Can Nvidia be Considered a Growth Stock Anymore?

AI Podcast

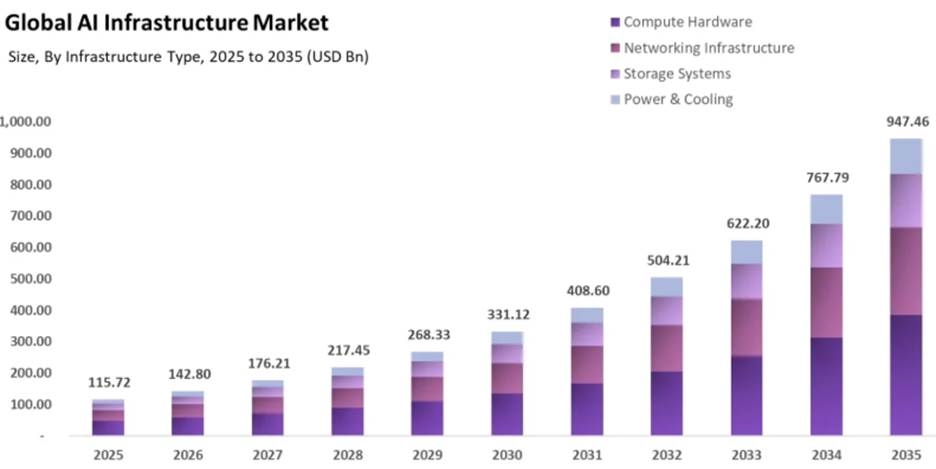

Nvidia's position as the backbone of AI infrastructure drives a bullish outlook, with projected AI market growth to $947.46 billion by 2035. Despite reaching a $5 trillion market cap, Nvidia's robust sales, exceeding $60.9 billion in 2026, and TSM's reliance on Nvidia chips (55% of AI revenue) demonstrate market leadership. Collaborations like the one with NAVER for AI data centers and a 2 million chip addressable market in China for 2026 indicate sustained growth potential. The company's ability to meet soaring demand, particularly for H200 AI chips, coupled with increasing revenue forecasts and strong EPS growth, suggests current market dips present an ideal entry point.

Nvidia: Ride This AI Infrastructure Backbone

TradingKey - I am optimistic on NVIDIA (NASDAQ: NVDA) even after attaining $5 trillion market. Honestly, Nvidia has consistently shown that it is the backbone of AI infrastructure. This huge growth emanates from Nvidia’s current growth and projected future growth. I am relying on the current growth trend and future AI infrastructure growth to rate this company as a buy. For example, the sector already shows a growth potential of $142.80 billion in 2026 and could reach $947.46 billion by 2035. This now begs one question below.

Why is Nvidia a Must Buy Now?

To me the macro-outlook is one of my primary reasons for optimism and also anchors my micro perspective. For instance, at the record sales of up to $60.9 billion in 2026 trailed closely by Intel at $54.2 billion, NVIDIA proves market leadership in semiconductor business.

The logic I am looking at here is whether NVIDIA is indeed an AI infrastructure backbone. In my view, when I look at TSM which is the largest chip manufacturer, its 55% of revenues from AI chip that use Nvidia technology tells me that this is a worthwhile company to invest in. In hindsight this does not only reveal that Nvidia is rallying the AI chip sector sales but also it has a high chance of sustaining this growth. Let’s take an example of the recent partnership with NAVER. Nvidia will be powering NAVER’s upcoming AI data centers which now explains why has the capacity to sustain its market leadership.

From where I seat, the oncoming contracts like NAVER’s and 2 million chips addressable market in 2026 for China gives this company an edge in revenue growth. I will explain this better later but what I am driving here is my optimism on why I am rating Nvidia as a “Buy”.

Is AI Infrastructure A Wealth-Building Backbone? Bull Case

In my previous explanations I mentioned that NVIDIA is currently the market leader in terms of market cap and semiconductor sales. This does not happen by chance but by design. Let’s start with the macro picture before moving to the micro level.

So far, the AI boom is still happening as AI moves from experimentation to a real product. To me, AI is at an inflection point right now, where its adoption is yielding recognizable benefits to a business. Therefore, I believe AI Infrastructure might likely continue soaring rapidly given the adoption rate and economic value.

