PDD Holdings Inc Stock (PDD) Moved Down by 3.17% on Jun 16: Key Drivers Unveiled

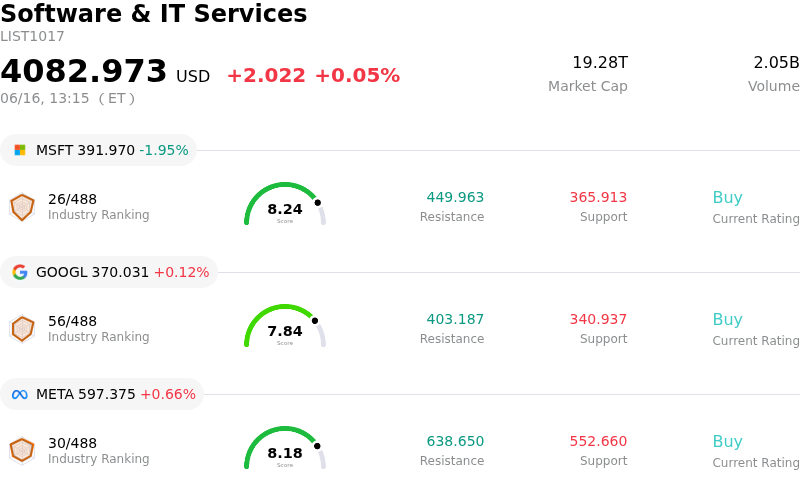

PDD Holdings Inc (PDD) moved down by 3.17%. The Software & IT Services sector is up by 0.05%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) down 1.95%; Alphabet Inc Class A (GOOGL) up 0.12%; Meta Platforms Inc (META) up 0.66%.

What is driving PDD Holdings Inc (PDD)’s stock price down today?

The recent downward pressure and intraday volatility on PDD Holdings shares are primarily driven by a combination of downbeat analyst initiations, persistent concerns over compressing profit margins, and intensifying regulatory headwinds in both domestic and international markets.

A significant immediate catalyst for the decline is a negative shift in sell-side sentiment. BNP Paribas recently initiated coverage on PDD with an Underperform rating, highlighting the company’s complex regulatory landscape and a missed opportunity to bolster share value through more aggressive shareholder return strategies like buybacks. This cautious initiation follows a wave of downward revisions and price target cuts from other major financial institutions after PDD’s first-quarter earnings release. The quarterly report revealed a significant miss on net profit, which fell year-over-year and came in well below consensus expectations. This contraction in profitability is a direct result of the company's aggressive, multi-year investment cycle aimed at bolstering its supply chain, supporting domestic merchants, and building out first-party brands, a strategy that is expected to continue compressing near-term operating margins.

Adding to the company-specific margin pressures are broader domestic macroeconomic and regulatory challenges in China. Ahead of the highly anticipated mid-year shopping festival, Beijing's market regulator summoned Pinduoduo alongside other major e-commerce platforms over deceptive promotional practices. This regulatory clampdown coincides with weaker-than-expected consumer price index data, intensifying investor anxieties regarding sluggish consumer demand and a deflationary retail environment in China. These factors raise doubts about the short-term growth trajectory of PDD’s core domestic business.

Concurrently, PDD's international growth engine, Temu, is navigating its own set of structural and regulatory hurdles. Temu has faced severe compliance scrutiny in key Western markets, including a substantial fine from the European Commission for violating the Digital Services Act. Ongoing legislative and customs scrutiny on low-value import parcels in the United States and the European Union threatens to decelerate Temu's global expansion. With rising compliance and logistics costs and a lack of near-term visibility on international profitability, institutional investors remain highly cautious, leading to elevated volatility and downward pressure on the stock.

Technical Analysis of PDD Holdings Inc (PDD)

Technically, PDD Holdings Inc (PDD) shows a MACD (12,26,9) value of -0.403, indicating a sell signal. The RSI at 38.043 suggests neutral condition and the Williams %R at 58.289 suggests sell condition. Please monitor closely.

Fundamental Analysis of PDD Holdings Inc (PDD)

PDD Holdings Inc (PDD) is in the Software & IT Services industry. Its latest annual revenue is $62.58B, ranking 9 in the industry. The net profit is $14.18B, ranking 9 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $121.21, a high of $170.00, and a low of $17.83.

More details about PDD Holdings Inc (PDD)

Company Specific Risks:

- Beijing Regulatory Summons on Promotional Tactics: On June 11, 2026, the Beijing Municipal Administration for Market Regulation summoned Pinduoduo and other e-commerce platforms over misleading advertising, opaque rules surrounding its "10 Billion Yuan Subsidy" campaign, and failing to disclose seller information ahead of the major 618 shopping festival, escalating regulatory compliance risks and threatening near-term domestic promotional sales.

- Institutional Rating Downgrade to Underperform: On June 15, 2026, BNP Paribas initiated coverage on PDD with an "Underperform" rating and a cautious price target of $89. Analysts highlighted growing domestic and international regulatory challenges, coupled with management's refusal to implement more aggressive shareholder return strategies to support share prices during high volatility.

- Severe Q1 2026 Profit Miss and Planned Margin Compression: PDD’s recently reported Q1 2026 earnings revealed an adjusted EPS of CNY 9.51, missing the consensus estimate of CNY 16.80 by over 43%. Net income fell 15% year-on-year, signaling intense margin compression as management commits to a multi-year RMB 100 billion spending plan to transition to first-party brand building and heavy supply chain investment.

- Cross-Border Tariff Pressures and De Minimis Risk for Temu: The global expansion model for Temu faces operational disruption and cost inflation due to escalating international trade tensions and the expiration of the de minimis tax exemption in the United States, which has directly elevated tariff costs for the platform's low-cost shipping model.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.