Vertiv Holdings Co Stock (VRT) Moved Down by 3.12% on Jun 10: A Full Analysis

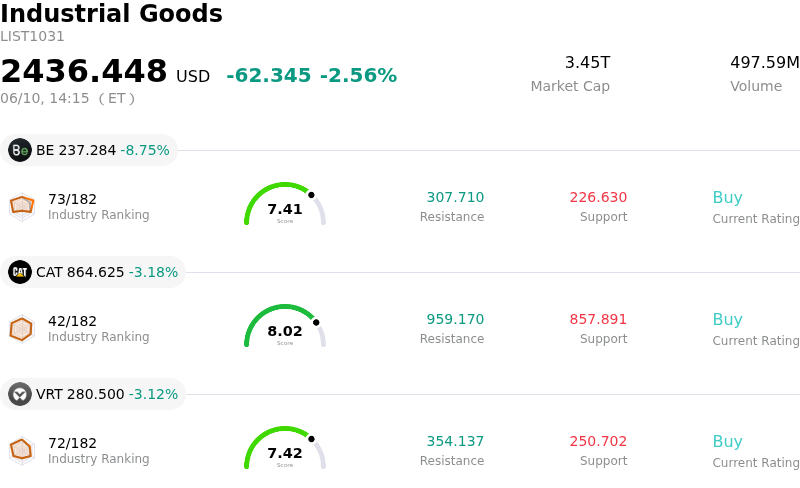

Vertiv Holdings Co (VRT) moved down by 3.12%. The Industrial Goods sector is down by 2.56%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Bloom Energy Corp (BE) down 8.75%; Caterpillar Inc (CAT) down 3.18%; Vertiv Holdings Co (VRT) down 3.12%.

What is driving Vertiv Holdings Co (VRT)’s stock price down today?

VRT experienced a downward movement and significant intraday volatility, which could be attributed to investors reassessing its premium valuation despite a backdrop of generally positive company-specific developments. The company recently reported strong first-quarter 2026 results, exceeding analyst estimates and raising its full-year guidance, driven by significant revenue growth and improved operating margins. This strong financial performance was underscored by approximately 30% year-over-year revenue growth in the first quarter of 2026 and a notable expansion in adjusted operating margins.

Furthermore, Vertiv has been active in product innovation and strategic partnerships, including the introduction of a converged physical infrastructure digital twin for NVIDIA Omniverse DSX, aimed at advancing configurable and simulation-ready AI factory infrastructure. Additionally, the company launched the Vertiv Rack Extreme, a high-capacity rack platform designed for the increasing demands of high-performance computing and AI applications. These initiatives, coupled with its extensive product portfolio, reinforce Vertiv's position as a key beneficiary of the rapidly expanding AI data center market and increasing demand for critical digital infrastructure. The company also declared a quarterly cash dividend recently.

Despite these positive factors, the stock has undergone substantial appreciation, leading to a premium valuation by several metrics. Its P/E ratio, for example, is noted to be significantly higher than historical averages, and some analyses suggest the stock is considerably overvalued. While the overall analyst consensus remains largely bullish with numerous buy and outperform ratings and raised price targets, the elevated valuation might be prompting some market participants to engage in profit-taking or to exercise caution. This rebalancing of investor sentiment regarding the stock's valuation relative to its strong growth prospects and recent positive announcements likely contributed to the observed short-term price correction.

Technical Analysis of Vertiv Holdings Co (VRT)

Technically, Vertiv Holdings Co (VRT) shows a MACD (12,26,9) value of [0.59], indicating a neutral signal. The RSI at 36.21 suggests neutral condition and the Williams %R at -81.04 suggests oversold condition. Please monitor closely.

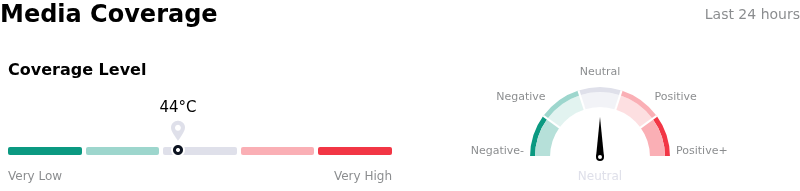

Media Coverage of Vertiv Holdings Co (VRT)

In terms of media coverage, Vertiv Holdings Co (VRT) shows a coverage score of 44, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Vertiv Holdings Co (VRT)

Vertiv Holdings Co (VRT) is in the Industrial Goods industry. Its latest annual revenue is $10.23B, ranking 17 in the industry. The net profit is $1.33B, ranking 13 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $359.30, a high of $500.00, and a low of $112.00.

More details about Vertiv Holdings Co (VRT)

Company Specific Risks:

- Vertiv Holdings Co. (VRT) stock appears overvalued by analysts, trading at a P/E ratio of 68.17 and featuring on lists of "Most Overvalued" stocks, indicating potential for a price correction.

- Analysts express concern that Wall Street's out-year margin assumptions for Vertiv are overly optimistic, with consensus models projecting the company to meet long-term margin targets a full year ahead of schedule, which introduces significant execution risk.

- The assumption of a "smooth" capacity expansion, necessary to fulfill Vertiv's substantial order book, carries meaningful operational risk that could hinder the company's ability to meet demand.

- Potential pressure on Vertiv's valuation is anticipated over the next twelve months due to a projected slowdown in capital expenditure growth by hyperscalers in 2027 and beyond.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.