For instance, 20% of organisations using AI are currently report 74% AI economic value. Well, it shows that there is still a huge gap to be filled despite real economic results. This explains why the market is expected to grow rapidly at a CAGR of 23.4% from $142.8 billion in 2026 to $947.46 billion by 2035.

[Source: Evolvance]

The Demand Outpaces Nvidia’s Supply

So, let’s now get to NVIDIAs for a micro level picture. NVIDIA’s optimism can be seen through the lens of the sale of chips. This year, NVIDIA scrambles to meet rapidly increasing demand for chips, especially for the H200 AI chips.

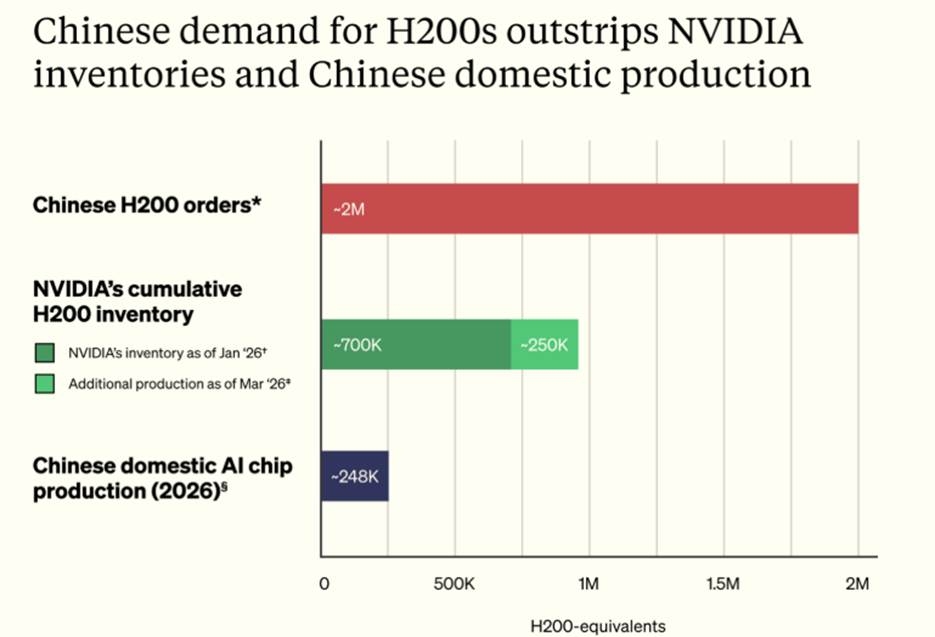

I am taking a scenario here. While, many companies continue placing orders with NVIDIA as previously highlighted, Chinese companies in particular are in full force with a total order of 2 million H200 chips in 2026. What makes it surprising is that NVIDIA reported only 700,000 units of H200 in stock. As an investor, this is not something to worry about because the company meeting these orders due to its collaboration with TSM.

Recall, that 55% of TSM’s AI chip revenues are made from NVIDIA chips. In other words, this is how NVIDIA is fulfilling these orders. In fact, March 2026, Nvidia has increased H200 AI chips to 250,000 from January’s 2026 700,000 H200 AI chips, totaling to 950,000. If you annualize 250,000 chips per quarter, that would mean approximately 1 million chips. This explains that Nvidia is not far from meeting these soaring orders.

[Source: IFP]

It is more interesting that NVIDIA is planning to invest in P.C chips as an additional stream in the consumption of AI capabilities. In other words, I see it as NVIDIA getting into both semiconductor production and AI service consumption. From my perspective, a recent remark by NVIDIA’s CEO Jensen Huang that the company is the largest purchaser of TSM indicates that the company has the capacity to meet unmet demand. Since NVIDIA’s chips are larger and more complex to produce, it is likely to maintain a strong market position for a long time. This is an added advantage for NVIDIA’s chips, which are competing with AMD and Intel chips. In fact, thanks to this advantage, its new Vera CPUs are expected to be more popular than GPUs, given their CPU’s essential role in crunching data. This gives it an edge in the P.C market.

