significantly higher than those of the past three years, underscoring firm confidence in the long-term trend of AI.

Capital will be primarily allocated to the expansion of advanced 2nm and 3nm capacity in Taiwan, as well as the capacity expansion of CoWoS advanced packaging production lines, while steadily advancing plans for overseas plant construction in the US and Japan.

Among these, TSMC confirmed an additional investment of $100 billion in Arizona, expanding its total investment scale to $265 billion to construct four chip factories, with the ultimate goal of establishing 10 wafer fabs and 2 packaging plants in the US.

TSMC CEO C.C. Wei previously stated that even if US domestic capacity continues to increase, the company would still find it difficult to meet the demands of US customers over the next few years, and this capacity expansion is precisely to address this supply-demand gap.

For third-quarter performance, TSMC expects sales to be between $44.6 billion and $45.8 billion, with a midpoint of approximately $45.2 billion, which is about $2 billion higher than the market's average expectation of $43.11 billion. The gross margin guidance range is 65% to 67%, and the operating margin guidance range is 56% to 58%, both broadly in line with market expectations. The company also stated that there are no bottlenecks in capacity expansion and expects cash dividends to continue to increase in 2027.

TSMC Outlook Optimistic, But AI Supply Chain Investment Returns Face Lingering Concerns

TSMC's strong performance and robust guidance have reinforced market confidence in the continued expansion of global AI infrastructure. As the core foundry partner for tech giants such as Nvidia ( NVDA) and Apple ( AAPL ), TSMC's capital expenditure scale is viewed as a key bellwether for the global AI chip supply and demand landscape.

At present, global investment in AI infrastructure is expected to exceed $725 billion this year alone, and SK Hynix even projects that the memory chip shortage will persist beyond 2030, as large-scale procurement by data center operators continues to drive up demand for AI-supporting chips such as High Bandwidth Memory (HBM).

However, some investors remain cautious about the sustainability of AI infrastructure investment. Currently, major global data center operators are financing their massive buildouts by continuously taking on debt, and whether their AI investments can deliver matching returns remains an open question in the market.

Meanwhile, as tech stock valuations remain at elevated levels, the market has also begun to debate whether the current AI supply chain has already priced in growth expectations for the next few years.

TSMC's management remains positive in the face of these concerns. The company believes that capacity for advanced processes and advanced packaging remains in short supply, and AI demand shows no signs of slowing down; instead, it continues to exceed previous expectations, meaning the company will still face capacity constraints for the next several years.

Overall, this earnings report proves once again that TSMC remains one of the highest-certainty beneficiaries in the global AI supply chain today.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.