Netflix Preview | 2Q Net Income Is Expected to Soar 45%; Popular Series & Live Events to Fuel Subscriber Gains

Streaming giant Netflix is set to report its Q2 earnings on July 17th.

The company is projecting double-digit revenue growth and an increase in margins as it moves toward advertising for monetization.

Netflix is poised to report its second quarter 2025 financial results and business outlook post-market on Thursday, July. 17, 2025.

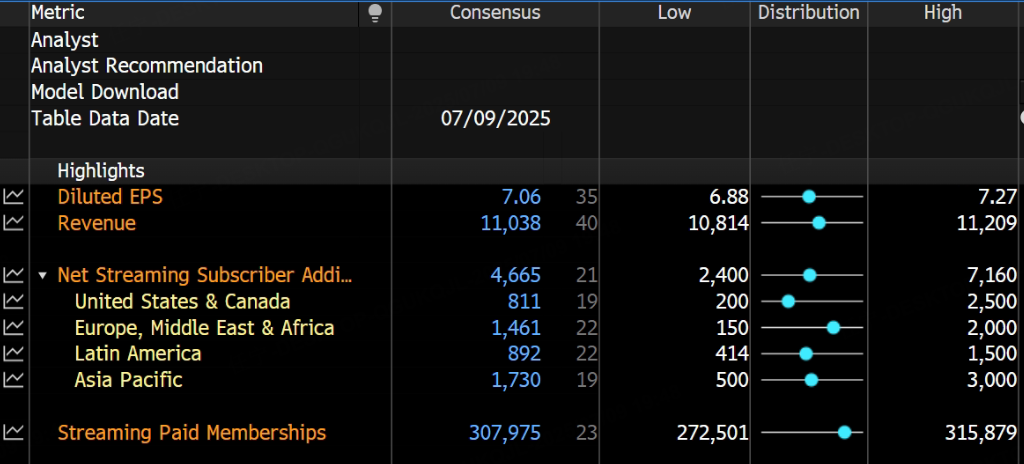

Netflix's Q2 revenue is expected to be $11.04 billion, rising 15.5% compared to the last year. Net income grew to $3.076 billion, or $7.07 per share, up 44.9% from a year ago, according to Bloomberg's consensus expectation.

Source: Bloomberg

Source: Bloomberg

Things to Watch in 2Q Earnings

Netflix Forecasts Another Strong Quarter

According to management's guidance, the company likely generated just over $11 billion in revenue in 2Q, representing accelerated year-over-year growth of 15.5%. At the bottom line, investors will be looking for $7.03 in EPS, which would be up by a whopping 44.1%.

Investors should also keep an eye out for any changes to Netflix's full-year guidance. As of the last update, the company was targeting between $43.5 billion and $44.5 billion in total revenue in 2025, but if management increases that number in the July 17 report, it could add fuel to the bullish sentiment surrounding Netflix stock.

Last Earnings Call (Investor Relations)

Last Earnings Call (Investor Relations)

Popular Series & Live Events to Attract Subscribers

Management characterized Netflix's 2H slate as a "slight embarrassment of riches" given three of its most-popular series will drop from late-June through year-end.

The third and final season of "Squid Game" came out on June 27, and the company is splitting the release of "Wednesday" and "Stranger Things" into two and three parts, respectively. The latter is being eventized, with the first volume scheduled for Thanksgiving, the second for christmas Day and the finale on New Year's Eve. There's also a focus on live events and sports with WWE RaW, NFL Christmas Gameday, the Taylor vs. Serrano boxing match (July 11) and the Canelo vs. Crawford fight (Sept. 13).

Aside from bringing in more paying subscribers, live events give Netflix a massive opportunity to attract advertisers. The company now offers three subscription tiers: Premium ($24.99 per month), Standard ($17.99 per month), and Standard with ads ($7.99 per month). The ad-supported tier regularly accounts for around half of all signups in countries where it's available, so Netflix has a growing opportunity to sell ad slots to businesses.

Ad Boost as Dollars Follow Eyeballs

Netflix is in the early innings of building its advertising business, but the streamer has already achieved reasonable scale with 94 million monthly active users (MAUs) as of May. That translates to roughly 40 million ad-tier subscribers, and the company could get a boost with a blockbuster release schedule, especially with more live events and sports.

Analyst at Bloomberg calculates bout 135 million MAUs or 58.5 million subscribers on the ad tier by year-end. With the content slate increasing subscribers and scale, Netflix will be better positioned to improve monetization with in-house ad-tech investments and programmatic partnerships with third parties like Google and The Trade Desk.

In fact, Netflix's advertising revenue doubled in 2024, and management expects it to double again in 2025 to about $3 billion. More live programming will only support that trend.

Analysts’ Opinions

KeyBanc Capital Markets boosted its price target on Netflix to $1,390 from $1,070, citing confidence in long-term growth driven by live events, price increases, and an expanding advertising business. The firm anticipates revenue will continue to grow by double-digit percentages over the medium term.

KeyBanc is even more bullish, forecasting second-quarter revenue of $11.2 billion and EPS of $7.20, slightly above consensus, attributing the potential upside to favorable foreign exchange rates. For the third quarter, KeyBanc expects revenue guidance to align with the Street’s $11.3 billion estimate.

Barclays raised its price target on Netflix to $1,100 from $1,000 while maintaining an Equalweight rating. Netflix currently trades near its 52-week high. The investment bank cited Netflix’s upcoming content slate as a positive factor, noting the streaming giant will release new seasons of two of its biggest shows, "Stranger Things" and "Wednesday," in the second half of the year, followed by NFL content later in 2025.

Barclays indicated that Netflix continues to benefit from weakness in the U.S. dollar, which should help boost margins throughout the year. The firm also noted that with Netflix no longer disclosing subscriber or ARPU metrics, it remains unclear what might disrupt the company’s current growth momentum.

Related Articles

National Debt Bomb Ignited? Musk Warns U.S. Will Be 1000% Bankrupt Without AI

TradingKey - Tesla (TSLA) CEO Elon Musk recently issued another warning regarding the rapidly ballooning U.S. national debt. He stated clearly that without artificial intelligence and robotics, the United States will inevitably head toward fiscal bankruptcy.

Why Sanae Takaichi Winning Japan’s Diet Election Led to a Surge in Japanese Stock Indices?

TradingKey - Reports indicate that the ruling coalition led by Japanese Prime Minister Sanae Takaichi has secured a single-party majority in the parliamentary elections held on Sunday (February 8). Following the news, the yen weakened slightly, while the Nikkei Index surpassed 57,000 for the first t

A Crash After a Surge: Why Silver Lost 40% in a Week?

TradingKey - Spot silver (XAGUSD) prices continue to decline. Silver plunged 20% on Thursday, breaking below $71 per ounce, with the sell-off intensifying on Friday as prices fell further below $64. Compared to the all-time high set on January 29, silver prices have retraced more than 40%, wiping out nearly all gains accumulated over the previous month.

Is Bitcoin’s Four-Year Cycle Dead in 2026?

Is the Bitcoin 4-year cycle dead? After 2025 broke historical records with a red post-halving year, institutional analysts explore if the Bitcoin price has decoupled from the halving countdown. Analyze the impact of spot ETFs, global liquidity, and the roadmap to the 2028 halving in this 2026 market