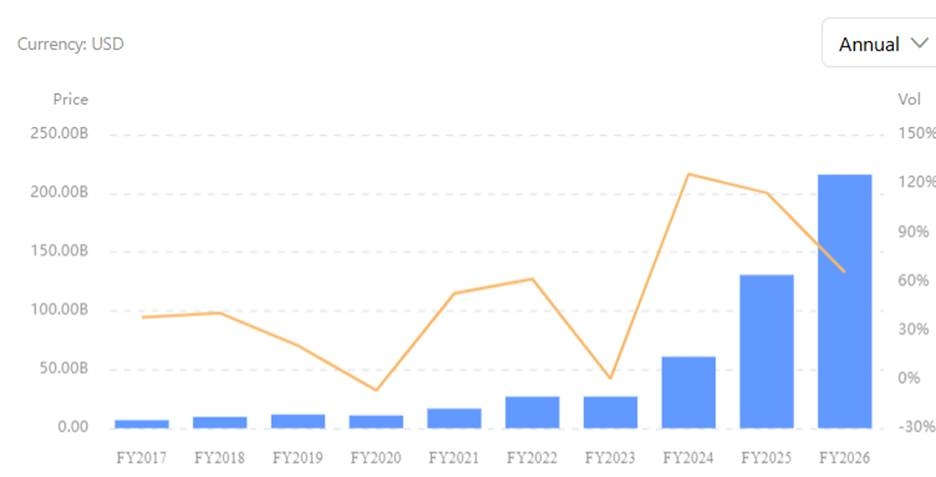

Solid Top-line Of 50% Growth YoY

NVDA is doing well on the top line, and the revenue trend shown in the image below, from 2017 to 2025, is a testament to this observation. This confirms soaring demand for AI infrastructure, and even when we look at the estimated forward revenue, the same occurrence is expected. In FY2025, the company recorded a top line of $130.50 billion, up from $60.92 billion in 2024, representing 114.20% YoY growth. In 2026, the company recorded $215.94 billion, representing 65%, but in my view, I do not want you to be fixated on the decline in YoY growth rate; rather, I want you to focus on the solid revenue upside trend.

[Source: TradingKey]

NVIDIA recorded a revenue of $81.6 billion in Q1’2027, representing 85% YoY. Following the management revenue guidance of $91.0 billion in Q2’2027, I will annualize this revenue to a mid-point of $81.0 billion per quarter. This leads me to estimate FY2027 revenue at $324 billion, representing YoY growth of above 50%. This is still a double-digit score, which is why I am optimistic about NVIDIA. In fact, if GAAP and non-GAAP remain at 74.9% and 75.0%, respectively, and the estimated reductions in GAAP and non-GAAP operating expenses are $8.5 billion and $8.3 billion, respectively, it is likely that NVIDIA earnings will continue to soar.

The top-line performance is also a reflection of earnings, as diluted earnings per share have also been on an uptrend. The diluted EPS trend below ranges from $0.39 in FY2022 to $4.93 in FY2026. Given that this has been achieved through consistent revenue growth, I believe the 2027 revenue increase will result in earnings growth.

TradingKey

On earnings, NVIDIA has been beating analysts’ estimates so far, which is a solid bullish rating factor. For instance, in Q1’2027, it beat analysts’ estimates by 67.1%, reporting actual EPS of $2.44 from an estimate of $1.46. This is a testament to the fact that the revenue increase has had a positive effect on the earnings as well.

[Source: TradingKey]

Given the earnings potential explained above, I believe this is why NVIDIA’s P/E multiple at 31.25x indicates that it is undervalued at the moment. I think investors should note that NVIDIA has been on a consistent uptrend over the last year, up by 45.10%. Given the optimism explained above, I believe this company has a high potential for its stock price to record an upside momentum. What you see today with prices plummeting, I believe, is an oversold scenario in which investors could be taking back profits after a 42% upward move. This is why I think the current dip presents an ideal entry point for a bullish move.

[Source: TradingKey]

Takeaway

I am reiterating my bullish rating driven by NVIDIA’s position in AI infrastructure and its solidified market access for AI chips. I am therefore rating NVIDIA as a buy, especially now that it is seeking to deliver over 2 million N200.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.