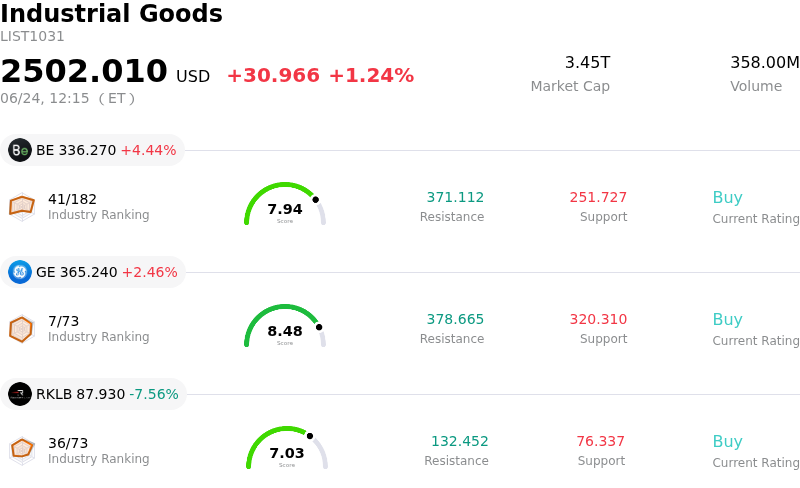

Deere & Co Stock (DE) Moved Up by 3.08% on Jun 24: What Signal Does It Send?

Deere & Co (DE) moved up by 3.08%. The Industrial Goods sector is up by 1.24%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Bloom Energy Corp (BE) up 4.44%; General Electric Co (GE) up 2.33%; Rocket Lab USA Inc (RKLB) down 7.56%.

What is driving Deere & Co (DE)’s stock price up today?

The positive price movement of Deere & Company shares on the current trading day reflects a confluence of strong company-specific updates and favorable macro-industrial shifts that have built upward momentum throughout the month. This upward trajectory occurs amid heightened intraday volatility, as investors continue to balance long-term agricultural cycle concerns against Deere’s near-term structural strengths and aggressive technological pivot.

A major fundamental driver of this positive sentiment is the company’s recent mid-quarter guidance upgrade. Deere caught the market by surprise by raising its full-year net income forecast, primarily fueled by a faster-than-anticipated adoption rate of its advanced "See & Spray" autonomous technology suites and stronger margins in its Production and Precision Agriculture segment. This shift signals to the investment community that Deere is successfully transforming from a traditional, highly cyclical hardware manufacturer into a high-margin, software-integrated technology leader, which has helped expand its valuation multiples.

Further supporting the stock’s rise is the company’s robust capital allocation strategy. Management recently announced a new massive share repurchase program, replacing its previous authorization. This aggressive buyback initiative underscores leadership’s deep confidence in the firm’s long-term cash flow generation capability, offering a strong cushion for the share price even as broader industrial sectors face macroeconomic uncertainty.

Additionally, recent regulatory and product developments have provided meaningful cost relief and market expansion. The U.S. government’s decision to reduce import tariffs on farm and construction equipment directly mitigates input cost pressures that have squeezed manufacturing margins. This tariff reduction, alongside the launch of the new 5E utility tractor featuring an electronically controlled eHydro transmission, reinforces Deere’s operational efficiency and product leadership across both large-scale and smaller farming segments.

However, despite these positive catalysts, underlying market risks remain in focus. Elevated interest rates and depressed crop prices continue to weigh on global farming incomes, keeping customer sentiment in the large agriculture segment muted. Investors must monitor whether these headwinds will eventually dampen demand. For now, the market is prioritizing Deere's diversified business model, where robust infrastructure spending benefits the construction and forestry divisions, offsetting pockets of agricultural weakness and driving the stock’s current outperformance.

Technical Analysis of Deere & Co (DE)

Technically, Deere & Co (DE) shows a MACD (12,26,9) value of 6.553, indicating a buy signal. The RSI at 58.168 suggests neutral condition and the Williams %R at 26.248 suggests buy condition. Please monitor closely.

Fundamental Analysis of Deere & Co (DE)

Deere & Co (DE) is in the Industrial Goods industry. Its latest annual revenue is $45.67B, ranking 2 in the industry. The net profit is $5.03B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $634.90, a high of $759.00, and a low of $471.00.

More details about Deere & Co (DE)

Company Specific Risks:

- Severe Cyclical Downturn in Large Agriculture Segment: Deere's high-margin Large Production & Precision Agriculture segment continues to struggle with a prolonged downturn. Regional demand in the U.S. and Canada is projected to drop 15% to 20% in fiscal 2026, exacerbated by depressed crop prices, rising farm debt levels, and a 15% slide in farmer incomes that are forcing customers to defer major capital upgrades.

- Disruption of Service Revenues from $99 Million "Right-to-Repair" Settlement: Following federal court preliminary approval of a $99 million antitrust settlement, Deere is legally mandated to open its closed diagnostic software ecosystem and provide proprietary tools to independent repair shops for at least a decade. This shifts power away from authorized dealerships, threatening Deere’s highly lucrative captive parts and service network.

- Substantial Margin Compression from Tariff Exposures: The company is facing a direct tariff exposure estimated at $1.2 billion for fiscal 2026, which constitutes an immediate 3% margin headwind. Even after accounting for recent rate cuts and refunds, Deere expects to absorb roughly $900 million in net tariff costs this fiscal year, restricting total margin expansion.

- Stretched Valuation Premium Out of Sync with Fundamentals: Trading at a premium Forward P/E of 27x to 32.5x compared to the industry average of ~21x, the stock heavily discounts an aggressive "next-cycle" peak recovery. This rich valuation leaves the stock highly vulnerable to downside volatility if farm-level economic recovery takes longer than institutional models suggest.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.